30-Second Summary

| Legs | Sell 1 OTM put · Sell 1 OTM call · Buy 1 further OTM call (call spread cap) |

| Cost | Net credit (must exceed call spread width for no upside risk) |

| Max Profit | Total credit received — earned if underlying stays between the put and short call strike |

| Max Loss | Downside: unlimited below the lower breakeven (short put) |

| Breakeven | Lower only: short put strike − total credit ÷ 100 |

| Upside Risk | None — if total credit > call spread width, there is no upside loss |

| Ideal Outcome | Underlying stays between the short put and the short call at expiration |

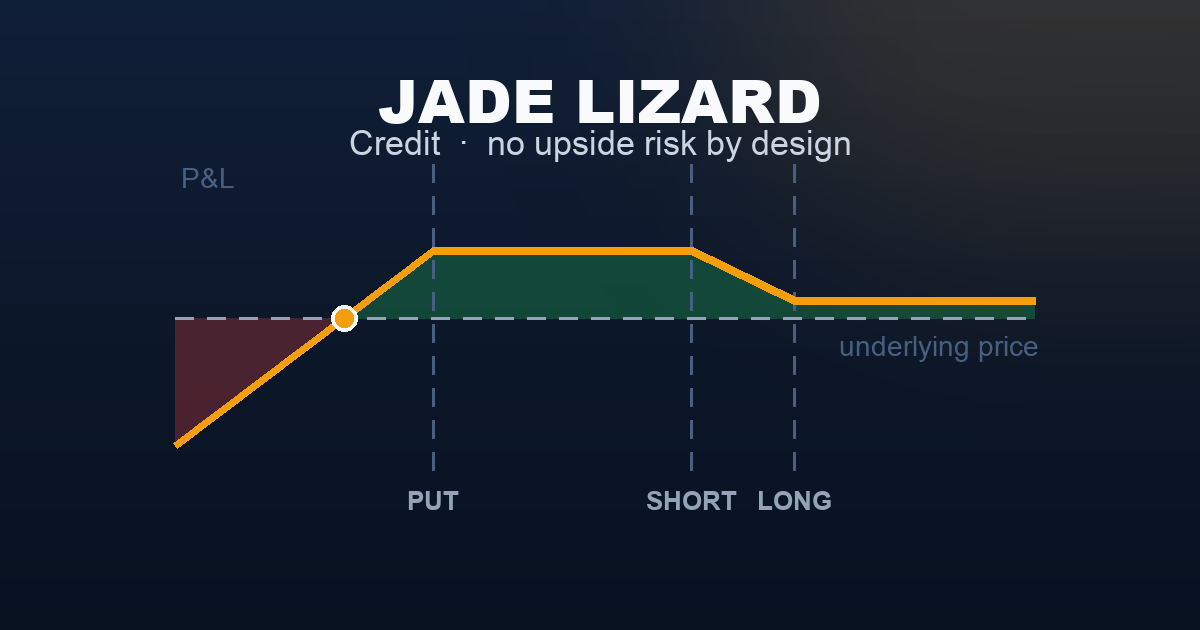

The Jade Lizard’s defining characteristic: by collecting a credit larger than the call spread’s maximum loss, you eliminate all upside risk entirely. You cannot lose money if the underlying goes up. You can only lose money if it goes down past the lower breakeven.

What Is a Jade Lizard?

The Jade Lizard combines two seller strategies into a single three-legged trade:

- Short OTM put — generates income; creates downside risk

- Short OTM call spread (sell a call, buy a higher-strike call) — generates income; the long call caps upside risk

The key condition: The total credit from all three legs must exceed the width of the call spread. When this holds, the worst outcome above the long call strike is still a net profit.

Example of why it works:

- Call spread width: 50 pts = $5,000 max loss on the call spread

- Total credit collected: $5,500

- At expiry above the long call: call spread max loss = −$5,000; total credit = +$5,500; net = +$500 profit

This is not magic — you are still short the put and face full downside exposure below the lower breakeven. The Jade Lizard simply redirects all the risk to one side (down) while eliminating the other (up).

Setup & Execution

| Leg | Action | Strike | DTE | Premium | Cash Flow |

|---|---|---|---|---|---|

| Short Put | Sell 1 | 7,450 | 30 | $45.00 | +$4,500 |

| Short Call | Sell 1 | 7,550 | 30 | $18.00 | +$1,800 |

| Long Call (cap) | Buy 1 | 7,600 | 30 | $8.00 | −$800 |

| Net | +$5,500 credit |

- Total credit: +$5,500

- Call spread width: 7,600 − 7,550 = 50 pts = $5,000

- Upside check: $5,500 credit > $5,000 call spread → no upside risk (✔)

- Max profit: +$5,500 (underlying stays between 7,450 and 7,550 at expiry)

- At/above 7,600: +$5,500 − $5,000 = +$500 (small profit, no loss)

- Lower breakeven: 7,450 − ($5,500 ÷ 100) = 7,395

- Below 7,395: losses grow $100 per point decline

Execution note: Check the “no upside risk” condition before placing the trade. If the credit does not exceed the call spread width, you are exposed to losses on both sides — which is a different (and less favorable) risk profile. Adjust by widening the put strike, tightening the call spread, or choosing a higher-IV environment.

The Payoff Diagram

| SPX at Expiry | Short 7,450 Put | Short 7,550 Call | Long 7,600 Call | Net P&L |

|---|---|---|---|---|

| 7,350 | −$10,000 | $0 | $0 | −$4,500 |

| 7,395 | −$5,500 | $0 | $0 | $0 ← lower BE |

| 7,450 | $0 | $0 | $0 | +$5,500 |

| 7,500 | $0 | $0 | $0 | +$5,500 |

| 7,550 | $0 | $0 | $0 | +$5,500 ← max profit |

| 7,600 | $0 | −$5,000 | $0 | +$500 |

| 7,650 | $0 | −$10,000 | +$5,000 | +$500 |

The +$500 floor above 7,600 confirms there is no upside risk in this trade.

The Seller’s Edge: No Upside Risk

Most income strategies have bilateral risk: an iron condor loses on both sides if the market moves too far. The Jade Lizard’s edge is structural asymmetry: by construction, the upside is always profitable (or at worst, breakeven).

Why does this matter? The most dangerous scenario for short-premium sellers is a rapid rally after entering a bearish or neutral position. The Jade Lizard completely sidesteps this risk. The only direction that hurts you is down.

What you are really selling: You are selling the market’s fear of a downside move (via the short put) while capping your exposure to an unexpected rally. If you are bullish-to-neutral and want to collect premium, the Jade Lizard is structurally more forgiving than an iron condor.

Understanding the Greeks

| Greek | Net at Entry | What It Means |

|---|---|---|

| Delta | Positive (+0.20 to +0.35) | Mildly bullish; short put adds positive delta |

| Gamma | Negative | Loses value as underlying moves rapidly (especially downward) |

| Theta | Strongly positive | All three legs benefit from time decay |

| Vega | Negative | Benefits from IV contraction; enter in elevated IV |

| Rho | Near zero | Minimal interest rate sensitivity |

The put’s delta dominates. The short put contributes significant positive delta to the position. The short call spread partially offsets this. Net: you are mildly long the underlying, which aligns with the strategy’s neutral-to-bullish bias.

IV environment matters. In high-IV environments (VIX 20+), the short put collects more premium, making it easier to satisfy the no-upside-risk condition. In low-IV environments, the credit may not exceed the call spread width, changing the risk profile entirely.

Trade Management

- Take profit at 50–75% of the total credit. Close all three legs when you have captured $2,750–$4,125 of the $5,500 max profit. This avoids holding through final-week gamma risk near the put strike.

- Roll the put down if IV spikes. If the underlying drops and IV surges, the short put’s value grows. Rolling it to a lower strike and further DTE collects additional credit and buys time.

- No action required on the upside. If the underlying rallies past 7,600, the net P&L is +$500 regardless of how far it goes. This is the structural advantage — you can ignore upside moves entirely.

- Close if underlying breaks the lower breakeven. Below 7,395, losses grow linearly. Exit or roll if SPX approaches this level with significant DTE remaining.

Real-World Example

Scenario A — Quiet Month (Win): SPX opens at 7,500, VIX at 20. Jade Lizard entered for +$5,500. SPX closes the month at 7,518 — between the short put (7,450) and short call (7,550).

All three options expire worthless. P&L = +$5,500 (full credit kept).

The trader collects max profit with no management required.

Scenario B — Surprise Rally (Still a Win!): Same entry. FOMC announces an unexpected 50bp rate cut. SPX surges to 7,680 by expiry.

- Short put 7,450: expires worthless (+$4,500 kept)

- Short 7,550 call: worth −$13,000

- Long 7,600 call: worth +$8,000

- Call spread net: −$5,000 (max loss on call spread)

- Total P&L: +$5,500 − $5,000 = +$500

Despite a 180-point rally, the position profits. This is the no-upside-risk principle at work.

Scenario C — Selloff (Loss): Same entry. Unexpected tariff news drops SPX to 7,360.

- Short put 7,450: worth −$9,000 (loss)

- Short/long call spread: both expire worthless

- P&L = +$5,500 − $9,000 = −$3,500

When to Use

Use a Jade Lizard when:

- You are neutral to mildly bullish and want to collect premium

- IV is elevated (VIX 18+) — makes it easier to satisfy the no-upside-risk condition

- You want no upside risk — if you’re worried about a sudden rally, the Jade Lizard protects you

- You prefer to manage risk on only one side (downside) rather than both

Avoid a Jade Lizard when:

- IV is so low that you cannot collect enough credit to exceed the call spread width

- You expect a significant downside move — the short put creates unlimited downside exposure

- You cannot monitor the position if the underlying approaches the lower breakeven

Strategy Ladder

| Direction | Strategy | Why |

|---|---|---|

| ← Simpler | Short Strangle | Sell put + sell call, no call-spread cap, bilateral unlimited risk |

| ← Simpler | Iron Condor | Fully defined risk on both sides (add a long put below the short put) |

| → This strategy | Jade Lizard | No upside risk; downside risk capped only by your short put |

| ↑ Related | Ratio Spread | Sell 2 calls, buy 1 — unlimited upside risk but higher call-side credit |

| ↑ Related | PMCC | Income from selling calls against a long LEAPS position |

This content is for educational purposes only and does not constitute financial or investment advice. Options trading involves significant risk of loss. Always consult a qualified financial professional before trading.