30-Second Summary

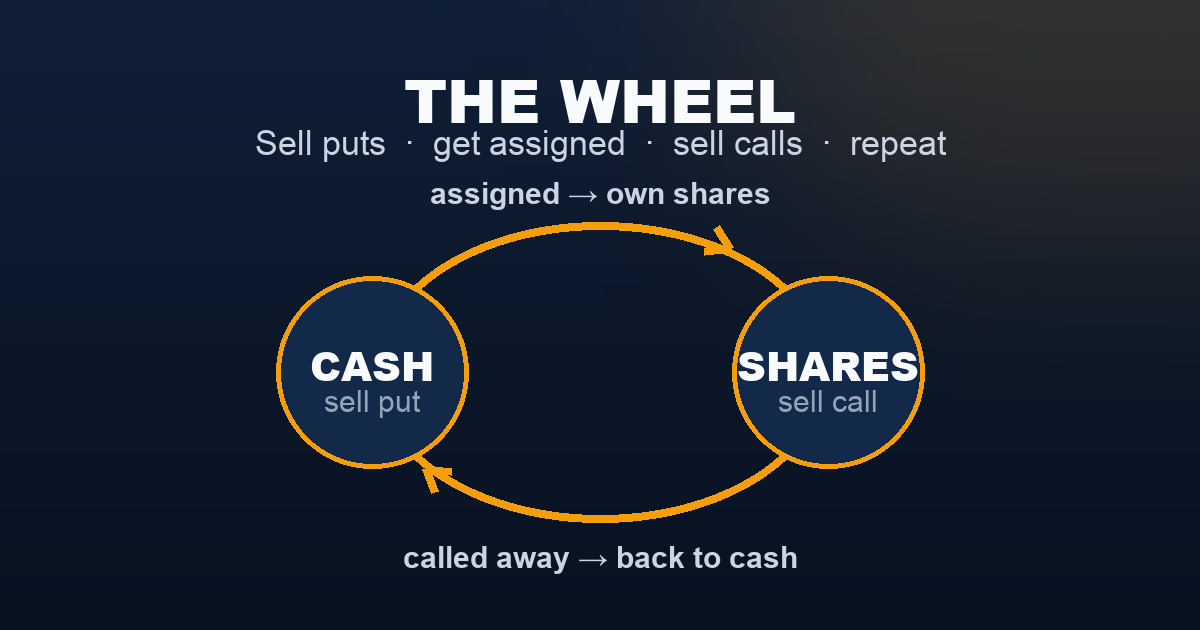

The Wheel isn’t a single trade — it’s a cycle. You sell a cash-secured put on a stock you’d be happy to own. If it expires worthless, you keep the premium and sell another. If you get assigned, you now own 100 shares — so you start selling covered calls against them. When the shares get called away, you’re back to cash, and the wheel turns again.

It’s the most popular systematic income strategy in retail options, and for one reason: every leg is a sale. You collect premium in every phase, theta works for you the entire time, and you only ever own stock at a price you already agreed was fair. The catch is the same catch every premium seller faces — the income is steady and capped, but if the stock craters after you’re assigned, you’re left holding a falling position and grinding calls against it to dig out.

One thing up front: the Wheel needs an underlying that delivers real shares on assignment. That rules out SPX, which is cash-settled. Every example here uses SPY — the ETF tracking the same S&P 500 index. More on that at the bottom .

What Is the Wheel?

The Wheel chains together two strategies you may already know — the cash-secured put and the covered call — into a continuous loop.

Sold on its own, a cash-secured put has two outcomes: the stock stays up and you keep the premium, or it falls and you buy shares at a discount. A covered call also has two outcomes: the stock stays down and you keep the premium, or it rises and your shares are sold at a profit. The Wheel simply says: whatever the outcome, immediately set up the next sale. Kept your cash? Sell another put. Got assigned? Sell calls against the shares. Got called away? Back to cash — sell another put.

Think of it as running a small insurance desk on a single stock. You’re always underwriting something — either the risk of buying the stock cheaper (the put) or the risk of selling it higher (the call) — and you collect a premium every time you write a policy. You don’t need the stock to do anything in particular. You just need it to be a name you’re genuinely willing to own, because sooner or later the wheel will hand you shares.

The phrase to hold onto: you are paid to be patient at both ends. Paid to wait to buy. Paid to wait to sell.

The Four Phases

Here’s the full cycle, with consistent SPY numbers so each phase connects to the next.

Phase 1 — Sell a cash-secured put. Pick a strike below the current price on a stock you’d buy anyway. Set aside the cash to buy 100 shares if assigned.

Phase 2 — Get assigned (or not). If the put expires above the strike, it’s worthless — keep the premium, return to Phase 1. If it expires below, you’re assigned 100 shares at the strike, with your effective cost reduced by the premium you collected.

Phase 3 — Sell a covered call. Now that you own shares, sell a call against them at or above your cost basis. If it expires below the strike, keep the premium and sell another call. Repeat for as long as you hold the shares.

Phase 4 — Get called away. If the call expires in the money, your shares are sold at the strike for a gain. You’re back to 100% cash — and you return to Phase 1 to start the wheel again.

| Phase | Action | If it expires OTM | If it expires ITM |

|---|---|---|---|

| 1 | Sell cash-secured put | Keep premium → repeat Phase 1 | → Phase 2 (assigned) |

| 2 | Buy 100 shares at strike | — | Now hold shares → Phase 3 |

| 3 | Sell covered call | Keep premium → repeat Phase 3 | → Phase 4 (called away) |

| 4 | Sell shares at strike | — | Back to cash → Phase 1 |

The Wheel Cycle

A single price-payoff diagram doesn’t capture the Wheel, because the payoff changes shape depending on which phase you’re in — it’s a short-put profile in Phases 1–2 and a covered-call profile in Phases 3–4. What it actually looks like is a loop:

One full cycle, in cash

Say SPY is trading at $750 and you run the wheel through one complete turn — assigned on the put, then called away on the call.

| Step | Cash flow | Running total |

|---|---|---|

| Sell 1 SPY $745 put (30 DTE) @ $7.00 | +$700 | +$700 |

| Assigned: buy 100 shares @ $745 | −$74,500 | (own shares, cost basis $738 after premium) |

| Sell 1 SPY $750 call (30 DTE) @ $6.00 | +$600 | +$1,300 |

| Called away: sell 100 shares @ $750 | +$75,000 | — |

| Net on shares ($75,000 − $74,500) | +$500 | — |

| Full-cycle profit | +$1,800 |

That’s +$1,800 on roughly $74,500 of cash committed — about 2.4% for the cycle, collected over maybe two months. Run that repeatedly and the premium compounds. Notice you never needed SPY to do anything dramatic: it drifted down enough to assign you, then up enough to call you away, and you got paid at every step.

The risk lives in Phase 2. If SPY had fallen to $700 instead of recovering, you’d be holding 100 shares at a $738 cost basis — a $3,800 unrealised loss — and your job becomes selling calls month after month to grind the basis down. That’s the deal: the upside is capped at the premiums plus the gap between strikes, the downside is owning a stock that keeps falling.

The Seller’s Advantage

The Wheel is a 100% seller strategy — there is no buying leg anywhere in the cycle. So the right comparison isn’t buyer-vs-seller; it’s the Wheel versus simply buying and holding the shares.

| The Wheel (Seller) | Buy & Hold (Owner) | |

|---|---|---|

| Income while flat | Premium every cycle | Dividends only |

| Probability of a profitable month | ~70–80% (premium cushions small moves) | ~55–60% (pure direction) |

| Upside in a big rally | Capped — shares called away at the strike | Unlimited |

| Downside in a crash | Same as owning, minus premiums collected | Full |

| Theta | Friend — earns every day | Neutral |

| Who wins more often? | The Wheel | — |

| Who wins bigger in a melt-up? | — | Buy & Hold |

The edge is real but bounded. In flat, choppy, or slowly rising markets — which is most of the time — the Wheel out-earns buy-and-hold because it monetises time and volatility the holder leaves on the table. In a sharp sustained rally, buy-and-hold wins easily, because the Wheel keeps capping your gains at each call strike. And in a crash, the Wheel offers no real protection — the premiums are a thin buffer against a position that behaves like long stock the moment you’re assigned.

This is the same insurance-company math behind every selling strategy on this site: frequent small wins, the occasional ugly stretch, and an edge that only shows up over many cycles — not any single one.

Understanding the Greeks

The Wheel’s Greeks shift between phases, but they all point the same direction the whole way around the loop.

Delta (always net positive): In Phases 1–2 you’re short a put — positive delta, you want the stock up. In Phases 3–4 you own shares and are short a call — still net positive delta, around +0.50 to +0.70. The Wheel is structurally a mild bullish position at all times. You never benefit from the stock falling; you only ever benefit from it rising or sitting still.

Theta (always your friend): Because every phase involves a short option, time decay works in your favour continuously. Whether you’re holding a short put or a short call, each day that passes without the option going deeper in the money is premium earned. The Wheel is, at its core, a machine for harvesting theta on a name you’re willing to own.

Vega (always negative): You’re perpetually short an option, so rising implied volatility hurts and falling IV helps. Selling the put or call when VIX is elevated collects fatter premiums and sets up an IV-crush tailwind. The flip side: a volatility spike right after you sell creates an unrealised loss even if the stock hasn’t moved much.

Gamma (always negative): The short option carries negative gamma, which bites near expiration when the strike is close. A stock oscillating around your put strike (or call strike) in the final days swings the position between “expires worthless” and “assignment” on small moves. This is why many Wheel traders close or roll at 50% of max profit rather than fighting gamma into the last few days.

Rho (ρ = ∂P/∂r — minor here): With 30 DTE options, rho is negligible. It only starts to matter on much longer-dated positions, which the Wheel rarely uses. Not a primary concern for a monthly cycle.

Trade Management & Adjustments

Strike and DTE selection. Most systematic Wheel traders sell the put around 0.30 delta (roughly 5–7% out of the money) at 30–45 DTE, and close at 50% of max profit to recycle capital faster. Same logic on the covered-call side once assigned.

Always sell calls at or above your cost basis. This is the cardinal rule of Phase 3. If you were assigned at $745 with a $738 effective basis, do not sell a call at $735 just because the premium is fat — getting called away below your basis locks in a loss. Sell at $745 or higher so that assignment is a win.

Rolling to avoid (or accept) assignment. If the put is challenged and you don’t want the shares yet, roll it down and out for a credit. If the call is challenged and you don’t want to give up the shares, roll it up and out. Only roll if your view on the stock is intact — rolling a put on a name you no longer want to own just deepens a mistake.

Knowing when to break the wheel. The Wheel assumes the underlying is a name you’d hold through a drawdown. If the company’s story changes — or, on an ETF like SPY, if your whole market thesis changes — the right move can be to take the loss and stop, not keep selling calls into a structural decline. The strategy is mechanical, but the choice of what to wheel is not.

What to avoid:

- Wheeling a stock you don’t actually want to own. Assignment is not optional — it’s the whole point.

- Reaching for premium by selling calls below your cost basis after assignment.

- Treating the premiums as downside protection. They’re an income enhancement, not a hedge.

Real-World Example

The setup: A trader wants exposure to the S&P 500 but thinks the index is slightly rich at $750. Rather than buy outright, they start a wheel — getting paid to wait for a better entry.

Cycle, month by month:

- Month 1 — sell the put. Sell 1 SPY $745 put for $7.00 → +$700. SPY drifts to $748 by expiration. The put expires worthless. Keep the $700. (Still in cash.)

- Month 2 — sell again, get assigned. Sell 1 SPY $740 put for $6.50 → +$650. This time SPY sells off to $731 into expiration. Assigned 100 shares at $740. Effective cost basis: $740 − $6.50 − the prior $7.00 = $726.50.

- Month 3 — covered call below the noise. Holding shares at a $726.50 basis with SPY at $731, sell a $745 call for $5.00 → +$500. SPY chops sideways and closes at $738. Call expires worthless. Keep the $500. Basis now $721.50.

- Month 4 — called away. Sell another $745 call for $5.50 → +$550. SPY rallies to $752. Shares called away at $745. Gain on shares: ($745 − $740) × 100 = +$500. Back to cash.

Tally for the cycle: $700 + $650 + $500 + $550 in premium = $2,400, plus $500 on the shares = +$2,900 — on roughly $74,000 of committed capital, across four months.

Buy-and-hold over the same stretch went from $750 to $752: a +$200 gain on the shares. The Wheel made over 14× that, because it monetised four months of chop and one assignment dip that the holder just sat through.

The honest footnote: had SPY kept falling after Month 2 — say to $690 — the trader would still be in Phase 3, holding shares underwater and selling calls month after month to claw the basis down. The cycle above is a good turn of the wheel. They aren’t all good. The edge is in running it through many turns, taking the assignments on names you’re glad to own, and letting the premium compound across the ones that work to cover the ones that don’t.

When to Use the Wheel

Best conditions:

- You want to own a particular stock or ETF, but at a better price than today’s — and you’re happy to be paid while you wait.

- Implied volatility is elevated (higher VIX) — fatter premiums on both the puts and the calls.

- The market is flat, choppy, or slowly rising. The Wheel feasts on sideways tape.

- You have the capital to be cash-secured on 100 shares (or the margin and discipline to run it on reduced buying power).

Avoid when:

- You’re not genuinely willing to own the underlying through a 20–30% drawdown. Assignment is a feature, not a bug.

- You expect a sharp sustained rally — buy-and-hold will beat a capped wheel badly.

- IV is very low — thin premiums may not justify the capital tied up and the management overhead.

Ideal VIX level: Above 18. The Wheel’s whole engine is selling volatility, so a higher VIX both pays you more upfront and sets up the IV-crush tailwind. Below 14, the premiums on a low-volatility ETF like SPY get thin enough that the cycle barely beats holding.

⚠️ Why the Wheel Doesn’t Run on SPX

Everything on this site is built around 0DTE SPX selling, so it’s worth being explicit: you cannot run the Wheel on SPX. The strategy depends on assignment delivering 100 real shares you can then sell calls against — and SPX never delivers shares.

SPX is a cash-settled, European-style index option. There’s no early assignment, and at expiration an in-the-money option settles in cash, not stock. There is no “Phase 2” — you’re never handed shares, so there’s nothing to write covered calls on. The wheel has no second half.

That’s why every example here uses SPY, the ETF that tracks the same S&P 500 index. SPY options are American-style and physically settled: an assigned put hands you 100 SPY shares at the strike, exactly what the Wheel needs. QQQ (Nasdaq-100) works the same way if you want tech-tilted exposure. The mechanics are identical to the covered call and cash-secured put pages, which also use SPY for the same reason.

So: the Wheel is a tool for the equity/ETF side of your book. SPX 0DTE iron condors live in a different universe — cash-settled, same-day, no shares ever changing hands. Both are premium-selling at heart; they just settle differently. For the full index-vs-ETF picture (settlement, exercise style, and the Section 1256 tax angle), see SPX vs SPY Options .

Strategy Ladder — Next Steps

Built from: The Wheel is two beginner trades chained together. Learn the halves first if you haven’t — Cash-Secured Put (Phases 1–2) and Covered Call (Phases 3–4).

Natural progression from here:

- Want defined-risk premium selling without owning shares? → Bull Put Spread — the capped-risk cousin of the cash-secured put

- Ready for two-sided, market-neutral income? → Iron Condor — sell both a put spread and a call spread at once

- Want stock-like exposure for less capital than the Wheel? → Poor Man’s Covered Call (PMCC) — replace the 100 shares with a long LEAPS call

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.