30-Second Summary

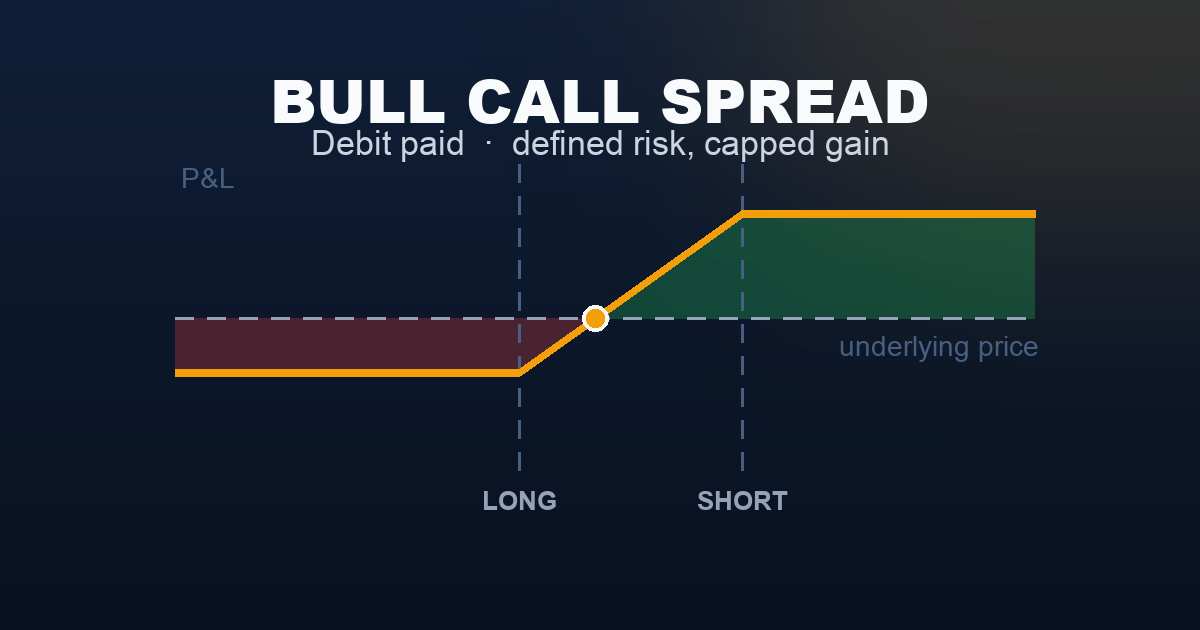

A bull call spread buys a call at one strike and sells a call at a higher strike — same underlying, same expiration. The sold call’s premium partially offsets the cost of the bought call. You pay less to enter, your maximum loss is smaller, and your breakeven is lower. The trade-off: your profit is capped at the short strike. If SPX blows through both strikes and keeps going, you keep only the spread width minus what you paid — nothing more.

This is the right tool when you have a moderate bullish view with a specific price target. If you expect a massive move, a single long call serves you better. If you expect a defined, measured rally, the spread is more capital-efficient.

What Is a Bull Call Spread?

A bull call spread — also called a vertical call debit spread — combines two calls on the same underlying with the same expiration date:

- Buy 1 call at a lower strike (the position you want, the bullish bet)

- Sell 1 call at a higher strike (the offset, reducing your net cost)

The sold call generates a credit that reduces the net premium you pay. In exchange for that subsidy, you hand back all profit above the short call’s strike. The result: a lower-cost, lower-risk, capped-upside bullish position.

The word vertical refers to the fact that both options share the same expiration — only the strikes are different (arranged vertically on an options chain). This distinguishes it from calendar and diagonal spreads, which involve different expirations.

Think of it this way: you’re buying a bullish bet on SPX from 7,525 to 7,575 — and nothing beyond that. You’ve agreed in advance to give away any gains above 7,575 in exchange for paying less to enter. Whether that’s a good deal depends entirely on how far you think SPX will actually move.

The key phrase: the spread defines both your maximum loss and your maximum profit before you enter. Unlike a naked long call, there is no scenario where this trade loses more than the net debit paid.

Setup & Execution

Legs:

- Leg 1 (Buy): 1 call at the lower strike — your directional bet

- Leg 2 (Sell): 1 call at the higher strike — the offset that reduces your cost

Both legs: same underlying, same expiration.

Strike selection:

- Both OTM: Lower cost, higher breakeven, requires a larger move. The most common setup for moderate directional trades.

- Long leg ATM, short leg OTM: Higher net debit, lower breakeven, higher probability of profit. A more aggressive setup.

- Spread width: Wider spreads (100+ points on SPX) cost more but offer more profit potential. Narrower spreads (25–50 points) are cheaper but give less room for the trade to develop.

A useful rule of thumb: if you’re paying more than 50% of the spread width as net debit, the risk/reward is working against you. Aim for a net debit of 20–35% of the spread width for balanced setups.

Expiration selection:

- 30–45 DTE: The sweet spot for directional spread trades. Enough time for the thesis to play out, without paying excessive theta.

- 0–14 DTE: Very high risk. Both legs see rapid theta decay; the spread can collapse to near-zero quickly if SPX doesn’t move.

- 60–90 DTE: Slower decay, more time for the trade to work, but higher upfront cost.

SPX Example — Entry:

Trade:

- Buy: 1 SPX 7,525 Call (30 DTE) for $29.00 = $2,900

- Sell: 1 SPX 7,575 Call (30 DTE) for $14.00 = $1,400

- Net debit: $15.00 per contract = $1,500 total paid

- Max profit: ($7,575 − $7,525 − $15.00) × 100 = $3,500

- Breakeven at expiry: $7,525 + $15.00 = $7,540

- Max loss: $1,500 (the net debit)

For maximum profit, SPX must close at or above $7,575 at expiration — a rally of 75 points (1.00%) from entry.

Breaking down the net cost:

| Long 7,525 Call | Short 7,575 Call | Net | |

|---|---|---|---|

| Premium | −$2,900 (paid) | +$1,400 (received) | −$1,500 |

| Max gain | Unlimited | Caps at $7,575 | $3,500 |

| Max loss | $2,900 | Offset by long | $1,500 |

The short call at $7,575 pays for nearly half the long call. You’ve reduced your cost and your maximum loss — in exchange for capping your profit at $3,500.

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,400 | −$1,500 (max loss) |

| 7,500 (entry) | −$1,500 (max loss) |

| 7,525 (long strike) | −$1,500 (max loss) |

| 7,540 (breakeven) | $0 |

| 7,550 | +$1,000 |

| 7,575 (short strike) | +$3,500 (max profit) |

| 7,650 | +$3,500 (max profit) |

Below the long strike ($7,525), both calls expire worthless and you lose the full net debit. Above the short strike ($7,575), both calls are in the money and their gains net to the full spread width — $3,500. Between the two strikes, the P&L transitions linearly.

The Spread vs The Single Leg

The bull call spread is always compared to the plain long call on the same lower strike. Here’s how they differ with the same entry price:

| Bull Call Spread | Long Call (7,525 only) | |

|---|---|---|

| Net premium paid | $1,500 | $2,900 |

| Breakeven | 7,540 | 7,554 |

| Max loss | $1,500 | $2,900 |

| Max profit | $3,500 (capped at 7,575) | Unlimited |

| P&L if SPX → 7,558 | +$3,300 | +$1,900 |

| P&L if SPX → 7,650 | +$3,500 | +$15,100 |

The spread costs roughly half as much, has a lower breakeven, and outperforms the naked long call in moderate rally scenarios. At SPX 7,558 — a 58-point (0.77%) move — the spread returns +$3,300 on $1,500 invested (+220%), while the naked long call returns +$1,900 on $2,900 invested (+66%). The spread wins by a wide margin.

The long call wins only when SPX moves well beyond the short strike. At SPX 7,650, the naked long call returns +$15,100 while the spread is capped at $3,500. The long call’s advantage only materialises in a large move.

The practical question: how far do you genuinely expect SPX to move? If the answer is “a lot,” use the long call. If the answer is “a specific, moderate amount,” the spread makes more capital-efficient sense. Most directional trades on SPX should use spreads.

Understanding the Greeks

The bull call spread’s Greeks are the net of both legs — long call minus short call.

Net Delta (positive, ~+0.25 to +0.45): The long call has positive delta; the short call subtracts negative delta. The net is positive but smaller than a naked long call — you participate in upside moves, just proportionally less. As SPX rises above both strikes, the deltas converge and net delta approaches zero — the position is fully “locked in” at max profit and no longer moves much. Below the long strike, the short call becomes irrelevant (both OTM) and delta is governed solely by the long call.

Net Theta (negative — time works against you): Both legs decay with time, but the short call’s theta partially offsets the long call’s theta. The net position still has negative theta — a debit spread always decays against you — but it decays more slowly than a naked long call. If SPX stays flat, you lose money, but at a slower rate than if you had bought the call alone.

Net Vega (positive, but muted): Rising IV benefits the long call but hurts the short call. The net is still positive — the spread benefits modestly from rising volatility — but the effect is weaker than a single long call. IV crush is less damaging to a spread than to a naked long call for the same reason.

Net Gamma (complex — near zero above short strike): Below the long strike, the short call is deep OTM and gamma comes entirely from the long call. Between the two strikes, positive gamma accelerates gains as SPX rises. Above the short strike, both calls have similar gamma, and the net approaches zero — the position has reached max profit and doesn’t accelerate further. This bounded gamma profile makes the spread more predictable near expiration than a single long call.

Net Rho (positive but small): Both calls have positive rho (calls benefit from rising rates), but the long call’s rho is slightly larger than the short call’s (lower strike = higher sensitivity). The net is small positive rho. Negligible for 30 DTE positions.

Trade Management & Adjustments

Taking profits early: Don’t hold to expiration. If the spread is worth $2,600 out of a $3,500 maximum (75% of max profit), close it. The remaining $900 of theoretical profit requires holding through gamma risk with SPX pinned near or above the short strike. Most experienced spread traders close at 50–75% of max profit and redeploy.

Closing to avoid assignment risk: SPX options (European-style) cannot be assigned early — they can only be exercised at expiration. This is one reason experienced traders prefer SPX over SPY for vertical spreads. On equity options (American-style), the short leg carries early assignment risk if it goes deep ITM. Always verify the exercise style of what you’re trading.

Rolling up and out: If SPX rallies quickly and the spread approaches max profit early in the cycle, you can close the existing spread and roll up — open a new spread at higher strikes and/or a later expiration. This extends the trade and collects additional premium, effectively “locking in” a portion of the gain while maintaining a bullish position.

When the trade is losing: If SPX fails to move and the spread approaches max loss with more than a week to expiration, decide whether your thesis is still intact. If it is, hold — theta is now working in your favour on the short call leg, and a late rally is still possible. If the thesis is broken, close the spread and limit the loss. Never hold a losing spread to expiration on hope alone.

What to avoid:

- Entering the spread when IV is very low. The short call collects less premium, making the net debit higher relative to the spread’s max value.

- Using very narrow spreads (10–15 SPX points). The commissions and bid-ask spread eat a meaningful fraction of the max profit.

- Letting the short strike sit deep ITM into expiration week without an exit plan.

Real-World Example

The trade: Non-farm payroll data is due in 2 weeks. The trader expects a strong jobs print to push equities modestly higher, but doesn’t expect a large sustained rally. A moderate move into the 7,550–7,575 range feels probable. The spread is a better fit than a naked call.

- Buy: 1 SPX 7,525 Call (30 DTE) for $23.00 = $2,300

- Sell: 1 SPX 7,575 Call (30 DTE) for $9.00 = $900

- Net debit: $14.00 = $1,400

- Max profit: $3,600 at SPX ≥ 7,575

- Breakeven: 7,539

What happened:

Payrolls came in above expectations. SPX rallied from 7,495 to 7,558 over the 30 days — a solid 63-point move. The rally was real but stopped well short of the 7,575 short strike.

At expiration, SPX closed at 7,558.

- Long 7,525 call: intrinsic value = $33 → worth $3,300

- Short 7,575 call: OTM, expired worthless

- Net P&L: $3,300 − $1,400 = +$1,900

The comparison:

| Bull Call Spread | Long Call (7,525 only at $23) | |

|---|---|---|

| Capital deployed | $1,400 | $2,300 |

| SPX at expiry | 7,558 | 7,558 |

| Position value | $3,300 | $3,300 |

| P&L | +$1,900 (+136%) | +$1,000 (+43%) |

The spread outperformed the naked long call on both absolute return and return on capital. This is the sweet spot for the bull call spread — a moderate, directed rally that lands inside the spread zone.

Had SPX closed at 7,650 instead:

- Spread: +$3,600 (capped)

- Long call 7,525: ($125 intrinsic − $23 paid) × 100 = +$10,200

In a large rally, the naked call wins decisively. The spread sacrificed meaningful theoretical upside in exchange for a lower entry cost and lower risk.

When to Use This Strategy

Best conditions:

- You have a specific price target in mind — you can articulate where SPX is going, not just “up”

- The expected move is moderate (1–3% over 30 days), not a breakout scenario

- IV is moderately elevated — the short call collects meaningful premium to reduce your net debit

- You want to put on a bullish trade but can’t afford or don’t want to risk a full long call premium

Avoid when:

- You expect a large, fast rally — the cap bites too hard

- IV is very low — the short call collects barely any premium and the spread offers little advantage over a naked long call

- You’re using the spread as a way to “afford” a trade you wouldn’t otherwise take — smaller cost does not mean smaller risk per dollar invested

Ideal VIX level: 15–25. Below 15, the short call premium is thin and the spread’s advantage shrinks. Above 25, you’re taking on vega risk in both directions — consider whether a spread is the right structure for a high-IV environment.

Strategy Ladder — Next Steps

Came from: Long Call — the single-leg version of this trade, without the upside cap.

The bearish equivalent: → Bear Put Spread — buy a put, sell a lower-strike put. Same debit structure, opposite direction.

The credit spread alternative: Want a bullish position where time is on your side? → Bull Put Spread — sell a put spread instead of buying a call spread. Same directional bias, credit instead of debit.

Natural progression:

- Combine a bull call spread and a bear put spread → Iron Condor — non-directional premium collection between defined strikes

- Want to reduce the cost even further? → Ratio Spreads (coming soon at Level 3) — sell more options than you buy, zero-cost entry at the expense of tail risk

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.