30-Second Summary

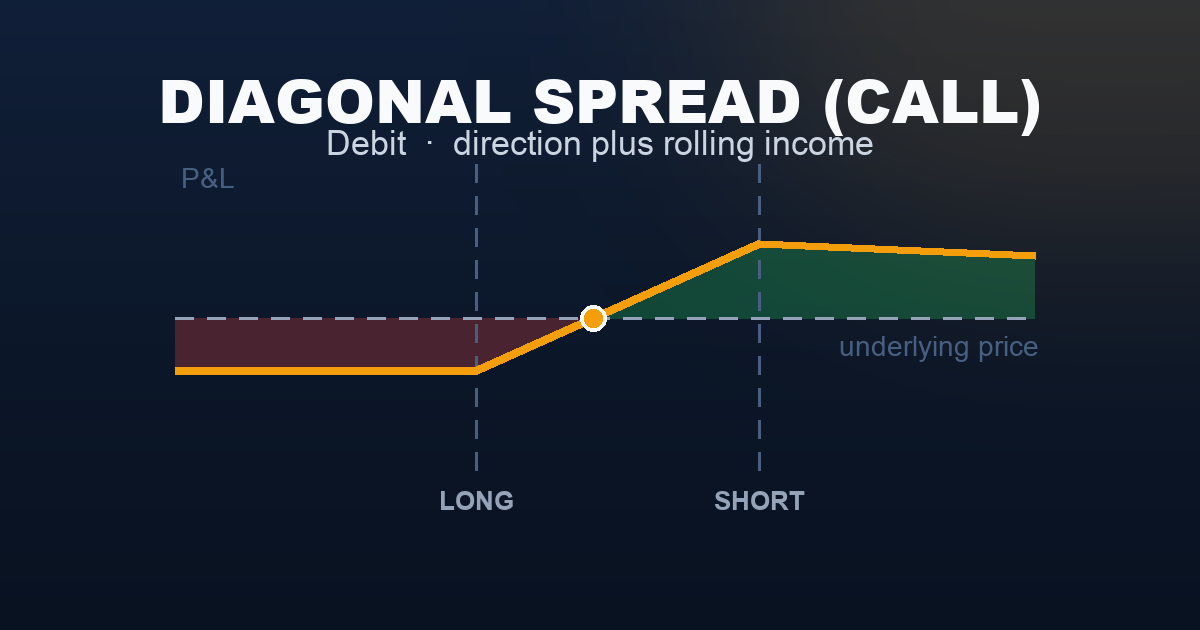

| Legs | Buy 1 longer-dated lower-strike call · Sell 1 shorter-dated higher-strike call |

| Cost | Net debit (the far-dated long costs more than the near-dated short) |

| Max Profit | Approximated near the short strike when the near-dated call expires worthless |

| Max Loss | Net debit paid (if underlying collapses and long call loses all value) |

| Breakeven | One lower breakeven; profits on both sides of the short strike |

| Ideal Outcome | Underlying rises moderately toward the short strike; IV stays stable or rises |

| Avoid When | IV is very low — the long call is cheap but the short generates little premium |

The diagonal spread combines the directional exposure of a calendar spread with the capital efficiency of a vertical spread. It is the foundation of the PMCC strategy and a core tool for traders who want to sell premium repeatedly against a longer-dated long position.

What Is a Call Diagonal Spread?

A call diagonal spread involves buying a longer-dated call at a lower strike and selling a shorter-dated call at a higher strike. Unlike a calendar spread (same strike, different expirations) or a vertical spread (same expiration, different strikes), the diagonal differs on both dimensions.

Why use it? The long call gives you directional exposure over a longer time horizon. The short call generates income in the near term, reducing your cost basis. After the short call expires (or is closed), you can sell another short call against the long — turning it into a rolling income strategy.

Key insight: The payoff at the short call’s expiration depends on how much time value remains in the long call. This makes the diagonal spread’s payoff curve approximate — it changes with IV and time. The diagram below shows typical values based on standard assumptions.

Two directions:

- Call diagonal (shown here) — bullish bias; long lower-strike call, short higher-strike call

- Put diagonal — bearish bias; long higher-strike put, short lower-strike put

Setup & Execution

| Leg | Action | Strike | DTE | Premium | Cash Flow |

|---|---|---|---|---|---|

| Long Call | Buy 1 | 7,500 | 90 | $137.00 | −$13,700 |

| Short Call | Sell 1 | 7,550 | 30 | $44.00 | +$4,400 |

| Net | −$9,300 debit |

- Long strike / DTE: 7,500 / 90 (ATM, far-dated)

- Short strike / DTE: 7,550 / 30 (OTM, near-dated)

- Strike difference: +50 points (bullish bias)

- Net debit: −$9,300

- Goal: Sell the 7,550 call repeatedly as each 30-day cycle expires, reducing the $9,300 cost basis toward zero over time

Strike selection rules:

- Long call: ATM or slightly OTM for leverage; or ITM for higher delta (less time value bleed)

- Short call: 1–2 strikes OTM on the near-dated expiration; match the long call’s strike or go slightly higher

- DTE ratio: short 20–45 DTE; long at least 2× the short DTE (so 60–90+ DTE)

Execution note: Enter as a diagonal order on your platform. The fill is sensitive to the bid-ask on both legs — use limit orders.

The Payoff Diagram

Note: The payoff below is approximate at the short call’s expiration. Exact P&L depends on remaining IV and time value in the long call.

| SPX at Short Expiry | Approximate P&L | Notes |

|---|---|---|

| 7,350 | ~−$3,000 | Long call far OTM, little time value left |

| 7,400 | ~−$1,500 | Approaching breakeven |

| 7,430 | ~$0 | Lower breakeven |

| 7,500 | ~+$3,000 | Long call ATM, 60 DTE time value intact |

| 7,550 | ~+$4,300 | Short expires worthless, long is ITM ← near peak |

| 7,600 | ~+$3,000 | Short leg costs; long partially offsets |

| 7,650 | ~+$1,500 | Net delta of two legs converges toward zero |

Exact values depend on remaining IV in the long call at the short expiry date.

Buyer vs. Seller Reality

The diagonal spread sits between the two worlds. You are long a far-dated call (buyer behavior) and short a near-dated call (seller behavior). The balance of these two forces determines your Greek profile at any moment.

Early in the trade (many days until short expiry): The short call’s theta benefits you most. You are effectively being paid to wait.

Near short expiry: Gamma risk from the short call dominates. If the underlying is near the short strike, the short call’s value fluctuates sharply. Traders typically close or roll 5–10 DTE before expiration.

After the short expires: You own the long call outright. You can sell another short call against it (rolling the diagonal), hold it outright, or exit. The rolling income strategy is what makes the diagonal a repeatable structure.

Understanding the Greeks

| Greek | Net at Entry | What It Means |

|---|---|---|

| Delta | Positive (~+0.35–0.45) | Moderately bullish; rises as underlying moves toward the long strike |

| Gamma | Near zero (complex) | Long gamma from far call, short gamma from near call; net depends on proximity to strikes |

| Theta | Mildly positive | The near-dated short call decays faster than the far-dated long — theta works for you |

| Vega | Positive | The far-dated long call is more vega-sensitive; IV expansion helps overall |

| Rho | Modestly positive | Far-dated long call has higher rho sensitivity to interest rates |

The vega mismatch: The far-dated long call has higher vega than the near-dated short call. A rise in IV benefits you more than it hurts you — this is the opposite of a calendar spread where the vega is closer to neutral. Enter in low-to-moderate IV environments.

Trade Management

- Roll the short call at 50–80% profit or 5–10 DTE. When the near-dated call has lost most of its value, close it and sell the next cycle’s call at the same or higher strike. This is the core of the rolling strategy.

- Target a net debit reduction of 30–50% per roll. Each sold call reduces your cost basis. After 2–3 rolls, the long call may be largely paid for by the income generated.

- Adjust the short strike as the underlying moves. If SPX surges past the short strike, roll the short call up-and-out (to a higher strike and/or longer DTE) to reduce assignment risk and collect more premium.

- Exit if IV collapses severely. A crash in IV deflates the long call’s time value, potentially turning a positive P&L into a loss. Close both legs and reassess.

- Never let the short expire in the money without rolling first. Assignment on a short SPX call would create an unhedged position. Close or roll before expiry.

Real-World Example

Scenario A — The Grind Higher (Win): SPX at 7,500, VIX 18. Buy 7,500 call (90 DTE) −$13,700, sell 7,550 call (30 DTE) +$4,400. Net: −$9,300.

Month 1: SPX drifts to 7,535. The short 7,550 call expires at $0. The 7,500 call (now 60 DTE) is worth ~$11,800.

Month 1 interim P&L: $11,800 − $13,700 + $4,400 = +$2,500

The trader rolls: sells the 7,560 call (30 DTE) for +$4,000. Net cost basis is now: $9,300 − $4,400 (month 1) − $4,000 (month 2) = $900.

After two rolls, they own the long call nearly for free.

Scenario B — The Gap Down (Loss): Same entry. An unexpected tariff announcement drops SPX to 7,370 in two sessions.

The short 7,550 call collapses to ~$1 (profit on the short, nearly full credit kept). But the long 7,500 call drops from $13,700 to ~$6,000 (IV partially offsets price drop, but intrinsic is zero).

P&L: $6,000 − $13,700 + $4,400 = −$3,300 (limited by the long call’s remaining time value).

The trader holds — the long call has 60 DTE remaining. If SPX recovers, the position can still profit. If not, they roll again at a lower short strike.

When to Use

Use a diagonal spread when:

- You are moderately bullish and want directional exposure with income

- You plan to roll the short call multiple times — the trade is a process, not a one-shot bet

- IV is moderate (VIX 15–22) — the long has enough value and the short generates reasonable credit

- You want defined risk without tying up full long-call capital

Avoid a diagonal spread when:

- IV is very low — the short leg generates minimal premium; consider a straight long call instead

- You expect a large, fast move — the short call caps your near-term upside

- You cannot commit to active management over multiple expiration cycles

Strategy Ladder

| Direction | Strategy | Why |

|---|---|---|

| ← Simpler | Long Calendar Spread | Same strike, different DTE — pure theta play without directional tilt |

| ← Simpler | Long Call | Simple directional bet, no management required |

| → This strategy | Diagonal Spread | Directional + rolling income; requires active management |

| ↑ Complex | PMCC | Deep ITM LEAPS as the long leg — the institutional version of this trade |

This content is for educational purposes only and does not constitute financial or investment advice. Options trading involves significant risk of loss. Always consult a qualified financial professional before trading.