30-Second Summary

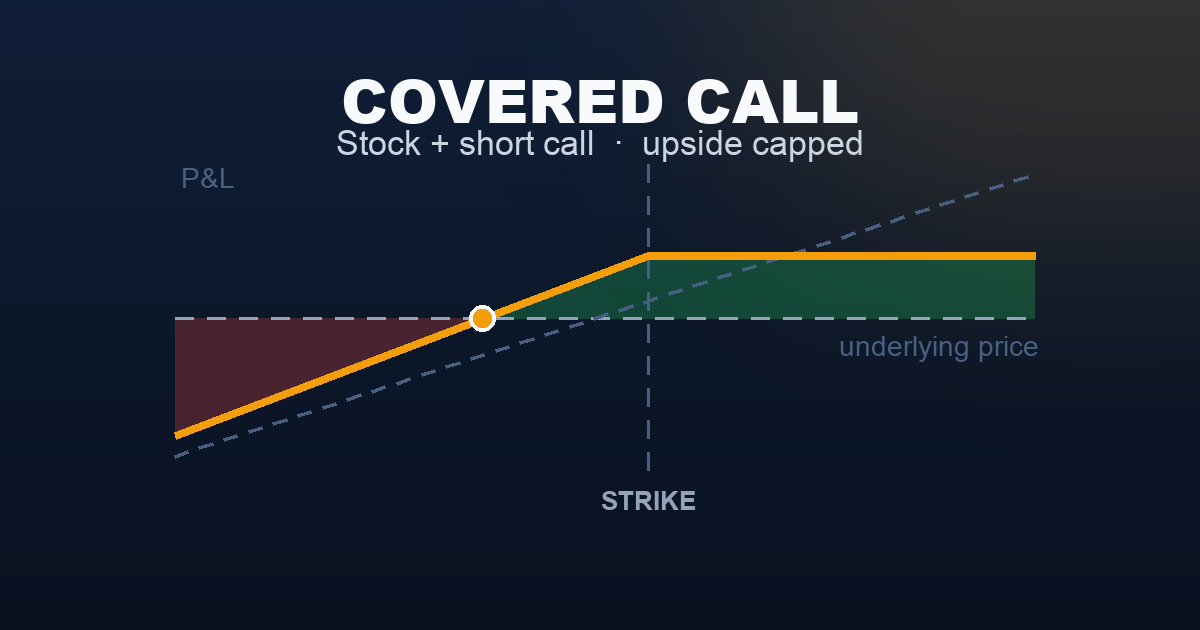

A covered call is the most popular income strategy in options. You own stock and sell a call option against your position — collecting premium upfront. If the stock stays below the strike at expiration, you keep the premium as extra income on your shares. If it rises above the strike, your shares are called away at a profit. Either way, the premium lowers your effective cost basis.

This is a seller’s strategy. Theta works in your favour — every day that passes without the stock reaching your strike is profit. The trade-off: you cap your upside. If the stock rallies hard past your strike, you participate only up to the strike and miss the rest. That’s the price of the income.

What Is a Covered Call?

When you sell a call option against shares you already own, you’re creating a covered call. You collect a premium upfront in exchange for agreeing to sell your shares at the strike price if the stock rises above it by expiration.

The word covered means the short call is backed by real shares — if the call is exercised, you deliver the shares you own rather than face unlimited loss. This is what distinguishes a covered call from a naked call, which has theoretically unlimited risk and requires a margin account.

Think of it like renting out a property you own. You collect rent each month. If a buyer decides they want to permanently purchase the property at a pre-agreed price, you must sell — and you walk away with the agreed price plus all the rent you collected. The risk: if the property doubles in value, you’ve already agreed to sell it at the original price.

The key phrase: you are selling time. Every day that passes without the stock reaching your strike, the option you sold decays in value — and that decay is profit in your pocket.

Setup & Execution

Legs:

- Leg 1: Own (or buy) 100 shares of the underlying

- Leg 2: Sell 1 call option at or above the current price

Strike selection:

- In-the-money (ITM): Strike below current price. Higher premium collected and more downside buffer, but the stock will almost certainly be called away on any rally. Suited for very neutral or slightly bearish views.

- At-the-money (ATM): Strike near current price. Collects the most time value. High probability of being called away if the stock moves at all.

- Out-of-the-money (OTM): Strike above current price. Lower premium, but gives the stock room to appreciate before being called. The most common choice for bullish-leaning covered call writers who want to keep their shares.

Expiration selection:

- 21–30 DTE: The sweet spot. Theta decay is fastest in this window relative to time remaining. Most systematic covered call writers sell monthly at 30 DTE and roll.

- 45+ DTE: More premium but longer commitment. Less flexibility to respond if the stock moves sharply.

- 7–14 DTE: Faster decay but lower absolute premium. Works well when rolling weekly.

SPY Example — Entry:

Trade:

- Own: 100 shares SPY @ $750 = $75,000 capital deployed

- Sell: 1 SPY $760 Call (30 DTE) for $7.00 = $700 premium received

- Net cost basis: $750 − $7.00 = $743 per share

- Breakeven at expiry: $743

To generate $700 in income, SPY only needs to stay below $760 at expiration — it can rise, fall slightly, or stay flat. The call only becomes a problem above $760.

Understanding what you’re collecting:

The $7.00 premium is made up of two components:

| Component | What it means | Amount (approx.) |

|---|---|---|

| Intrinsic Value | How far the option is already in the money | $0 (OTM strike — none) |

| Extrinsic Value | Time value + implied volatility premium | $7.00 (all of it) |

Since the $760 strike is above the current SPY price of $750, the call has zero intrinsic value — you are being paid entirely for the possibility of a future rally. If SPY never reaches $760, the option expires worthless and you keep the full $7.00 per share. If it does, you sell your shares at $760 — a $10.00 gain on the stock plus the $7.00 premium = $1,700 total, the maximum this trade can return.

The Payoff Diagram

| SPY at Expiry | P&L |

|---|---|

| $710 | −$3,300 |

| $743 (breakeven) | $0 |

| $750 (entry) | +$700 |

| $760 (strike) | +$1,700 (max profit) |

| $775 | +$1,700 (capped) |

Above the strike, the payoff is flat. A $775 SPY and a $765 SPY pay you the same $1,700. You gave up all gains above $760 when you sold the call.

Below $743, the premium stops offsetting the stock decline and losses begin to accumulate. The covered call does not protect you from a significant drop — it only provides the $7.00 buffer.

The Seller’s Advantage

This is the first strategy on this site where you are the seller. The probability math shifts in your favour.

| Covered Call (You, the Seller) | Long Call (The Buyer) | |

|---|---|---|

| Probability of Profit | ~60–70% | ~30–40% |

| Max Profit | Capped at $1,700 | Unlimited |

| Max Loss | Stock to zero (−$74,300) | Premium paid only |

| Theta | Friend — earns every day | Enemy — costs every day |

| Who wins more often? | Usually | Rarely |

| Who wins bigger when right? | — | Buyer, by a lot |

The covered call has roughly a 60–70% probability of expiring below the strike — meaning you keep the full $700 premium about two-thirds of the time. That is a genuine statistical edge, and it repeats every single month if you roll systematically.

But notice the asymmetry. If SPY rallies to $810, the buyer of your call collects enormous profits while you’re capped at $1,700. And the downside risk is not the option premium — it’s owning $75,000 worth of stock. If SPY falls 20%, you lose roughly $15,000 minus the $700 premium. The covered call is not a hedge. It is an income enhancement on a position you are already willing to hold.

Understanding the Greeks

Delta (~+0.55 combined position): The combined covered call position has a net positive delta of roughly 0.55–0.70. You own the stock (delta = +1.0) and the short call has delta of approximately −0.30 to −0.45. The net effect: you still benefit from the stock rising, just less so dollar-for-dollar than a pure stock position. As the stock approaches and exceeds the strike, your net delta falls toward zero — the call’s negative delta offsets more and more of the stock’s positive delta.

Theta (positive — your friend): This is the key advantage over buying strategies. Every day that passes, the call you sold loses value from time decay. That decay is profit you’ve already locked in from selling. For a 30 DTE option, theta might earn you $5–$15 per day in decay. You are collecting rent, not paying it.

Vega (negative — your enemy): Rising implied volatility hurts the covered call. If VIX jumps from 16 to 24, the call you sold becomes more expensive to buy back, reducing your unrealised gain. Selling covered calls when IV is elevated (high VIX) means more premium collected upfront — and a bigger tailwind from IV mean-reversion if volatility subsequently drops.

Gamma (negative — risk near expiry): The short call carries negative gamma. As expiration approaches with the stock near the strike, the call’s delta changes rapidly and unpredictably. A stock that oscillates near $760 in the final few days can make your position difficult to manage — the call swings dramatically in value with each small move. This is when covered call writers most often face the decision to close early or roll.

Rho — minor for short-dated calls: The short call has negative rho, meaning rising interest rates slightly increase the call’s value, which works marginally against you as the seller. In practice, rho is negligible for 30 DTE covered calls. It becomes slightly more relevant for longer-dated positions (LEAPS), but it is rarely a primary concern in a systematic monthly covered call program.

Trade Management & Adjustments

Taking profits early: You don’t have to hold until expiration. If the call you sold for $7.00 decays to $2.10 in two weeks, you’ve captured 70% of the maximum profit with time still remaining. Many covered call writers close at 50% of max profit and redeploy into a new position — capturing more premium cycles per year.

Rolling: If the stock rallies toward your strike, you can roll the call up and out — buy back the existing call and sell a new one at a higher strike and/or later expiration. This maintains the covered call structure and collects additional premium, though it extends your commitment. Rolling up accepts less upside cap in exchange for more room to run.

Assignment: If the call expires in the money, your shares will be called away at the strike. For a covered call, this is not a disaster — you sell your shares at the strike price you agreed to, keep all the premium, and realise the full $1,700 max profit. The only regret is if the stock ran significantly higher. After assignment, you can buy shares again and start the next cycle.

Early assignment risk: SPY options are American-style — the buyer can exercise early. This is rare but can happen if the call goes deep in the money, especially around ex-dividend dates (the buyer may exercise early to capture the dividend). If you’re writing covered calls on SPY near a dividend date, be aware of this risk.

What to avoid:

- Selling covered calls on stocks you don’t want to keep long-term. If the stock falls 30%, the $700 premium is cold comfort.

- Chasing premium by selling ATM or ITM calls aggressively. More premium means more assignment risk and more upside given up.

- Forgetting to roll. A covered call that expires worthless is a success — but leaving your shares unhedged until the next cycle means you’re collecting nothing during that time.

Real-World Example

The trade: A trader owns 100 shares of SPY purchased at $745. Markets have been calm, VIX is low, and they decide to generate some income while waiting.

- Own: 100 shares SPY @ $745

- Sell: 1 SPY $760 Call (30 DTE)

- Premium collected: $8.00 → $800 total

- Max profit: ($760 − $745 + $8.00) × 100 = $2,300

What happened:

A surprise dovish Fed comment triggered a broad equity rally. Over the next 30 days, SPY marched from $745 to $787 — a 5.6% move higher. The trade was correctly directional. The stock went up.

But the $760 call was deep in the money at expiration. The shares were called away at $760.

Result: +$2,300

The covered call worked exactly as designed. But the alternative — holding the shares without selling the call — would have returned ($787 − $745) × 100 = $4,200.

The covered call cost the trader $1,900 in missed gains.

This is the fundamental tension of the covered call: it is profitable, it worked, and yet the trader made less than half of what buy-and-hold would have returned. On a month when the market rallies 5%+, writing a covered call feels like a mistake.

Over time, in flat or slowly rising markets, the income accumulates. In sharp rallies, the cap bites hard. The covered call writer must be genuinely comfortable selling shares at the strike — not just hoping the stock stays below it.

When to Use This Strategy

Best conditions:

- You already own stock and want to generate income on a flat or slowly bullish position

- Implied volatility is elevated — more premium available, and you benefit from IV mean-reversion

- You’re willing to sell your shares at the strike price if called away

- The stock has a clear resistance level above the current price — a natural strike target

Avoid when:

- You believe the stock is about to make a large move higher — selling a call caps your upside at exactly the wrong moment

- IV is very low — the premium collected may not be worth the commitment

- You’re using the covered call as a substitute for a stop loss or portfolio hedge — it is neither

Ideal VIX level: Above 16. The higher the VIX, the more premium you collect for the same strike. Below 14, covered call premiums are thin and may not justify the mechanical overhead of managing the position.

Strategy Ladder — Next Steps

Came from: New to options? Read Introduction to Options Trading first. Already familiar with single-leg buyer strategies? See Long Call and Long Put for the buyer’s perspective on the same trade.

Natural progression from here:

- Want downside protection instead of income? → Protective Put — buy a put on stock you own, the mirror-image of the covered call

- Want to generate income without owning stock first? → Cash-Secured Put — sell a put backed by cash, often used to acquire stock at a discount

- Want to run the covered call and cash-secured put as one continuous cycle? → The Wheel — the covered call is Phases 3–4 of the loop: sell calls on your shares until they’re called away, then return to selling puts

- Ready for two-leg income spreads? → Level 2 — Intermediate Strategies — Bull Call Spread , bear put spreads, and more

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.