30-Second Summary

| Legs | Buy 1 deep ITM LEAPS call (180+ DTE) · Sell 1 OTM short-dated call (30–45 DTE) |

| Cost | Net debit — the LEAPS call dominates the cost |

| Max Profit (per cycle) | Credit from the short call + LEAPS appreciation up to the short strike |

| Max Loss | Net debit paid for the LEAPS (if underlying collapses to zero) |

| Breakeven | LEAPS cost − all credits collected over time |

| Ideal Outcome | Underlying grinds higher toward the short strike each month |

| Avoid When | IV is very low — the short call generates little income; or you expect a fast large move up |

The PMCC (Poor Man’s Covered Call) replicates the payoff of a covered call at a fraction of the capital cost. Instead of buying 100 shares of SPX exposure (which is not practical), you buy a deep ITM LEAPS call that behaves like owning the underlying — then sell a short-dated OTM call against it each month for income.

What Is a PMCC?

A traditional covered call requires owning 100 shares and selling a call against them. For most indices like SPX, that means hundreds of thousands of dollars in capital. The PMCC replaces the shares with a deep ITM LEAPS call (delta 0.80+), which closely tracks the underlying at a fraction of the cost.

The core mechanics:

- The long LEAPS acts as a stock surrogate. Deep ITM, high delta, long-dated — it captures most of the underlying’s movement.

- The short near-dated call generates monthly income. When it expires worthless, the trader sells another one. This rolling process reduces the effective cost of the LEAPS over time.

The capital advantage: A LEAPS call costs far less than 100 shares. The income from repeatedly selling short calls can eventually reduce the cost basis to near zero — turning the long call into a “free” position.

The critical rule: The short call strike must always be above the long LEAPS strike. If the short call is exercised, you must be able to deliver the long call’s intrinsic value — otherwise you’re in a naked short situation.

Setup & Execution

| Leg | Action | Strike | DTE | Premium | Cash Flow |

|---|---|---|---|---|---|

| Long LEAPS Call | Buy 1 | 7,350 | 180 | $280.00 | −$28,000 |

| Short Near-Term Call | Sell 1 | 7,600 | 30 | $36.00 | +$3,600 |

| Net | −$24,400 debit |

- LEAPS strike: 7,350 (deep ITM by 150 pts, delta ≈ 0.85)

- Short call strike: 7,600 (OTM by 100 pts)

- Strike gap: 250 pts — always keep the short above the long

- Initial cost basis: −$24,400

- After 6 monthly rolls at $3,600/cycle: −$24,400 + $21,600 = −$2,800 residual basis

- Lower breakeven (first cycle): ~7,475 (where LEAPS appreciation offsets the net debit and short call credit)

Execution note: Some platforms display this as a diagonal spread. Always verify that the short call strike is above the long call strike. The short leg must be in the same account as the long to avoid margin treatment as a naked call.

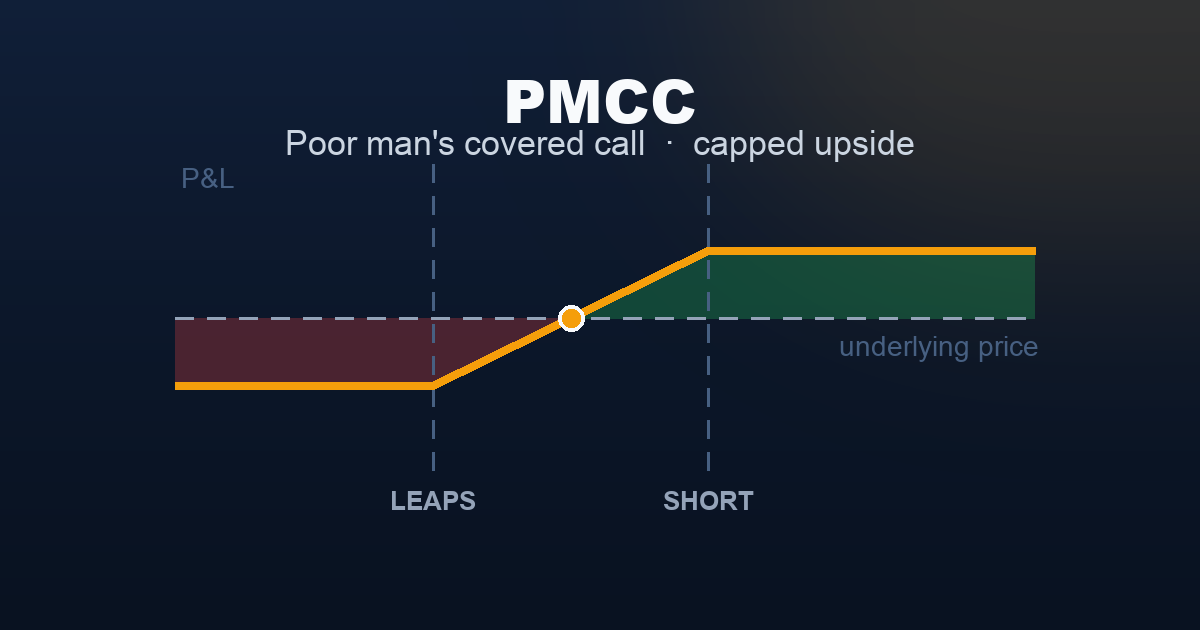

The Payoff Diagram

Payoff shown at the first short call’s expiration (30 DTE). With each subsequent roll, the breakeven shifts lower as credits accumulate.

| SPX at Short Expiry | Approx. LEAPS Value | Short Call Cost | Net P&L |

|---|---|---|---|

| 7,350 | ~$25,200 | $0 | −$2,800 |

| 7,400 | ~$25,900 | $0 | −$2,100 |

| 7,450 | ~$26,600 | $0 | −$1,400 |

| 7,475 | ~$27,400 | $0 | ~$0 ← breakeven |

| 7,500 | ~$28,000 | $0 | +$1,600 |

| 7,550 | ~$30,200 | $0 | +$3,400 |

| 7,600 | ~$32,000 | $0 | ~+$4,000 ← near peak |

| 7,650 | ~$37,000 | −$5,000 | ~+$4,000 ← flattens |

LEAPS values are approximate; actual P&L depends on remaining IV and time value in the long call.

Why “Poor Man’s”?

A standard covered call on SPX requires owning 100 “shares” of SPX exposure. Because SPX cannot be directly owned as shares, institutional traders use futures or ETFs like SPY. The PMCC replicates this at a fraction of the capital by substituting the shares with a deep ITM LEAPS call.

Capital comparison:

- Owning SPX equivalent (via SPY): ~$750,000 (100 shares at $750)

- PMCC long LEAPS: ~$28,000 (this example)

- Capital reduction: ~96%

But this efficiency comes with trade-offs:

- The LEAPS has a finite life — it expires, unlike actual shares

- The LEAPS loses time value (theta) over time — shares don’t

- If IV collapses, the LEAPS can lose value even if the underlying stays flat

- Assignment risk on the short call requires careful management

Understanding the Greeks

| Greek | Net at Entry | What It Means |

|---|---|---|

| Delta | ~+0.60–0.75 | Long delta from LEAPS minus short delta of near call; moderately bullish |

| Gamma | Near zero | Long LEAPS gamma and short near-term gamma partially offset each other |

| Theta | Mildly positive | Near-term short call decays faster than the far-dated LEAPS; slight daily income |

| Vega | Positive | LEAPS has higher vega than the short call; benefits from IV expansion |

| Rho | Positive | Far-dated LEAPS is more sensitive to interest rate changes |

The vega risk: Because the LEAPS has much higher vega than the short near-term call, a sharp IV collapse can hurt the position even if the underlying rises. This is most common after a major market event resolves. Entering the LEAPS in low-IV environments reduces this risk.

Trade Management

- Roll the short call at 50–80% profit or 5–10 DTE. Close the expiring short call and sell the next month’s call at the same or higher strike. Each roll credits your cost basis.

- Adjust the short call strike as the underlying rises. If SPX moves from 7,500 to 7,580, roll the 7,600 short call to a 7,650 call. Collect the credit difference and maintain upside room.

- Never let the short call go deep ITM without rolling. If SPX surges past the short strike and you hold to expiration, you’ll face assignment. While your long LEAPS covers it, you lose the upside gain above the short strike. Roll before expiry.

- Track your effective cost basis. After each roll, subtract the credit received. When your total collected credits approach the initial LEAPS cost, you effectively own the long call for free.

- Exit the LEAPS with 60–90 DTE remaining. As the LEAPS approaches expiration, its time value erodes rapidly. Roll to a new far-dated LEAPS (same or higher strike) before the time value erosion accelerates.

Real-World Example

Scenario A — Rolling the Income (Win over 4 months): SPX at 7,500. Buy 7,350 LEAPS (180 DTE) for −$28,000. Sell 7,600 call (30 DTE) for +$3,600.

- Month 1: SPX 7,520. Short expires worthless. Roll → sell next 7,600 call +$3,300.

- Month 2: SPX 7,560. Roll +$3,000.

- Month 3: SPX 7,590. Roll +$2,700.

- Month 4: SPX 7,610. Short goes slightly ITM — roll to 7,650 call +$2,900.

Total credits collected: $15,500. Effective LEAPS cost: $28,000 − $15,500 = $12,500. The position now has substantial cushion and the LEAPS (now worth ~$37,000 with SPX at 7,610) generates a large unrealized gain.

Scenario B — Crash and Roll (Managed Loss): Same entry. One week in, an unexpected policy event drops SPX to 7,360.

The short 7,600 call collapses to near $0 (effectively a full credit). The LEAPS 7,350 call: SPX is now at 7,360, just $10 above the LEAPS strike. Value drops from $28,000 to ~$5,700 (time value preserved, intrinsic nearly zero).

P&L: $5,700 − $28,000 + $3,600 = −$18,700

The trader now rolls: sells the next 7,400 call for +$2,200. The process continues — either SPX recovers and they earn back losses through rolls, or they eventually exit the LEAPS for whatever value remains.

When to Use

Use a PMCC when:

- You are moderately bullish over a multi-month horizon

- You want the income of a covered call without tying up equity capital

- IV is moderate (VIX 15–22) — the LEAPS is affordable and the short call generates reasonable income

- You are committed to actively managing the position over multiple cycles

Avoid a PMCC when:

- You expect a large, fast upside move — the short call will cap your gains

- IV is very low — the LEAPS time value is low, but the short call also generates little income

- You cannot monitor the position weekly — assignment on the short call requires prompt action

- The underlying is in a strong downtrend — the LEAPS will lose value faster than rolls can compensate

Strategy Ladder

| Direction | Strategy | Why |

|---|---|---|

| ← Simpler | Long Call | Pure bullish exposure, no active rolling required |

| ← Simpler | Diagonal Spread | Same structure, narrower strike gap, shorter LEAPS DTE |

| → This strategy | PMCC | Deep ITM LEAPS as stock surrogate; maximum capital efficiency |

| ↑ Related | Jade Lizard | Add a short put below to generate additional income |

| ↑ Related | Ratio Spread | Sell 2 near-term calls (more income, more risk) |

This content is for educational purposes only and does not constitute financial or investment advice. Options trading involves significant risk of loss. Always consult a qualified financial professional before trading.