30-Second Summary

A cash-secured put is a seller strategy with two built-in outcomes — and you can profit from either one. Sell a put below the current stock price and collect the premium upfront. If the stock stays above the strike at expiration, the put expires worthless and you keep the premium as pure income. If the stock falls below the strike, you’re assigned — you buy 100 shares at the strike price, but your true cost is the strike minus the premium collected, lower than the stock was trading when you entered.

This is a seller’s strategy. Theta works in your favour every day. The trade-off: your downside is owning stock that continues to fall after assignment. The cash-secured put gives you a better entry price on stock you wanted to buy — not a guarantee that the stock will recover.

What Is a Cash-Secured Put?

When you sell a put option, you take on the obligation to buy 100 shares of the underlying at the strike price if the buyer exercises. A cash-secured put means you hold exactly that much cash in your brokerage account — strike × 100 — ready to fund the purchase immediately. No margin. No borrowed capital.

Think of it like placing a standing limit order to buy a stock at a lower price, and getting paid while you wait. If SPY never falls to your strike, you keep the premium and start the next cycle. If it does, you buy the shares at the agreed price — already below where the stock was trading when you entered, with the premium collected reducing your cost further still.

The word secured is important. A naked put — the same trade done in a margin account without full cash collateral — carries identical mechanics but dramatically higher risk on borrowed leverage. Most beginner-level brokerage accounts require cash-securing for exactly this reason. A cash-secured put is one of the most conservative options strategies available.

The key phrase: you choose the price you’re willing to pay, and get compensated for committing to it.

Setup & Execution

Legs:

- Leg 1: Hold enough cash to buy 100 shares (strike × 100)

- Leg 2: Sell 1 put option below the current stock price

Strike selection:

- In-the-money (ITM): Strike above current price. Higher premium but near-certain assignment. Suited for traders who actively want the shares immediately at a set price.

- At-the-money (ATM): Strike near current price. Maximum time value, ~50% probability of assignment.

- Out-of-the-money (OTM): Strike below current price. Lower premium but gives the stock room to move before assignment. The most common choice for income-focused CSP sellers.

Expiration selection:

- 21–30 DTE: The sweet spot. Theta decay is accelerating in this window relative to premium remaining. Most systematic CSP sellers target 30 DTE and close at 50% of max profit.

- 45+ DTE: More premium collected but capital tied up longer.

- 7–14 DTE: Faster theta but lower absolute premium. Works for high-frequency rolling on liquid underlyings.

SPY Example — Entry:

Trade:

- Cash held: $745 × 100 = $74,500 (fully collateralising the short put)

- Sell: 1 SPY $745 Put (30 DTE) for $7.00 = $700 premium received

- Breakeven at expiry: $745 − $7.00 = $738

- Effective purchase price if assigned: $738 per share

To keep the full $700 premium, SPY only needs to close above $745 at expiration — it can rise, stay flat, or drift a few dollars lower. The put only becomes a problem below $745.

Understanding your capital commitment:

| Cash collateral required | $74,500 |

| Premium collected | $700 |

| Return on capital (30 DTE) | 0.94% |

| Annualised equivalent | ~11.3% |

| Breakeven price at expiry | $738 |

| Effective purchase price (if assigned) | $738 per share |

The $7.00 premium consists entirely of extrinsic value — the $745 strike is $5 below the current price, so the put has zero intrinsic value. You’re being paid for the possibility that SPY declines to $745 within 30 days. If it never does, the full $700 belongs to you.

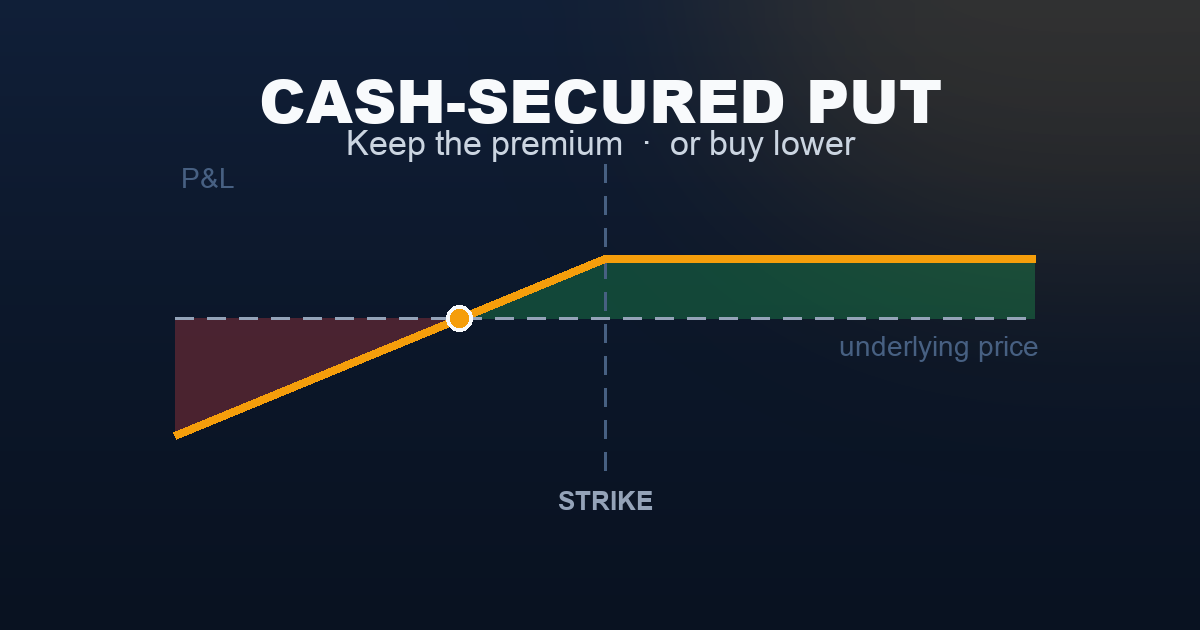

The Payoff Diagram

| SPY at Expiry | P&L |

|---|---|

| $720 | −$1,800 |

| $730 | −$800 |

| $738 (breakeven) | $0 |

| $745 (strike) | +$700 (max profit) |

| $750 (entry) | +$700 (max profit) |

| $775 | +$700 (max profit) |

Above the strike, the payoff is flat. Whether SPY ends at $750 or $775, you earn the same $700. You gave up participation in any rally in exchange for the premium.

Below the strike, the put expires in the money and you are assigned shares. Your P&L then behaves exactly like owning stock — every dollar SPY drops below $738 (your effective cost) costs $100. The $700 premium is the only buffer.

The Seller’s Advantage

This is a seller’s strategy. The probability math shifts in your favour from the moment you enter.

| Cash-Secured Put (You, the Seller) | Long Put (The Buyer) | |

|---|---|---|

| Probability of Profit | ~60–70% | ~30–40% |

| Max Profit | Capped ($700 premium) | Large (strike × 100 − premium) |

| Max Loss | Stock to zero (−$73,800 net) | Premium paid only |

| Theta | Friend — earns every day | Enemy — costs every day |

| Who wins more often? | Usually | Rarely |

| Who wins bigger when right? | — | Buyer, by a lot |

The cash-secured put has roughly a 60–70% probability of expiring above the strike — the same statistical edge as a covered call, which is no coincidence. A CSP and a covered call on the same underlying, same strike, same expiry carry identical risk and reward at expiration — a consequence of put-call parity. The difference is how you get there: the covered call starts with shares and adds a short call; the CSP starts with cash and adds a short put.

The risk is the same as all seller strategies: you accept frequent small wins and rare large losses. A $75 drop in SPY to $663 means a loss of ($663 − $738) × 100 = −$7,500, partially offset by the $700 premium. The premium does not protect you from a serious decline — it only improves your entry price.

Understanding the Greeks

Delta (~+0.25 to +0.40 for OTM put): A short put has positive delta — the position benefits when the stock rises and loses when it falls. An OTM short put with delta of 0.30 means the position gains roughly $30 per $1 rise in SPY and loses roughly $30 per $1 fall. As SPY falls toward the strike, delta rises toward 1.0 — you become increasingly exposed to the stock’s full price risk. As SPY rises above the strike, delta falls toward 0 — the put becomes nearly worthless and your position is essentially holding cash.

Theta (positive — your friend): Every day that passes without SPY falling to your strike is money earned. For a 30 DTE CSP, theta might earn $5–$10 per day as the option decays. If SPY stays flat for two weeks, you’ve already captured a significant portion of the $700 maximum profit through time alone. Most systematic sellers target 50% of max profit — often achieved in half the time remaining.

Vega (negative — your enemy): Rising implied volatility hurts the CSP. If VIX spikes from 16 to 26 after entry, the put you sold becomes much more expensive to buy back — creating an unrealised loss even if SPY hasn’t moved. CSPs entered when VIX is elevated collect more premium but carry more IV risk if volatility rises further. Conversely, a drop in VIX after entry (IV crush) is a pure tailwind: the option loses value faster than time alone would explain.

Gamma (negative — risk near expiry): The short put carries negative gamma. As expiration approaches with SPY near the $745 strike, the put’s delta changes rapidly and unpredictably. A stock oscillating near the strike in the final days creates real assignment uncertainty — the put can swing between nearly worthless and full assignment risk on small moves. This is why many CSP sellers close positions at 50% profit rather than fighting gamma near expiry.

Rho (positive for short puts): A short put benefits slightly from rising interest rates. Higher rates reduce the theoretical value of put options (buyers are less willing to pay for the right to sell at a fixed price), which benefits you as the seller. Rho’s effect is small for 30 DTE options and rarely drives a CSP decision — but it becomes more relevant for longer-dated positions.

Trade Management & Adjustments

Taking profits early: The most reliable rule: close at 50% of max profit. If the put you sold for $7.00 decays to $3.50 in two weeks, you’ve captured 50% of the maximum in half the time. Buy back the put, release the $74,500 in capital, and redeploy into a fresh CSP. Two 50% cycles per month often outperform holding a single position to expiration.

Rolling: If SPY falls toward your $745 strike, you can roll down and out — buy back the $745 put and sell a new one at a lower strike and/or later expiration. This collects additional premium and gives SPY more room to recover, but it extends your capital commitment and increases your total exposure if SPY continues lower. Roll only if your thesis on SPY remains intact and you’re genuinely comfortable buying at the new, lower strike.

Assignment — and why it isn’t a failure: If the put expires in the money, you’re assigned 100 shares at $745. Your effective cost is $745 − $7.00 = $738 per share — lower than the $750 SPY was trading when you put on the trade. You now own 100 shares at a better price than if you’d bought outright. From here you can hold and wait for recovery, sell if SPY recovers, or immediately write a covered call against the shares to generate additional income while holding. This last move — CSP until assigned, then covered call — is called the Wheel. It starts here.

Early assignment risk: SPY options are American-style — the buyer can exercise early. This is rare for puts but can happen if the put goes deep in the money, particularly around ex-dividend dates when there may be a theoretical advantage to early exercise. Be aware of upcoming dividend dates if you’re managing a CSP near or through the strike.

What to avoid:

- Running CSPs on underlyings you don’t actually want to own. Assignment is always possible, and the premium provides no protection against a sharp sustained decline.

- Treating the cash collateral as available for other trades. The full strike × 100 must remain reserved until the position is closed or expires.

- Selecting strikes purely for maximum premium without regard for where you’re comfortable owning the stock. More premium always means more risk.

Real-World Example

The trade: A trader wants to add SPY to their portfolio and was planning to buy outright at $749. Instead, they sell a cash-secured put to try to acquire it cheaper — or earn income if the stock doesn’t reach their strike.

- Cash held: $74,000 ($740 × 100)

- Sell: 1 SPY $740 Put (30 DTE) for $6.00 → $600 received

- Breakeven: $734

- Effective purchase price if assigned: $734

What happened:

Over the 30-day period, SPY drifted lower on light volume — no sharp catalyst, just a slow grind. At expiration, SPY was at $733, below the $740 strike. The trader was assigned 100 shares at $740.

| CSP Strategy | Outright Purchase at $749 | |

|---|---|---|

| Shares acquired at | $740 | $749 |

| Premium collected | $600 | — |

| Effective cost per share | $734 | $749 |

| SPY at expiration | $733 | $733 |

| P&L | −$100 | −$1,600 |

The trader is down — SPY fell through the breakeven. But the CSP produced a −$100 loss versus a −$1,600 loss from outright purchase. The premium collected and the lower strike combined to absorb $1,500 in additional downside.

The position now converts naturally to a covered call. The trader owns 100 shares of SPY at a $734 effective cost and can write a call to generate income while holding for recovery. The Wheel has started.

When to Use This Strategy

Best conditions:

- You have a specific stock or ETF you genuinely want to own at a lower price

- Implied volatility is elevated — more premium available, and you benefit from any subsequent IV crush

- The underlying is in a neutral to mildly bullish trend with no imminent binary risk event (earnings, Fed meeting, economic data)

- You have the capital available to fully collateralise the position without needing it elsewhere

Avoid when:

- The underlying is in a confirmed downtrend — assignment means catching a falling knife

- You don’t actually want to own the underlying — assignment is always possible

- VIX is very low — thin premiums may not justify locking up $74,000+ for a month

- A major catalyst (earnings, FDA) is expected within the 30-day window

Ideal VIX level: Above 16. Higher VIX means more premium for the same strike distance. The CSP seller also benefits doubly from any subsequent drop in VIX — the option loses value faster than time alone would explain.

Strategy Ladder — Next Steps

Came from: New to options? Read Introduction to Options Trading for the foundational framework. Coming from buyer strategies? The Long Put is the buyer’s side of this same trade.

The complementary strategy: Got assigned and now own shares? → Covered Call — sell a call against your position to generate income while holding. Together with the CSP, this forms the Wheel.

The margin-backed version: → Short Put (Naked) — the same trade on margin instead of full cash. Higher return on capital, meaningful leverage risk if assigned.

Natural progression from here:

- Want to protect shares you hold after assignment? → Protective Put — buy a put to hedge existing shares

- Want to cap the maximum loss on the short put itself? → Bull Put Spread — sell a put and buy a lower-strike put to define the risk

- Want to run the CSP and covered call as a systematic cycle? → The Wheel — chain the two into a repeating income loop: sell puts until assigned, sell calls until called away, repeat

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.