30-Second Summary

A naked short put is mechanically identical to a Cash-Secured Put — you sell a put, collect premium, and profit if the underlying stays above the strike. The difference is capital: a CSP holds the full strike × 100 in cash as collateral. A naked short put uses margin instead, requiring far less capital upfront.

That difference has a serious consequence. If the put is assigned on a cash-secured position, you buy the stock with cash you already have. If you’re assigned on a naked put in a margin account, you buy 100 shares of stock on borrowed money during a decline — the scenario most likely to trigger a margin call.

This is a seller’s strategy. Theta works in your favour. The risk is not the option mechanics — it’s the leverage applied to a position when the market is falling hardest.

What Is a Short Put?

When you sell a put option, you take on the obligation to buy 100 shares of the underlying at the strike price if the buyer exercises. A naked short put means you do this without holding the full cash to fund that purchase. The position sits in a margin account, backed by the account’s margin capacity rather than dedicated collateral.

The word naked means uncovered — no long put below the short to cap your loss, and no cash earmarked for assignment. This distinguishes it from:

- The Cash-Secured Put (Level 1) — same short put, fully funded with cash. Assignment is manageable. No leverage risk.

- The Bull Put Spread — same short put, with a long put below it. Max loss is defined. No assignment delivers stock.

If the CSP is the conservative version and the bull put spread is the defined-risk version, the naked short put sits between them in character but above both in leverage risk. Most experienced traders run it on cash-settled indexes (SPX) specifically to avoid physical assignment — cash settlement means no shares change hands at expiration, only the cash difference.

The key phrase: the position is identical to a CSP — until assignment. That’s when the capital structure matters.

Setup & Execution

Legs:

- Sell 1 put option below the current price

That’s it. No long leg, no offsetting position. Pure short premium exposure.

Strike selection:

- Same logic as the CSP: sell OTM puts at a level you’d be comfortable buying the underlying

- Most traders target the 20–30 delta range — roughly 65–80% probability of expiring worthless

- Higher delta (closer to ATM) = more premium but higher assignment probability

- On SPX (cash-settled), assignment mechanics don’t apply — only the P&L matters at expiration

Expiration selection:

- 21–45 DTE: Standard window. Theta decay is meaningfully accelerating and there’s time for the trade to mature.

- 7–14 DTE: Faster decay but higher gamma risk. Fine for high-frequency systematic sellers.

Margin requirements: Naked short puts require a margin account with options Level 3 or 4 approval, depending on the broker. The typical margin requirement for a single naked short put is calculated as:

20% of underlying price × 100 + premium received − OTM amount

For a $515 SPY put with SPY at $520, margin is roughly:

(20% × $520 × 100) + $500 − $500 = $10,400

Compare to:

- CSP: $51,500 in cash set aside

- Bull Put Spread: ~$4,500 locked up (spread width − credit)

- Naked Short Put: ~$10,400 in margin capacity

The naked short put requires less capital than a CSP but more than a spread — and unlike both, the risk is leveraged if the underlying falls sharply.

SPY Example — Entry:

Trade:

- Sell: 1 SPY $515 Put (30 DTE) for $5.00 = $500 premium received

- Margin held: ~$10,400 (broker-calculated)

- Breakeven at expiry: $515 − $5.00 = $510

- Max profit: $500 (SPY ≥ $515 at expiry)

- Max loss: Theoretically $51,000 (SPY → $0); practically, a 20% drop to $416 = −$9,400

Comparing the three ways to run the same short put:

| Naked Short Put | Cash-Secured Put | Bull Put Spread | |

|---|---|---|---|

| Short strike | $515 | $515 | $515 |

| Premium collected | $500 | $500 | ~$450 (net) |

| Max profit | $500 | $500 | ~$450 |

| Max loss | Unlimited (leveraged) | ~$50,500 (unleveraged) | ~$4,550 (defined) |

| Capital required | ~$10,400 (margin) | $51,500 (cash) | ~$4,550 |

| Assignment risk | Yes — on leverage | Yes — cash available | No |

| Return on capital | ~4.8% | ~1.0% | ~9.9% |

The naked short put has the highest return on capital — but the return metric is only meaningful if the margin collateral is stable. Under stress, margin requirements expand just as losses mount.

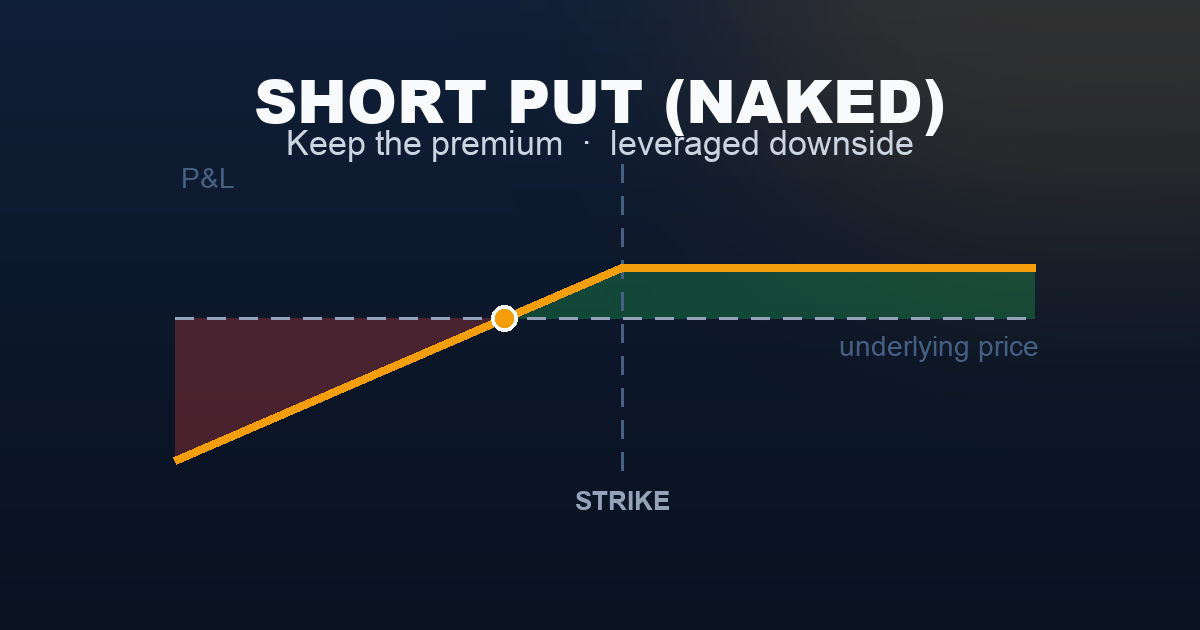

The Payoff Diagram

| SPY at Expiry | P&L |

|---|---|

| $545 | +$500 (max profit) |

| $520 (entry) | +$500 (max profit) |

| $515 (strike) | +$500 (max profit) |

| $510 (breakeven) | $0 |

| $490 | −$2,000 |

| $460 | −$5,000 |

| $416 (−20%) | −$9,400 |

The loss accelerates as SPY falls — $100 per each dollar below breakeven, with no floor. Compare this to the Cash-Secured Put payoff — identical shape, but with a CSP you have the $51,500 in cash ready to absorb the outcome. With a naked short put, that capital doesn’t exist in the account.

The Leverage Risk

The mechanics of the short put are the same regardless of how you fund it. The P&L profile above applies to both the CSP and the naked short put. What changes is what happens when SPY falls and assignment occurs.

Cash-Secured Put — assignment scenario:

- SPY falls to $490, put expires in the money

- You are assigned 100 shares at $515

- Your $51,500 in cash covers the purchase

- You now own SPY at $515, effective cost $510 after premium

- Paper loss: ($510 − $490) × 100 = −$2,000 on paper, fully funded, no margin call

Naked Short Put — same scenario:

- SPY falls to $490, put expires in the money

- You are assigned 100 shares at $515

- Your broker charges $51,500 to your margin account

- Your margin capacity was only ~$10,400 for this trade

- The remaining $41,000+ must come from your account’s total equity

- If your total account equity can’t cover it: margin call, forced liquidation, additional losses

The naked short put’s risk isn’t hypothetical — it’s the scenario that follows naturally from a normal market correction. A 10–15% decline in SPY is not unusual. If your account holds multiple naked short puts across several underlyings, one coordinated move lower can trigger cascading margin calls.

This is why the naked short put is classed as intermediate rather than beginner, and why many experienced traders run it only on cash-settled underlyings (SPX) where no shares are actually delivered.

Understanding the Greeks

The Greeks for a naked short put are identical to those of a Cash-Secured Put — there is no difference in position structure, only in capital treatment.

Delta (positive, ~+0.30 to +0.45): The position gains when the underlying rises and loses when it falls. As SPY approaches the strike from above, delta grows toward +1.0 — the position tracks the stock price closely. Below the strike, you are effectively long 100 shares delta on margin.

Theta (positive — your friend): Every day that passes without a breach of the strike is earned income. For a 30 DTE naked short put, theta earns $5–$15 per day in decay. Time is on your side — but only while SPY stays above the breakeven.

Vega (negative — your enemy): Rising implied volatility increases the cost to close the position. If VIX spikes after entry, the put you sold becomes more expensive to buy back, creating an unrealised loss even if SPY hasn’t moved. High VIX at entry means more premium — but VIX can always go higher.

Gamma (negative — accelerates risk near expiry): As expiration approaches with SPY near the strike, the short put’s delta changes rapidly. A small decline near expiry can produce a large loss swing. Systematic sellers typically close well before expiration to avoid the final week of gamma risk.

Rho (positive): Higher rates slightly benefit the short put — puts become less valuable as rates rise. Negligible for 30 DTE positions.

Trade Management & Adjustments

Taking profits early: Close at 50% of max profit. If you collected $500 and the put is now worth $250 to close, close it. This releases margin capacity, reduces gamma risk, and frees capital for the next cycle. The final 50% of profit is almost never worth the tail risk of holding to expiration.

Rolling: If SPY declines toward the strike, you can roll — buy back the expiring put and sell a new one at a lower strike and/or later expiration for additional credit. This delays the loss and collects more premium, but extends risk into a declining market. Roll only if you genuinely expect SPY to recover, not as reflexive hope.

Converting to a spread: If the trade moves against you, the fastest risk-reduction available is buying a lower-strike put to convert the naked short put into a bull put spread. This caps your maximum loss immediately at the cost of some premium. It’s more expensive than opening the spread from the start, but useful in a fast-moving decline where you need to define risk quickly.

When to close without rolling: If SPY breaks a key technical support level, if the reason you entered has changed, or if your account equity is approaching margin call territory — close. Taking a defined loss is always better than being forced out at a worse price by the broker.

What to avoid:

- Running naked short puts across multiple uncorrelated underlyings simultaneously. When markets fall, they fall together. Correlated positions compound the margin problem.

- Using margin capacity to the limit. Leave meaningful buffer — margin requirements can expand mid-trade if volatility spikes.

- Confusing the high probability of profit with low risk. A 70% probability of full profit means 30% probability of a loss that can be many multiples of the gain.

Real-World Example

The trade: A trader with a $40,000 margin account sells a naked short put. SPY is at $518 and they believe it will remain flat or rise modestly.

- Sell: 1 SPY $510 Put (30 DTE) for $4.00 → $400 received

- Margin held: ~$9,800 (broker estimate)

- Breakeven: $506

- Max profit: $400

Scenario A — the expected outcome (SPY stays flat):

SPY drifts to $524 over 30 days. Both puts expire worthless.

Result: +$400

Return on margin: $400 / $9,800 = 4.1% in 30 days (~49% annualised on margin). High-looking, but the denominator is borrowed capacity — not stable capital.

Scenario B — the dangerous outcome (SPY falls 12%):

An unexpected macro shock sends SPY from $518 to $455 over three weeks.

- The $510 put moves deep in the money

- With SPY at $455, the put is worth ~$55 = $5,500 — a $5,100 unrealised loss

- Margin requirements expand as SPY falls: broker may increase required margin to $18,000+

- The trader’s $40,000 account now has ~$34,500 in equity — still above margin call threshold for now

- But: if they held 3 naked puts across different names that all fell together, margin calls begin

At expiration with SPY at $455, assignment occurs:

- Forced purchase of 100 shares at $510 = $51,000

- Account equity of ~$34,500 plus any remaining margin capacity must cover this

- If insufficient: forced liquidation of other positions to meet the obligation

The same trade as a bull put spread (sell $510, buy $460):

- Net credit: $3.50 = $350 (slightly less)

- Max loss: ($510 − $460 − $3.50) × 100 = $4,650 (defined)

- Margin required: ~$4,650

- No assignment risk

The spread earns $50 less but limits the worst-case outcome from uncapped to $4,650. For most traders, that trade-off is correct.

When to Use This Strategy

Best conditions:

- You trade SPX (cash-settled) and want to avoid stock assignment entirely

- You have significant margin buffer and understand the leverage dynamics

- You are running a systematic, high-frequency premium selling program with strict position-size discipline

- You explicitly prefer the higher return-on-margin ratio over the defined-risk of a spread

Avoid when:

- Your account holds multiple positions that could all decline simultaneously

- You are new to margin — the mechanics of margin calls and forced liquidation require experience to manage under pressure

- VIX is already elevated — a naked short put entered during a volatile market risks assignment into a fast-moving decline

For most traders: the Bull Put Spread is a better structure. The small reduction in credit is almost always worth the elimination of uncapped loss and reduced margin requirement. The naked short put earns incrementally more in normal markets and catastrophically more in bad ones — in the wrong direction.

Ideal VIX level: 16–22. Same as the CSP and bull put spread — elevated IV means more premium. The difference is that at higher VIX levels, the probability of a sharp decline is also higher, which makes the naked structure more dangerous precisely when it’s most lucrative.

Strategy Ladder — Next Steps

Came from: Cash-Secured Put — the same short put, fully funded. If you understand the CSP, you understand the short put. The only new concept here is margin and what it means when the trade goes wrong.

The defined-risk version: → Bull Put Spread — add a long put below the short to cap your maximum loss. Nearly identical premium collection, dramatically different tail risk.

The next level: → Collar (coming soon) — own stock, sell a covered call, buy a protective put. Combines short put economics with explicit downside protection.

Natural progression:

- Systematically selling puts on SPX with defined risk? That’s the put side of an Iron Condor

- Want to use LEAPS as a synthetic stock substitute to run high-leverage short puts with less capital at risk? → PMCC / Synthetic Long (coming soon at Level 3)

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.