30-Second Summary

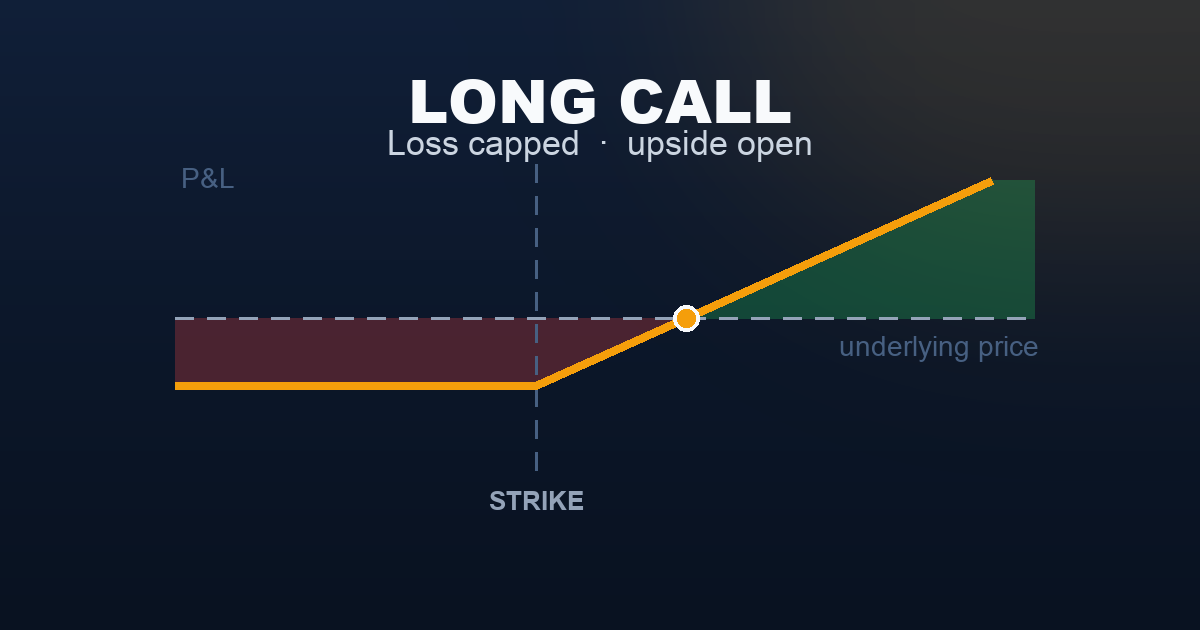

A long call is the simplest bullish bet in options. You pay a premium upfront for the right to buy the underlying at a set price (the strike) before expiration. If the underlying rises sharply above your strike, you profit. If it doesn’t — if it goes sideways, moves up slowly, or falls — you lose the entire premium you paid.

This is a buyer’s strategy. You are on the lottery-ticket side of the trade. The potential reward is theoretically unlimited, but the odds of winning are not in your favour. Understanding that trade-off is the entire point of this article.

What Is a Long Call?

When you buy a call option, you’re purchasing a contract that gives you the right — but not the obligation — to buy 100 shares of a stock (or the cash equivalent for an index like SPX) at a specific price (the strike price) on or before a specific date (expiration).

You pay a premium upfront. That’s your total maximum loss. In exchange, you get unlimited upside if the underlying moves far enough above your strike.

Think of it like buying a ticket to a concert that may or may not happen. You pay $50 for the ticket. If the concert happens and it’s amazing, you’re in. If it gets cancelled, you lose your $50 — nothing more, nothing less.

The key phrase: the underlying must move enough, in the right direction, fast enough to overcome the premium you paid. All three conditions must be true for a long call to be profitable.

Setup & Execution

Legs: Buy 1 call option

Strike selection:

- In-the-money (ITM): Strike below current price. More expensive, behaves more like owning the stock, higher probability of some profit but lower leverage.

- At-the-money (ATM): Strike near current price. Balanced risk/reward, popular choice.

- Out-of-the-money (OTM): Strike above current price. Cheap premium, but requires a large move to profit. Most long calls that retail traders buy are OTM — and most expire worthless.

Expiration selection:

- 0 DTE (same-day): Maximum leverage, maximum risk. The option will either make or lose its entire value today.

- 30–45 DTE: Common for directional trades. Gives time for the thesis to play out, but theta (time decay) is actively working against you from day one.

- 90+ DTE: Slower time decay. Better for longer-term directional views.

SPX Example — Entry:

Trade: Buy 1 SPX 7,550 Call (30 DTE) Premium paid: $36.00 per contract = $3,600 total cost Breakeven at expiry: 7,550 + 36 = 7,586

To make a dollar of profit, SPX must close above 7,586 at expiration — a move of 86 points (1.15%) from entry.

Understanding what you’re actually paying for:

The $36.00 premium is made up of two components:

| Component | What it means | Amount (approx.) |

|---|---|---|

| Intrinsic Value | How far the option is already in the money | $0 (OTM strike — none) |

| Extrinsic Value | Time value + implied volatility premium | $36.00 (all of it) |

Since the 7,550 strike is above the current price of 7,500, there is zero intrinsic value — you are paying entirely for the possibility of a future move. This is why most long calls expire worthless. The moment you buy, the clock starts draining that $36.00 toward zero unless SPX moves decisively in your favour.

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,400 | −$3,600 (max loss) |

| 7,500 (entry) | −$3,600 (max loss) |

| 7,586 (breakeven) | $0 |

| 7,650 | +$6,400 |

| 7,800 | +$21,400 |

The loss is flat and capped no matter how far SPX falls. The profit is unlimited — but it requires a significant upward move just to break even.

The Buyer vs Seller Reality

This is the section most options courses skip. Here it is plainly.

| Long Call (You, the Buyer) | Short Call (The Seller) | |

|---|---|---|

| Probability of Profit | ~30–40% | ~60–70% |

| Max Profit | Unlimited | Capped (premium collected) |

| Max Loss | Premium paid ($3,600) | Unlimited (naked) |

| Theta | Enemy — costs you every day | Friend — earns every day |

| Who wins more often? | Rarely | Usually |

| Who wins bigger when right? | Buyer, by a lot | — |

A long call has roughly a 30–40% probability of profit at expiration. That means 60–70% of the time, the buyer loses their entire premium. The seller on the other side collects that premium more often than not.

This isn’t a flaw — it’s the design. The buyer accepts a low win rate in exchange for the chance at a large asymmetric payoff. The seller accepts a high win rate in exchange for capped gains and the risk of catastrophic loss on the rare big move.

Neither side is wrong. But you must know which side you’re on and trade the size accordingly.

A long call is a lottery ticket, not an investment. Size it like one. Losing the entire premium is the expected outcome more often than not.

Understanding the Greeks

Delta (0.30–0.50 for ATM): Delta tells you how much the option price moves per $1 move in SPX. An ATM long call has a delta of roughly 0.50 — if SPX moves up $10, the option gains ~$5 in value. Delta moves toward 1.0 as the option goes deeper in the money, and toward 0 as it goes further out of the money.

Theta (negative — your enemy): Every day that passes, your option loses value from time decay. For a 30 DTE option, theta might be $20–$50 per day. You are paying rent on your position every single day. If SPX stays flat for two weeks, you’ve lost a significant portion of your premium with nothing to show for it.

Vega (positive — a friend when IV rises): Long calls benefit from rising implied volatility. If the VIX jumps from 16 to 22 after you buy your call, your option becomes more valuable even if SPX hasn’t moved yet. Conversely, if IV collapses (common after earnings or big events), your option can lose value even if SPX moves in your direction. This is called IV crush and it destroys long option positions regularly.

Gamma (positive — accelerates gains near expiry): Gamma measures how fast delta changes. As expiration approaches, gamma increases dramatically — a small move in SPX produces a larger change in the option’s value. This cuts both ways: a sharp rally can turn a modest gain into a large one quickly, but a reversal can just as quickly erase it. Gamma is highest for ATM options closest to expiration.

Rho (ρ = ∂C/∂r) — positive for calls, benefits from rising rates: Rho measures the sensitivity of the option’s price to changes in interest rates. Formally: ρ = ∂C/∂r, meaning the rate of change of the call price (C) with respect to the risk-free rate (r). A long call has positive rho — rising interest rates increase the theoretical cost of carrying the underlying stock, which slightly increases call values. In practice, rho is the least impactful Greek for short-dated options like 0–30 DTE SPX trades. It becomes meaningfully larger for longer-dated options (LEAPS), where the time value of money compounds over the holding period and a 1% rate move can shift the option’s value by several dollars.

Trade Management & Adjustments

Taking profits: Most experienced traders don’t hold long calls to expiration. A common approach is to close at 50–100% gain — take the double and move on. Holding for the “moonshot” usually means giving back profits as theta accelerates near expiry.

Cutting losses: Set a mental stop at 50% of premium paid. If you paid $3,600 and the position drops to $1,800, close it. You preserve half your capital for the next trade. Letting a long call ride to zero hoping for a late recovery is one of the most common and expensive habits in options trading.

Rolling: If you are wrong on timing but still believe in the direction, you can close the current call and open a new one with a later expiration. This costs money (you’re buying more time) and should only be done if your thesis is genuinely intact — not as an emotional response to being down.

What to avoid:

- Buying 0 DTE OTM calls on SPX as a regular income strategy. These expire worthless the vast majority of the time.

- Doubling down when a long call is losing value. Adding to a losing premium position accelerates losses.

- Ignoring IV. Buying calls when VIX is elevated means you’re paying an inflated premium and face a headwind from IV mean-reversion.

Real-World Example

The trade: SPX has been consolidating near all-time highs. The Federal Reserve is meeting in 3 weeks and the trader expects a dovish signal to push equities higher.

- Buy: 1 SPX 7,550 Call (30 DTE)

- Premium paid: $27.00 → $2,700 total

- Breakeven: 7,577

What happened:

The Fed meeting came and went with no surprise. SPX moved from 7,480 to 7,540 over 28 days — a 60-point rally. Impressive by most measures.

But the 7,550 strike was never reached. The call expired worthless.

In the final 48 hours, the option’s value plummeted from $4.00 to $0.00 as the market priced in that SPX had almost no chance of clearing 7,550 before the closing bell. Theta, which had been quietly draining $3–$5 per day for weeks, accelerated to $2–$3 per hour in the final sessions. There was no gradual decline — the last few dollars disappeared almost instantly.

Result: -$2,700 (100% loss)

SPX rallied nearly 0.8% and the long call buyer still lost everything. This is the brutal reality of buying OTM options — being directionally right is not enough. You need to be right about how far and how fast.

A seller on the other side of this trade collected $2,700 in premium and kept every cent.

When to Use This Strategy

Best conditions:

- Strong directional conviction with a specific catalyst (earnings, Fed, economic data)

- Low implied volatility environment — cheaper premiums mean a better entry price

- Enough time for the thesis to play out (30+ DTE for most setups)

Avoid when:

- IV is elevated — you’re paying a high premium that may deflate regardless of direction

- You don’t have a specific catalyst or time horizon

- You’re thinking of it as a “safe” trade because your “max loss is just the premium” — that premium is still real money

Ideal VIX level: Below 18. Above 25, long calls become expensive and IV crush risk increases significantly.

Strategy Ladder — Next Steps

Came from: Just starting with options? Read the foundational Introduction to Options Trading first.

The bearish equivalent: For a mirror-image bet on the downside, see Long Put .

Natural progression from here:

- Want to reduce the cost of your long call? → Bull Call Spread — buy a call, sell a higher-strike call to offset cost

- Want to be on the other side of this trade? → Short Call (coming soon) — sell the call, collect premium, accept unlimited risk

- Want to profit from a big move in either direction? → Long Straddle — buy both a call and a put

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.