30-Second Summary

A collar owns stock, sells an OTM call above the current price, and buys an OTM put below it — all in a single structure. The call you sell generates premium that funds the put you buy. When the strikes are chosen so the premiums match, the protection costs nothing net: a zero-cost collar.

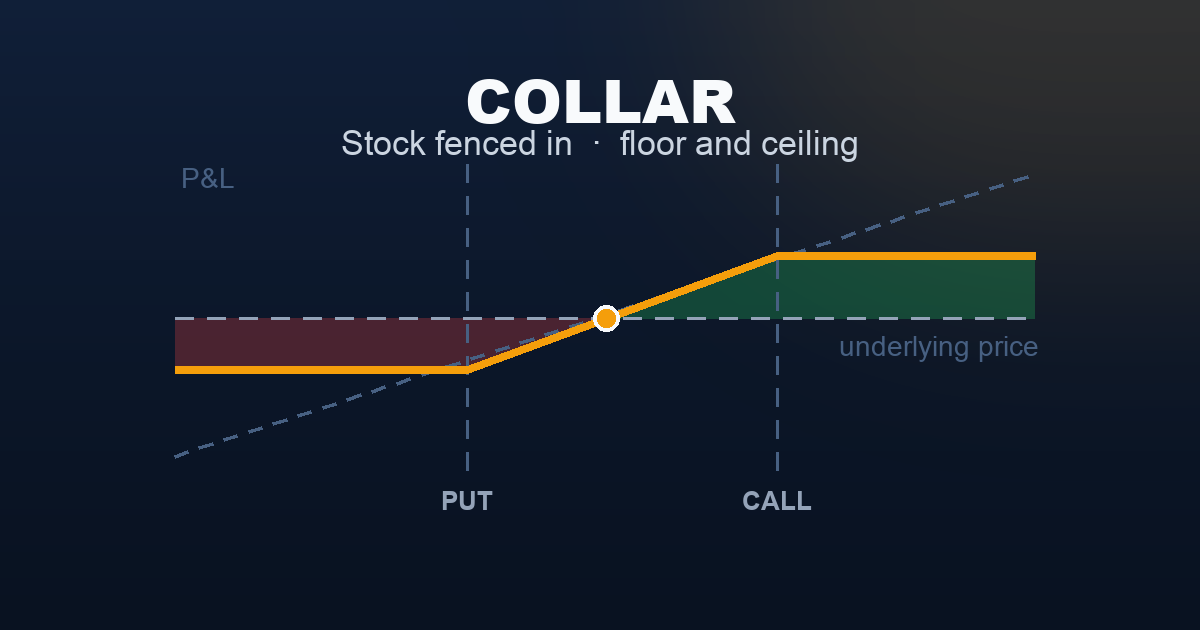

The result: a bounded position. Your downside is floored at the put strike. Your upside is capped at the call strike. In between, the position behaves like stock ownership. The collar is not a trade you put on to make money — it is a trade you put on to control risk you already have.

What Is a Collar?

A collar is what you get when you run a Covered Call and a Protective Put simultaneously on the same position:

- Own 100 shares of the underlying

- Sell 1 OTM call above the current price (the covered call leg — caps upside, generates credit)

- Buy 1 OTM put below the current price (the protective put leg — floors downside, costs premium)

If the call premium equals the put premium, the two legs cancel out and the collar costs nothing. The covered call pays for the protective put. You’ve converted an open-ended stock position into a defined-range position with no upfront cost.

This is not a coincidence — it’s the design. The collar is the most capital-efficient form of portfolio protection available for a stock position. Rather than paying for a protective put out of pocket, you fund it by agreeing to cap your upside. Whether that trade-off makes sense depends on your conviction about the underlying’s future direction.

The key phrase: you are giving up something you might not need (a large rally) to get something you definitely want (a defined floor).

Setup & Execution

Legs:

- Leg 1: Own 100 shares of the underlying

- Leg 2 (Sell): 1 OTM call above the current price — collects premium, caps upside

- Leg 3 (Buy): 1 OTM put below the current price — pays premium, floors downside

Strike selection and cost structure:

The distance between the strikes and the current price determines both the level of protection and the net cost:

- Zero-cost collar: choose strikes so call premium = put premium. No net cash changes hands. Most common and most practical.

- Net debit collar: buy the put at a higher strike or closer to ATM than the call. Better protection, costs money upfront.

- Net credit collar: sell the call much closer to ATM (or further OTM on the put). Collect premium net but cap upside more aggressively.

For a zero-cost collar, the call strike is usually further OTM than the put strike — because calls typically command more premium than equidistant puts in rising-market environments.

Expiration selection:

- 30–45 DTE: Standard monthly protection, manageable premium and flexibility to roll.

- 90+ DTE: More efficient for longer-term holders — lower annualised premium cost, fewer rolls required.

- LEAPS (1 year+): Used for long-term concentrated positions. Set it and manage at a lower frequency.

SPY Example — Zero-Cost Collar:

Trade:

- Own: 100 shares SPY @ $520

- Sell: 1 SPY $530 Call (30 DTE) for $5.00 = $500 received

- Buy: 1 SPY $510 Put (30 DTE) for $5.00 = $500 paid

- Net cost: $0 (zero-cost collar)

- Breakeven at expiry: $520 (entry price — no net premium to recover)

- Max profit: ($530 − $520) × 100 = $1,000 (SPY ≥ $530)

- Max loss: ($520 − $510) × 100 = $1,000 (SPY ≤ $510)

For a month of completely defined risk, the net cost is zero. The call at $530 caps the upside; the put at $510 floors the downside. The position can neither make more than $1,000 nor lose more than $1,000 at expiration — regardless of how far SPY moves.

Understanding the structure:

| Leg | Action | Premium | |

|---|---|---|---|

| Stock | 100 shares @ $520 | Own | $52,000 deployed |

| Call | $530 strike | Sell | +$500 received |

| Put | $510 strike | Buy | −$500 paid |

| Net | $0 |

The collar’s symmetry in this example — $10 OTM on each side for the same premium — reflects balanced market expectations. In practice, put skew typically means the put costs more for the same distance; you would sell the call closer to ATM to match the premium.

The Payoff Diagram

| SPY at Expiry | P&L |

|---|---|

| $490 | −$1,000 (max loss — floor holds) |

| $510 (put strike) | −$1,000 (max loss) |

| $520 (entry / breakeven) | $0 |

| $530 (call strike) | +$1,000 (max profit) |

| $560 | +$1,000 (max profit — cap holds) |

Below the put strike ($510), the floor activates. Above the call strike ($530), the cap activates. Between the two strikes, the position tracks stock ownership exactly — dollar for dollar. The zero-cost entry means the breakeven is exactly the stock’s entry price.

The Cost of Certainty

The collar is best understood by comparing it to its component strategies and to holding stock alone:

| Collar | Protective Put | Covered Call | Stock Only | |

|---|---|---|---|---|

| Net cost | $0 | −$500 | +$500 | $0 |

| Downside floor | $510 ✓ | $510 ✓ | None | None |

| Max loss | −$1,000 | −$1,000 | ~Unlimited | ~Unlimited |

| Upside cap | $530 | None | $530 | None |

| Max profit | +$1,000 | Unlimited | +$1,000 | Unlimited |

| Theta | Near neutral | Negative | Positive | N/A |

The collar occupies the middle of the table. It shares its defined max loss with the protective put and its upside cap with the covered call — but unlike either standalone strategy, it costs nothing net.

The comparison that matters most is against the standalone protective put: both have the same floor ($510) and the same max loss (−$1,000). But the protective put costs $500 while the collar costs nothing — because the call covers it. The price of free protection is the cap at $530. If you believe the stock will stay below $530 over the next 30 days, the collar is strictly better than the standalone protective put.

The comparison against stock only is stark. Stock ownership has no floor — a 30% decline costs $15,000+. The collar caps that at $1,000, for free, with the only cost being forfeited gains above $530.

Understanding the Greeks

A symmetric zero-cost collar — equidistant strikes, matched premiums — has near-neutral Greeks from the options legs. This is one of its most useful properties.

Net Delta (~+0.30 to +0.45): Stock contributes +1.0 delta. The short call subtracts roughly −0.35 delta (you’re short a call with delta ~0.35). The long put subtracts roughly −0.30 delta (you’re long a put with delta ~−0.30, contributing negatively). Net delta is approximately +0.35 to +0.45 — still positively directional, but significantly less than naked stock ownership. The position participates in about 35–45% of the stock’s daily move.

Net Theta (near zero): The short call earns theta; the long put pays theta. For symmetric, equidistant strikes with matched premiums, these approximately cancel. Unlike a naked protective put (which bleeds theta daily), the collar has almost no daily time decay cost. This is the practical advantage of funding the put with a call: the protection doesn’t drain your account each day.

Net Vega (near zero): The short call is short vega (hurts from rising IV); the long put is long vega (benefits from rising IV). For symmetric strikes, these roughly cancel. The collar is largely indifferent to volatility changes — another practical advantage for long-term holders who don’t want to manage vega risk.

Net Gamma (near zero for symmetric collars): The short call’s negative gamma and the long put’s positive gamma offset each other for equidistant strikes. The collar behaves almost like a linear, bounded stock position with minimal optionality curvature. In practice, slight asymmetries in the strikes will introduce small positive or negative gamma, but this is rarely a significant management consideration.

The overall picture: a symmetric zero-cost collar acts like a capped, floored stock position with almost no option Greeks to actively manage. This is why it’s popular for long-term holders — you get defined risk without ongoing theta drain, vega exposure, or gamma surprises.

Trade Management & Adjustments

Rolling the call: As expiration approaches with SPY above the call strike ($530), the call will be exercised and your shares called away. If you want to keep the shares, roll the call forward — buy back the expiring $530 call and sell a new call at a higher strike and/or later expiration, collecting additional premium. This effectively ratchets your upside cap higher while maintaining protection.

Rolling the put: If SPY declines toward the put strike ($510), you can roll the put — sell the existing put and buy a new one with a lower strike and/or later expiration. Rolling the put down and out maintains the collar structure if you want to stay in the trade, but reduces the floor level. Only roll down if you can afford the lower floor.

Lifting the call (partial unwind): If you become more bullish mid-trade, you can buy back the short call to remove the upside cap while keeping the protective put. The put becomes a standalone protective put again, just as if you’d bought it originally — though you’ll pay the current call price to close it, which may be more than the credit you received if SPY has rallied.

Closing the full collar: If you decide to sell the stock, close all three legs simultaneously: sell the shares, buy back the short call, and sell the long put. Most brokers support multi-leg orders that handle this as a single transaction.

What to avoid:

- Collaring a stock you’re no longer willing to hold. The collar defers the decision to sell — it doesn’t eliminate the underlying position risk.

- Setting the put strike too far OTM for a “zero cost” collar by also setting the call too close to ATM. This produces a cheap collar but aggressively caps a stock you presumably hold because you’re bullish on it.

- Ignoring dividend dates. SPY calls are American-style — the buyer can exercise early before ex-dividend to capture the dividend. If your covered call is exercised early, you lose the dividend and your collar’s structure unwinds.

Real-World Example

The trade: A trader holds 100 shares of SPY bought at $522. A major election is scheduled in 28 days, introducing significant near-term uncertainty. The trader is long-term bullish but wants to protect the position through the event without selling. VIX is low at 14.2, making protection relatively cheap.

- Own: 100 shares SPY @ $522

- Sell: 1 SPY $534 Call (30 DTE) for $4.50 = +$450

- Buy: 1 SPY $510 Put (30 DTE) for $4.50 = −$450

- Net cost: $0

- Max profit: ($534 − $522) × 100 = +$1,200 (SPY ≥ $534)

- Max loss: ($522 − $510) × 100 = −$1,200 (SPY ≤ $510)

Scenario A — Protection triggered (SPY falls):

The election produces an unexpected result. SPY falls from $522 to $488 over the 30 days.

| With Collar | Without Collar | |

|---|---|---|

| Stock P&L | −$3,400 | −$3,400 |

| Short $534 call | Expired worthless | — |

| Long $510 put | +$2,200 (intrinsic $22 × 100) | — |

| Net P&L | −$1,200 (floor) | −$3,400 |

The collar absorbed $2,200 of a $3,400 loss. The floor held exactly as designed.

Scenario B — Cap triggered (SPY rallies):

The election is resolved smoothly. Risk assets rally. SPY moves from $522 to $556.

| With Collar | Without Collar | |

|---|---|---|

| Stock P&L | +$1,200 (capped, shares called at $534) | +$3,400 |

| Short $534 call | Exercised — shares sold at $534 | — |

| Long $510 put | Expired worthless, −$450 | — |

| Net P&L | +$1,200 (capped) | +$3,400 |

The collar cost $2,200 in missed upside. The protection that wasn’t needed consumed gains.

These two scenarios define the collar’s character: it narrows the outcome to a defined range. Whether that’s worth it depends entirely on how much uncertainty you’re willing to accept.

When to Use This Strategy

Best conditions:

- You hold a meaningful stock position through a specific, time-limited risk event (earnings, election, economic data, regulatory decision)

- VIX is low — protection is cheap, making the zero-cost collar achievable with minimal upside sacrifice

- You have a large unrealised gain you cannot or don’t want to realise yet (tax considerations, holding period)

- You are comfortable giving up some upside in exchange for sleep-at-night certainty

Avoid when:

- You are strongly bullish — the call cap limits the very outcome you’re positioning for

- The spread between available strikes is too wide to achieve a zero-cost collar without setting the call far too close to the current price

- You’re applying it mechanically every month on a position you’d be better off simply selling

Ideal VIX level: 12–18. Lower VIX makes the zero-cost collar easier to structure — more premium from the call can fund a closer put. Above 20, both puts and calls are more expensive, but the asymmetric nature of put skew means achieving zero-cost may require selling a call that’s uncomfortably close to ATM.

Strategy Ladder — Next Steps

Came from: Covered Call + Protective Put — the collar is exactly these two strategies stacked on the same position. If you’ve read both, you’ve already understood the collar’s components.

This completes Level 2. You now understand single-leg strategies, all four vertical spreads, the naked short put, and the collar. The building blocks for everything at Level 3 are in place.

At Level 3:

- Iron Condor — sell a bull put spread below the market and a bear call spread above it simultaneously. Profit from range-bound markets with defined risk on both sides. The core strategy on this site.

- Iron Butterfly (coming soon) — tighten the iron condor until both short strikes share the same price. Higher credit, narrower profit zone.

- PMCC / Synthetic Covered Call (coming soon) — use a deep ITM LEAPS call as a stock substitute to write covered calls with far less capital.

- Calendar Spread (coming soon) — exploit the difference in time decay between two expirations on the same strike.

→ Level 3 — Advanced Strategies

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.