30-Second Summary

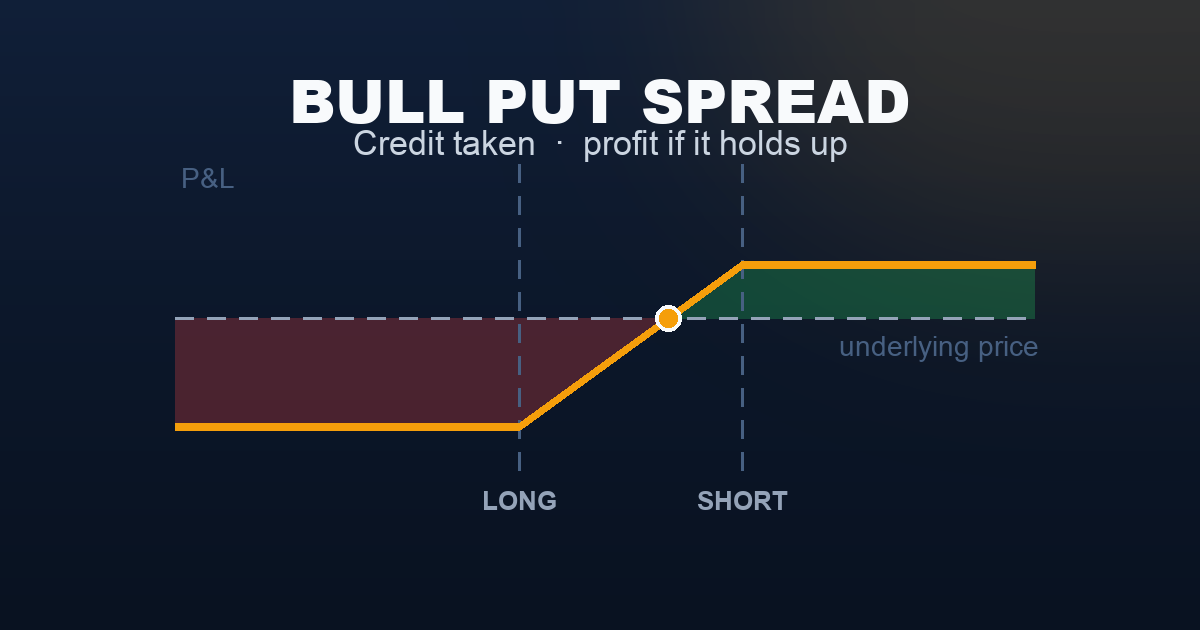

A bull put spread sells a put at a higher strike and buys a put at a lower strike — same underlying, same expiration. You receive a net credit upfront. If the underlying stays above the short put strike at expiration, both puts expire worthless and you keep the full credit. If it falls below the short strike, your profit erodes. If it crashes through the long strike, you’ve hit your maximum loss — defined and capped.

This is a seller’s strategy. Theta works in your favour every day. You don’t need SPX to rise — you just need it not to fall past your short strike. The trade-off: your maximum loss is larger than your maximum gain. Probability is on your side, but the losses when they come are proportionally larger.

What Is a Bull Put Spread?

A bull put spread — also called a vertical put credit spread — combines two puts on the same underlying with the same expiration:

- Sell 1 put at a higher strike (the short leg — where the premium comes from)

- Buy 1 put at a lower strike (the long leg — this caps your maximum loss)

You receive the net difference between the two premiums as a credit. That credit is your maximum profit. Without the long put, you’d have a naked short put — the same premium, but unlimited downside risk if SPX falls sharply. The long put at the lower strike acts as a floor. In exchange for paying a small amount for it, you convert an uncapped position into a defined-risk one.

The bull put spread is the put-side equivalent of the bear call spread, and together they form the two wings of an iron condor — the core strategy on this site. Understanding the bull put spread is a direct prerequisite to understanding how iron condors are constructed and managed.

The key phrase: you profit by being right about what doesn’t happen. SPX doesn’t have to rise — it just needs to not fall past your short strike.

Setup & Execution

Legs:

- Leg 1 (Sell): 1 put at the higher strike — the core of the trade, where the credit comes from

- Leg 2 (Buy): 1 put at the lower strike — the protection that defines your max loss

Both legs: same underlying, same expiration.

Strike selection:

- Short strike OTM: Sell below the current price. The further OTM, the higher the probability of keeping the full credit — but the less premium collected. Most traders target the 20–30 delta level for the short strike.

- Long strike further OTM: Typically 25–50 points below the short strike on SPX. Wider spreads collect more credit but carry proportionally larger max loss.

- Key ratio: aim to collect at least 20–25% of the spread width. Collecting $10 on a $50-wide spread = 20% — a reasonable floor for risk/reward.

Expiration selection:

- 21–45 DTE: The standard window. Theta decay is accelerating and there’s time for the trade to mature without excessive gamma risk.

- 0–14 DTE: High gamma risk near the short strike in the final days. The spread can swing dramatically on small SPX moves.

- 7 DTE (rolling income): Used by systematic sellers who roll frequently. Lower credit per cycle but faster theta capture.

SPX Example — Entry:

Trade:

- Sell: 1 SPX 7,475 Put (30 DTE) for $22.00 = $2,200 received

- Buy: 1 SPX 7,425 Put (30 DTE) for $7.00 = $700 paid

- Net credit: $15.00 per contract = $1,500 received

- Max profit: $1,500 (if SPX ≥ 7,475 at expiry)

- Breakeven at expiry: $7,475 − $15.00 = $7,460

- Max loss: ($7,475 − $7,425 − $15.00) × 100 = $3,500

For maximum profit, SPX must close at or above $7,475 at expiration — it can rise, stay flat, or fall up to 25 points as long as it stays above the short strike. SPX can move in either direction as long as it doesn’t breach 7,475.

Breaking down the net credit:

| Short 7,475 Put | Long 7,425 Put | Net | |

|---|---|---|---|

| Premium | +$2,200 (received) | −$700 (paid) | +$1,500 |

| Max gain | Unlimited exposure | Caps loss at 7,425 | $1,500 |

| Max loss | Unlimited (naked) | Limited to spread | $3,500 |

The long put at 7,425 costs $700 to buy. That $700 converts unlimited downside into a capped $3,500 maximum loss. It is not a cost — it is the price of certainty.

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,650 | +$1,500 (max profit) |

| 7,500 (entry) | +$1,500 (max profit) |

| 7,475 (short strike) | +$1,500 (max profit) |

| 7,460 (breakeven) | $0 |

| 7,450 | −$1,000 |

| 7,425 (long strike) | −$3,500 (max loss) |

| 7,350 | −$3,500 (max loss) |

Above the short strike ($7,475), both puts expire worthless and you keep the full $1,500 credit — regardless of how far SPX rises. Below the long strike ($7,425), both puts are in the money and the loss is flat at maximum. Between the two strikes, P&L transitions linearly through the breakeven at $7,460.

The shape is the mirror image of the bear call spread — profit on the right, loss on the left.

The Defined-Risk Advantage

The bull put spread is best compared to selling the put naked — the trade you’d have without the long put.

| Bull Put Spread | Naked Short Put | |

|---|---|---|

| Net credit received | $1,500 | $2,200 (no long put cost) |

| Max profit | $1,500 | $2,200 |

| Max loss | $3,500 (defined) | Enormous (SPX toward 0) |

| Margin required | ~$3,500 (spread width − credit) | Typically $15,000–$30,000+ |

| Theta | Positive — earns each day | Positive — earns each day |

| Probability of max profit | ~65–70% | ~65–70% (same short strike) |

The naked short put collects $700 more in premium but carries tail risk that is theoretically as large as SPX going to zero. The spread reduces your credit slightly while capping the worst-case outcome at $3,500.

The margin comparison is decisive for most traders. A naked short put on SPX requires substantial margin collateral — often $15,000 to $30,000 or more depending on the broker and account type. The spread requires only the net max loss (~$3,500). Four or five spread positions can be run for the capital cost of a single naked put, with fully defined and distributed risk.

The bull put spread is also directly comparable to the Cash-Secured Put from Level 1. A CSP commits large amounts of cash to back a single short put and accepts full assignment risk. The bull put spread commits $3,500, caps the loss, and requires no assignment-ready capital. For traders who want the credit spread income profile without the capital intensity of a CSP, the bull put spread is the natural evolution.

Understanding the Greeks

Net Delta (positive, ~+0.15 to +0.25): You sold the higher-strike put (contributing positive delta, since you’re short negative delta) and bought the lower-strike put (contributing negative delta). Net delta is positive — the position gains when SPX rises and loses when it falls. As SPX falls toward the short strike, net delta increases in magnitude and losses accelerate. Below the long strike, both puts are deep ITM, their deltas converge, and net delta approaches zero — locked at max loss.

Net Theta (positive — your friend): As time passes with SPX above the short strike ($7,475), both puts decay. The short put decays faster (higher time value, closer to ATM), so net theta is positive — you earn money each day SPX doesn’t fall through your strike. For a 30 DTE spread collecting $15 credit, net theta might be $5–$10 per day. You profit from time standing still.

Net Vega (negative — your enemy): The short put has more vega than the long put. Rising implied volatility hurts the position — the short put becomes more expensive to buy back even if SPX doesn’t move. This is the principal risk in volatile, high-VIX environments. Conversely, IV crush after entry (VIX falling while SPX stays flat) is a pure tailwind.

Net Gamma (negative — accelerates losses near short strike): The short put has more gamma. As expiration approaches with SPX near $7,475, the position’s delta swings rapidly. A decline through the strike produces large, fast losses. Negative gamma is the reason systematic sellers close at 50% profit or 21 DTE rather than holding to expiration.

Net Rho (positive): Higher interest rates reduce put values — the short put loses value, which benefits the position (you could buy it back cheaper). The effect is small for 30 DTE positions and not a primary consideration.

Trade Management & Adjustments

Taking profits early: Close at 50% of max profit. If you collected $1,500 and the spread is now worth $750 to buy back, close it. Capturing $750 in half the time and redeploying capital is almost always better than holding for the final $750 through gamma-heavy expiration week. Many systematic traders also use a time-based close: 21 DTE regardless of profit level, to avoid the accelerating risk of the final three weeks.

Rolling down and out: If SPX falls toward the short strike, you can roll — buy back the existing spread and sell a new one at a lower strike and/or later expiration. Rolling extends the profit zone downward and collects additional credit, but it also increases your maximum loss if SPX continues to decline. Roll only when your thesis on SPX is intact. Rolling a losing position into a bigger losing position is one of the most common mistakes in options trading.

Defending a breach: If SPX closes below the short strike ($7,475) and the position has moved against you, your options are:

- Close immediately and accept the loss — cleanest if the reason you entered is gone

- Hold if SPX is still above the long strike ($7,425) and you believe the decline will reverse

- Roll down and out for additional credit if conviction remains

Never let a bull put spread drift to max loss without a decision. The spread structure caps the loss — but reaching that cap requires deliberate inaction.

What to avoid:

- Entering bull put spreads when the market is in a confirmed downtrend. Credit spreads are not tools for catching falling knives.

- Widening the spread to collect more credit without proportionally increasing your risk tolerance. A $100-wide spread collecting $20 has the same ratio but a much larger max loss.

- Treating 65–70% probability of profit as a guarantee. One loss at max ($3,500) erases more than two maximum wins ($1,500 each). Position sizing matters more than entry selection.

Real-World Example

The trade: SPX has pulled back to a support zone near 7,490 after a 3% decline over two weeks. VIX has spiked to 19.2 on the move lower, making put premiums elevated. The trader has no strong directional view but believes SPX is unlikely to breach support and fall another 25+ points. A bull put spread captures the elevated put premium while defining the downside.

- Sell: 1 SPX 7,475 Put (30 DTE) for $17.00 = $1,700

- Buy: 1 SPX 7,425 Put (30 DTE) for $7.00 = $700

- Net credit: $10.00 = $1,000

- Max profit: $1,000

- Max loss: ($50 − $10) × 100 = $4,000

- Breakeven: 7,465

What happened:

SPX found its footing at support and recovered over the following two weeks. It drifted from 7,492 to 7,518 by expiration — a modest rally. Both puts expired worthless.

Result: +$1,000 (full max profit)

The position required no active management. SPX didn’t even need to rally — just not fall 25 more points. The elevated VIX at entry translated into meaningful credit, and when VIX subsequently declined to 16 over the 30 days, IV crush accelerated the position’s decay toward zero. The position was worth $500 (50% of max) at day 14 — a systematic seller would have closed there and redeployed.

The scenario that breaks it: Had SPX instead continued lower to 7,400:

- Both puts ITM at expiration

- Loss = ($50 − $10) × 100 = −$4,000 (max loss)

- The long put prevented any additional loss below 7,425

Six maximum-profit trades ($1,000 each) = $6,000. One maximum-loss trade = −$4,000. The math favours the seller, but only with disciplined position sizing and consistent management.

When to Use This Strategy

Best conditions:

- SPX is at or near a known support level, and you believe a further decline is unlikely

- VIX is elevated — more credit available for the same strike distance, and any subsequent IV decline benefits the position

- You want to sell premium with defined risk and no requirement to hold large cash collateral

- You are combining it with a bear call spread above to form an iron condor

Avoid when:

- The market is in a confirmed downtrend — credit spreads on the put side should not fight falling momentum

- VIX is very low — thin premiums may not justify the margin tied up and the management overhead

- A major catalyst (earnings, FOMC, CPI) is inside the expiration window that could send SPX sharply lower

Ideal VIX level: 18–30. The higher the VIX, the more credit you collect for the same strike placement. Bull put spreads are especially attractive after a market pullback when VIX has spiked and SPX is sitting at a support level — maximum premium, maximum edge.

Strategy Ladder — Next Steps

Came from: Cash-Secured Put or Short Put (Naked) — the same short put strategy, with either full cash or margin collateral and unbounded risk. The bull put spread is the defined-risk evolution of both.

The bearish credit mirror: → Bear Call Spread — sell a call spread above the market. Same credit structure, opposite directional bias. Combine the two and you have an iron condor.

The bullish debit alternative: → Bull Call Spread — buy a call spread instead. Pay a debit, get a better risk/reward ratio, but theta works against you. Use when you expect a directional move rather than sideways action.

Natural progression:

- Stack a bull put spread below the market and a bear call spread above → Iron Condor — collect credit from both sides, profit if SPX stays within a defined range

- Narrow the strikes until both spreads share a common short strike → Iron Butterfly (coming soon at Level 3) — higher credit, narrower profit zone

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.