30-Second Summary

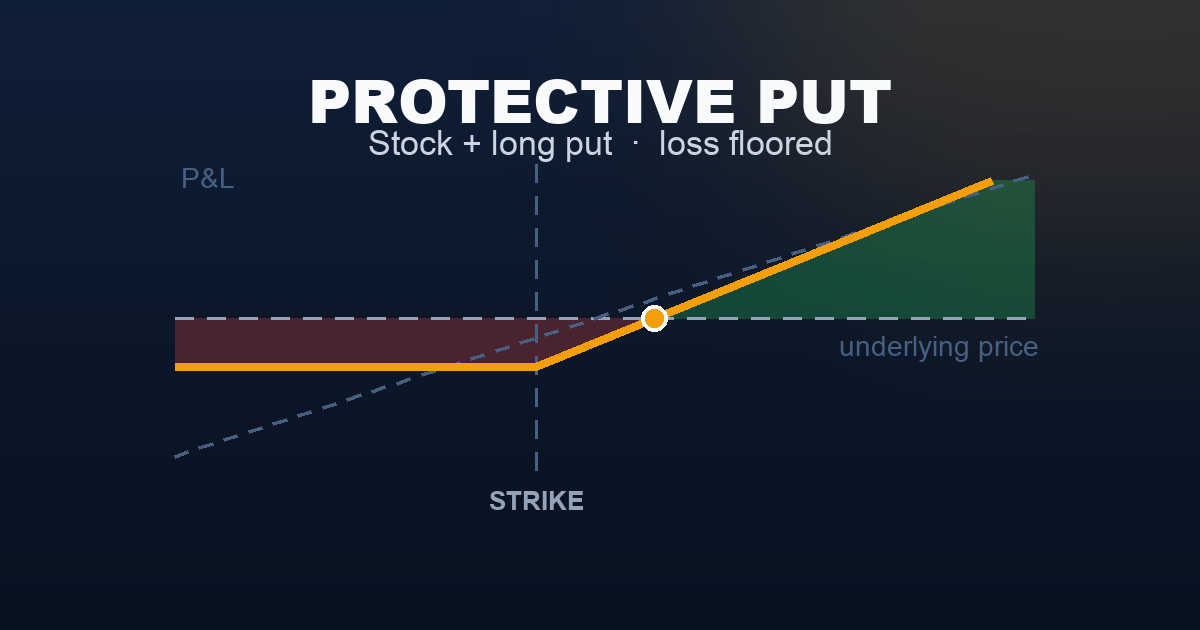

A protective put is portfolio insurance. You own stock and buy a put option below the current price. If the stock rises, you keep all the gains — the put expires worthless and the premium you paid is the cost of the coverage. If the stock falls sharply, the put activates and limits your loss to a defined maximum, no matter how far the stock drops.

This is a buyer’s strategy. You are paying for certainty. Theta works against you — every day the stock stays above your strike, the put loses value toward zero. The trade-off is explicit: you sacrifice some return every month (the premium) in exchange for a known, capped worst-case outcome. Whether that trade is worth making depends entirely on the size of the risk you’re carrying and the cost of the premium.

What Is a Protective Put?

A protective put combines two positions: 100 shares of stock (or an ETF like SPY) that you already own, and 1 long put option on the same underlying. The put gives you the right to sell your shares at the strike price — creating a hard floor under your position.

Without the put, owning stock means accepting unlimited downside. SPY can fall 20%, 40%, or more — and you’re exposed to every dollar of that decline. The protective put caps that exposure. Below the strike, the put’s gains perfectly offset the stock’s losses. The net position stops losing money.

Think of it like buying homeowner’s insurance. You pay a premium every period. If nothing bad happens, the premium is gone — a cost of carrying the property. If a disaster strikes, the insurance pays out and caps your total loss. You would never say the premium was “wasted” just because your house didn’t burn down.

The protective put is sometimes called a married put when you buy the stock and the put at the same time, treating them as a single packaged trade. The mechanics are identical — the naming just reflects whether you had the stock first or entered both legs simultaneously.

The key phrase: your maximum loss is defined the moment you buy the put. That certainty has a cost. Everything else follows from that.

Setup & Execution

Legs:

- Leg 1: Own (or buy) 100 shares of the underlying

- Leg 2: Buy 1 put option below the current price

Strike selection:

- Deep out-of-the-money (OTM): Strike well below current price. Cheap premium, but only activates on a severe decline. This is “catastrophe insurance” — you accept a large loss before the put kicks in.

- Out-of-the-money (OTM): Strike moderately below current price. The most common choice. Balances cost versus protection level.

- At-the-money (ATM): Strike near current price. Most expensive but protection begins immediately from any decline.

Expiration selection:

- 30 DTE: Most practical for regular monthly protection. Premium cost is manageable, and you renew each month.

- 90+ DTE: Higher upfront cost but lower annualised cost (time premium is more efficient at longer tenors). Good for longer-term holders who don’t want to roll monthly.

- LEAPS (1+ year): Used by institutional investors and serious long-term holders. Lower annualised cost, significant upfront outlay.

SPY Example — Entry:

Trade:

- Own: 100 shares SPY @ $750 = $75,000 capital deployed

- Buy: 1 SPY $740 Put (30 DTE) for $7.00 = $700 premium paid

- Total effective cost: $750 + $7.00 = $757 per share

- Breakeven at expiry: $757 (need SPY to rise $7 to offset the put cost)

- Maximum loss (the floor): ($740 − $750) × 100 − $700 = −$1,700

No matter how far SPY falls — to $710, $670, or lower — the most you can lose on this position is $1,700. That certainty is what you paid $700 for.

What the premium buys you:

| Protected Position | Unprotected Stock | |

|---|---|---|

| Maximum loss | −$1,700 (defined) | Unlimited (stock to $0) |

| Breakeven at expiry | $757 | $750 |

| Monthly cost | $700 | $0 |

| Upside | Unlimited | Unlimited |

The only thing the protection costs you is the $700 premium and the $7 higher breakeven. The upside is completely intact.

The Payoff Diagram

| SPY at Expiry | P&L |

|---|---|

| $700 | −$1,700 (max loss — floor holds) |

| $720 | −$1,700 (max loss — floor holds) |

| $740 (strike) | −$1,700 (max loss — floor holds) |

| $750 (entry) | −$700 |

| $757 (breakeven) | $0 |

| $775 | +$1,800 |

Below the strike ($740), the payoff is completely flat. A crash to $700 and a drop to $740 both produce the same −$1,700 loss. The put is absorbing all additional decline below the strike.

Above the breakeven ($757), the position profits dollar-for-dollar with stock ownership. The upside is exactly the same as holding stock — only shifted right by the $7.00 premium cost.

The Cost of Protection

Understanding the protective put means being honest about its fundamental trade-off.

| Stock + Protective Put | Stock Only | |

|---|---|---|

| Maximum loss | −$1,700 (defined) | Unlimited |

| Maximum gain | Unlimited | Unlimited |

| Breakeven | $757 (need $7 rally) | $750 (flat to break even) |

| Theta | Enemy — put decays daily | N/A |

| Vega (crash scenario) | Friend — IV spike amplifies put gains | Hurt — high IV means fear in the market |

| Monthly cost | $700 | $0 |

The protection has real value, but it comes with a real cost. At $700 per month, protecting a $75,000 SPY position costs roughly 0.93% per month or ~11.2% per year. On a position returning 8–10% annually, consistently buying protective puts can turn a profitable position into a flat one.

This is why most long-term investors don’t buy protective puts continuously. The insurance premium erodes returns over time if the market doesn’t crash. But in the months that matter — when volatility spikes and markets fall sharply — the put becomes the most valuable thing in the portfolio.

The key consideration: VIX level at entry. When VIX is at 14.5 (as in this example), a $7 put is relatively cheap. The same put costs $11–$14 when VIX is at 25. Buying protection after the storm has already started is expensive. The optimal time to buy insurance is when markets are calm and VIX is low — which is also the time it feels least necessary.

Understanding the Greeks

Net Delta (~+0.65 for the combined position): Owning stock gives you delta of +1.0. The long $740 put has a delta of approximately −0.30 to −0.40 (negative for long puts). The combined position has a net delta of roughly +0.60 to +0.70 — you still benefit meaningfully from SPY rising, but with slightly less sensitivity than naked stock ownership. As SPY falls toward $740, the put’s delta increases toward −1.0, and the combined position’s net delta approaches zero — at that point, every dollar SPY drops is fully offset by the put. You’re hedged.

Theta (negative — your enemy): Every day that passes without a significant decline, the put loses value. For a 30 DTE protective put, theta costs roughly $5–$15 per day. If SPY stays flat for two weeks, you’ve already lost a significant portion of the $700 premium with no benefit. This ongoing cost is the explicit price of certainty — there is no way around it.

Vega (positive — especially powerful in a sell-off): This is the protective put’s most underappreciated feature. Long puts benefit from rising implied volatility. When markets crash, VIX spikes — and your put gains value from both the price decline (intrinsic value) and the volatility expansion (extrinsic value). A put that would be worth $10 in intrinsic terms alone might be worth $15 or $20 when VIX is elevated. The crash protection is even stronger than the payoff diagram suggests.

Gamma (positive — accelerates protection as SPY falls): The long put carries positive gamma, which increases as expiration approaches and the put moves toward the money. A sudden sharp drop in SPY produces a faster, larger gain on the put than a slow drift lower — positive gamma means the protection accelerates into the scenario where you need it most.

Rho (negative for long put): Rising interest rates slightly reduce the value of put options, which works marginally against you as the buyer. This is the same Rho effect described in the Long Put article — the right to sell at a fixed price is worth slightly less when rates are higher, as the present value of the strike decreases. In practice, Rho is negligible for 30 DTE protective puts and never drives the decision.

Trade Management & Adjustments

Rolling the put: As expiration approaches and the put retains value (if SPY is near or below the strike), you can roll the put forward — sell the existing put and buy a new one at the same or a different strike with a later expiration. Rolling locks in any gains from the expiring put and maintains continuous protection. The cost of rolling is the net premium you pay for the new contract minus any proceeds from closing the old one.

Letting it expire worthless: If SPY rallies and the put expires worthless, the premium is gone. This is the expected outcome most of the time, and it’s not a failure — it’s the cost of the coverage you held. Decide in advance whether to re-buy protection for the next period.

Taking the floor: If SPY falls sharply and the put is deep in the money, you face a choice: exercise the put (sell your shares at the strike), sell the put for its intrinsic value and keep the shares, or roll the put to a later expiration to extend the protection. The right choice depends on whether you want to remain long the stock.

Avoiding the panic premium: If SPY drops 10% in a week and VIX spikes to 35, your put is likely worth significantly more than its intrinsic value. Selling the put at elevated IV locks in the maximum benefit. Waiting until calm returns may reduce the extrinsic value you could have captured. This is the flip side of the vega advantage — capture it when it’s there.

The protective put is not a stop loss: A stop loss exits your position automatically at a trigger price. A protective put gives you a right to exit at the strike — but you choose when to exercise. The difference matters: a protective put allows you to hold through a crash and benefit from a subsequent recovery, while a stop loss locks in the loss immediately. They serve different purposes.

Real-World Example

The trade: A trader holds 100 shares of SPY at $754. Markets are at all-time highs and VIX is low. With a significant geopolitical event expected within 30 days, they decide to buy a month of protection.

- Own: 100 shares SPY @ $754

- Buy: 1 SPY $742 Put (30 DTE) for $6.50 → $650 paid

- Max loss: ($742 − $754) × 100 − $650 = −$1,850

- Breakeven: $754 + $6.50 = $760.50

What happened:

The geopolitical event came and went without incident. Markets shrugged it off and SPY drifted from $754 to $761 over the 30 days. The $742 put expired worthless.

Result: +$50 (stock +$700, put −$650)

The protection was not needed. The $650 premium is gone.

Without the put, the unprotected position would have returned +$700.

The protective put cost the trader $650 in return — a 93% reduction in the month’s gains — for protection that was never used.

This is the most common outcome. Most months, protective puts expire worthless. This is uncomfortable but expected — the same way you don’t regret car insurance because you didn’t crash this month.

The scenario that justifies it: Consider an alternative universe where the geopolitical event triggered a flash crash and SPY fell from $754 to $705 over the same 30 days.

| Protected (SPY + $742 Put) | Unprotected | |

|---|---|---|

| SPY falls to $705 | −$1,850 (floor held) | −$4,900 |

| Difference | — | $3,050 worse |

In the crash scenario, the $650 in protection absorbed $3,050 in additional loss. That is the asymmetric value of the protective put: the cost is capped (the premium), but the benefit is not.

When to Use This Strategy

Best conditions:

- You hold a long stock position and face a specific near-term risk event (earnings, election, economic data release, geopolitical uncertainty)

- VIX is low — protection is cheapest when markets are calm, before the risk materialises

- You want to keep your position through a volatile period but can’t tolerate an open-ended loss

- The position is large enough that the premium cost is small relative to the potential loss it prevents

Avoid when:

- VIX is already elevated — you’re buying expensive protection after the risk is priced in

- You plan to sell the stock soon anyway — the protection costs money you’re about to give up

- The stock is a small speculative position where the premium exceeds what you’d lose if the thesis failed

Ideal VIX level: Below 18. Below 15 is ideal. Above 25, protective puts become expensive enough that the annual cost can approach or exceed the expected return on the stock itself. The math of buying insurance after the storm has already arrived rarely works in your favour.

Strategy Ladder — Next Steps

Came from: New to options? Start with Introduction to Options Trading for the core framework. Familiar with put options? The Long Put is the same instrument used here — just without the underlying stock position.

The income alternative: Don’t need protection right now and want to generate income instead? → Covered Call — sell a call against your shares to earn premium in flat or slowly rising markets.

Combined strategy: Stack a covered call on top of the protective put and you have a Collar — defined risk on the downside, capped upside, with the covered call premium partially or fully paying for the put. The most capital-efficient form of stock protection.

Natural progression from here:

- Want defined risk on a new position without owning shares? → Cash-Secured Put — sell a put backed by cash to acquire shares at a discount

- Want portfolio-wide protection rather than per-position puts? → Index Put Hedging (coming soon at Level 3) — buying SPX puts to hedge a broad equity portfolio

- Ready for multi-leg defined risk strategies? → Level 2 — Intermediate Strategies

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.