30-Second Summary

A short strangle sells an out-of-the-money call above the current price and an out-of-the-money put below it — different strikes, same expiration, both short. You collect a net credit upfront. If the underlying stays between the two OTM strikes at expiration, both options expire worthless and you keep the full credit. If the underlying moves far enough to breach either breakeven, one of the short obligations starts losing money — with no wing to stop it.

The short strangle is the most widely traded naked-selling structure among professional income traders. Wider breakevens than the Short Straddle mean a higher probability of profit and more room for the market to fluctuate without threatening the position. You collect less premium per trade — but you win more often, and the winning range is a flat profit plateau rather than a single pin point.

What Is a Short Strangle?

Selling a strangle means taking on two obligations:

- Short call: If SPX rallies above the call strike, the position starts losing. The short call is worth more to close every point SPX rises above the strike — offset only by the premium collected.

- Short put: If SPX falls below the put strike, the position starts losing. The short put is worth more to close every point SPX falls below the strike — offset only by the premium collected.

You collect both premiums at entry. If SPX stays anywhere between the two strikes at expiration — a 100-point range in this article’s example — neither obligation is costly and you keep the full credit. If SPX breaks through either breakeven, one obligation starts producing losses with no defined ceiling.

The short strangle’s defining structural advantage over the short straddle is the flat profit plateau. Where the straddle earns maximum profit only when SPX pins exactly at the ATM strike, the strangle earns maximum profit for any SPX close between the put strike and the call strike. The market can move 25 points in either direction from the current price and the trade still produces full maximum profit.

You are the counterparty to the long strangle buyer. Every dollar of premium you collect is a dollar the buyer paid hoping for a large move. The seller wins approximately 70–80% of the time on a short strangle — because markets more often stay within a range than break decisively past OTM strikes. But the losses when they occur can be many times the premium collected. Position sizing and mechanical stop execution are what make this sustainable.

Setup & Execution

Legs:

- Leg 1 (Sell): 1 OTM call above the current underlying price

- Leg 2 (Sell): 1 OTM put below the current underlying price

Both legs: same underlying, same expiration, different strikes.

Strike selection: Traders commonly target two ranges depending on premium requirements:

- 15–25 delta strikes: The standard short strangle range. Each leg carries roughly 15–25 delta, giving the structure an 80–85% theoretical probability of both options expiring worthless. Enough premium to justify the trade; enough buffer to survive typical market fluctuations. This is the most widely used configuration.

- 10–15 delta strikes: A wider, lower-credit strangle. Very high probability (85–90%+), but premium is thin. Useful in low-IV environments where tighter strikes don’t collect enough to justify the undefined risk.

For symmetric, non-directional exposure, match the call and put strikes equidistant from the current price. A slight directional lean can be introduced by widening the side you’re less concerned about.

Expiration selection:

- 30–45 DTE: The standard window. Enough theta decay per day to generate meaningful income; enough time to manage if SPX moves toward a short strike.

- 7–21 DTE: Faster theta-per-dollar but less buffer. Short strangles with less than two weeks remaining are vulnerable to rapid movement.

- 45–60 DTE: Used in very-high-IV environments to lock in elevated premiums further in advance.

SPX Example — Entry:

Trade:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Short call | 7,550 | Sell | +$2,150 |

| Short put | 7,450 | Sell | +$2,150 |

| Total | +$4,300 (credit) |

- Net credit: $43.00 per contract = $4,300 total received

- Max profit: $4,300 (any SPX close between 7,450 and 7,550 at expiration)

- Max loss: Unlimited on both sides

- Upper breakeven: 7,550 + 43 = 7,593

- Lower breakeven: 7,450 − 43 = 7,407

Compare to the short straddle: An ATM short straddle at 7,500 would collect approximately $7,200 but with breakevens at 7,428 and 7,572. This strangle collects $2,900 less but the breakevens are 43 points wider on each side — SPX can move an additional 43 points in either direction before the trade begins losing.

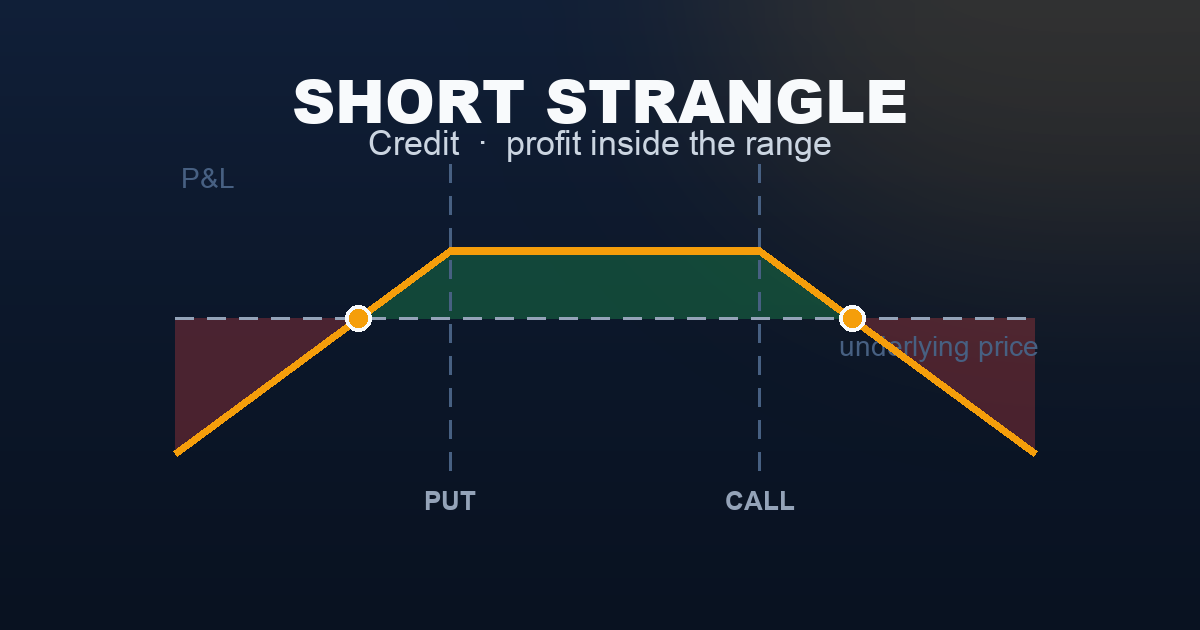

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,350 | −$10,000 |

| 7,407 (lower breakeven) | $0 |

| 7,450 (put strike) | +$4,300 |

| 7,500 (inside profit zone) | +$4,300 |

| 7,550 (call strike) | +$4,300 |

| 7,593 (upper breakeven) | $0 |

| 7,650 | −$10,000 |

The flat-top inverted-U shape is the short strangle’s signature — the exact mirror of the long strangle’s flat-bottom U. The plateau sits at the maximum credit level and spans the full range between the two OTM strikes. Any SPX close within that range earns the full credit. The two loss arms drop steeply below the breakevens with no wing to cap them.

This flat profit zone distinguishes the strangle from the straddle. In a short straddle, maximum profit requires SPX to pin exactly at the ATM strike at expiration. In a short strangle, maximum profit is earned across the entire range between the short strikes — any close between 7,450 and 7,550 produces the same full credit. The market simply needs to stay within the wider range.

The Seller vs Buyer Reality

| Short Strangle (Seller) | Long Strangle (Buyer) | |

|---|---|---|

| Probability of Profit | ~70–80% | ~20–30% |

| Max Profit | Capped: premium collected ($4,300) | Unlimited / very large |

| Max Loss | Unlimited on both sides | Capped: debit paid ($4,300) |

| Profit zone | Flat plateau between the two strikes | Two wings outside the breakevens |

| Theta impact | Ally — earns every day | Enemy — costs every day |

| Vega impact | Enemy — rising IV hurts | Ally — rising IV helps |

The short strangle wins roughly 70–80% of the time — higher than the short straddle (~60–70%) because of the wider profit zone. But the losses when they occur are just as potentially severe. A gap move through either breakeven creates losses that grow without limit until the position is closed.

The math of premium selling requires that occasional large losses not outweigh accumulated small wins. A strangle that collects $4,300 per trade and loses $12,900 on one stop-out requires three complete wins to recover. The only path to a positive long-run expectancy is consistent position sizing and mechanical stop execution — not varying size based on confidence, and not moving stops when a loss is inconvenient.

Understanding the Greeks

Net Delta (near zero at entry): A 20-delta short call and a −20-delta short put produce net delta near zero at entry. The position is non-directional. As SPX moves toward one strike, the tested option’s delta grows while the untested side approaches zero. The position develops a directional lean: testing the call side makes the position delta-negative, testing the put side makes it delta-positive. Managing this delta drift is the central ongoing task of the short strangle seller.

Net Gamma (negative — the primary risk driver): Short gamma means losses accelerate as SPX moves. A moderate move from 7,500 to 7,530 creates a small loss on the call side. A large move to 7,595 creates a disproportionately larger loss — because negative gamma compounds the delta increase as SPX moves. Negative gamma is most dangerous in the final two weeks, when a short strangle near its short strikes can produce $1,000–$3,000 in losses from a single session.

Net Theta (positive — the daily income engine): Two short OTM options decay every day. For a $4,300 short strangle at 30 DTE, net theta earns approximately $70–$115 per calendar day — somewhat less than a short straddle because OTM options carry less time value. Every day SPX stays within the profit zone is income. The theta advantage is why systematic sellers return to this structure month after month: the income is steady and does not require the market to do anything specific except remain range-bound.

Net Vega (negative — the IV expansion threat): Two short options lose value when IV rises. A VIX spike after entry inflates both short options, producing mark-to-market losses before SPX has moved significantly. The strangle’s vega exposure is lower than the straddle’s in absolute terms (OTM options carry less vega than ATM options), but it remains a primary systemic risk. Entering when IV is elevated (VIX 20–28) and likely to mean-revert creates a structural tailwind: the short options deflate as VIX normalises, accelerating profit beyond what theta alone produces.

Net Rho (≈ 0): The call’s positive rho and the put’s negative rho approximately offset at similar delta magnitudes. Negligible for 30–45 DTE structures.

Trade Management

The short strangle requires the same disciplined management as the short straddle. The flat profit zone gives it more built-in resilience — SPX can move 25–30 points in either direction from entry and the trade remains fully profitable. That buffer reduces the frequency of management decisions, but when a threat develops, the response protocols are identical.

Rule 1 — Profit target: 25–50% of credit collected

At 25% of the $4,300 credit ($1,075 gain, strangle worth $3,225 to close), the position has captured meaningful premium with reduced risk. At 50% ($2,150 gain, strangle worth $2,150 to close), the risk-reward of holding further has shifted against the seller. Close and redeploy. Traders who wait for 75–100% of credit typically hold through the most dangerous gamma window and frequently give back gains.

Rule 2 — Stop loss: 200% of credit received

If closing the strangle now costs $12,900 (2× the $4,300 credit as a total loss from mark-to-market), close immediately. A tighter 150% stop is also common. The exact threshold matters less than the commitment to execute it without hesitation.

Rule 3 — Time-based exit: 21 DTE

Close regardless of P&L at 21 days remaining. The gamma environment from 21 DTE inward produces disproportionate risk relative to the remaining premium. The first three weeks of a 30 DTE strangle capture most of the available theta with manageable gamma; the final week carries accelerating tail risk. Exit early, preserve capital for the next cycle.

Rule 4 — Rolling to re-centre

When SPX drifts 30–40 points from the entry price, the strangle develops a meaningful delta bias. Rolling — buying back the current strangle and selling a new one at the updated ATM level — resets delta and collects additional credit. Roll once or twice at most. Rolling into a trending market repeatedly compounds losses rather than managing them.

Rule 5 — Close before scheduled binary events

If an FOMC decision, CPI release, NFP, or major index constituent earnings falls within the remaining days, close the strangle before the event. Short strangles are built for calm markets — they are structurally exposed to the gap moves that catalysts produce.

Position sizing: Risk no more than 2–3% of account equity per short strangle. Undefined-risk structures require tighter per-trade limits than defined-risk spreads.

Real-World Example

The setup: SPX has been trading in a 90-point range for three weeks following a VIX spike that proved transient. VIX at 21.5 is elevated relative to the 60-day average of 17 — option prices are pricing in more movement than the current environment warrants. Daily SPX ranges have narrowed from 55 to 28 points. No major catalyst is scheduled for the next 25 days.

Trade:

- Sell SPX 7,550 Call (30 DTE): $23.00 = $2,300

- Sell SPX 7,450 Put (30 DTE): $23.00 = $2,300

- Total credit: $46.00 = $4,600

- Upper breakeven: 7,596 | Lower breakeven: 7,404

Day 18: SPX at 7,521. VIX has declined from 21.5 to 15.8 as the market recovered composure. The strangle is worth $23.00 to close.

- Cost to close: $2,300

- Original credit: $4,600

- Net profit: +$2,300 (50% of max)

Close at the 50% target. The trade captured theta plus an IV tailwind — VIX falling from 21.5 to 15.8 deflated both short legs beyond what time decay alone would have achieved.

The gap scenario:

On Day 12, an unexpected Fed emergency announcement signals financial stability concerns. SPX drops 85 points in two hours to 7,411 — through the lower breakeven of 7,404 and 39 points below the short put strike of 7,450.

- Short put (7,450): worth approximately $65 (intrinsic + time value)

- Short call (7,550): nearly worthless at $1.50

- Strangle to close: $6,650

- Current loss: −$2,050

The position is approaching the 200% stop ($9,200 cost to close). If SPX continues to 7,350:

- Short put (7,450): worth approximately $102 (100 intrinsic + time value)

- Strangle to close: ~$10,350 — past the 200% stop

- Loss: −$5,750

Mechanical stop execution at the 200% threshold limits the loss to approximately one net credit received. Failing to execute the stop allows negative gamma to compound the loss into a catastrophic outcome.

When to Use This Strategy

Best conditions:

- VIX is elevated relative to recent realised volatility — implied vol is pricing in more movement than the market is producing, and mean-reversion is likely

- SPX is in a consolidation phase: tightening daily ranges, declining ATR, no strong directional momentum

- No major binary catalyst is scheduled within the expiration window

- You have active daily monitoring capacity and can manage intraday if SPX tests a short strike

- IV rank is in the upper half of its 52-week range — selling high IV is structurally superior

Avoid when:

- VIX is below 14 — premium barely justifies the undefined risk; breakevens are too narrow

- A known binary event is approaching — FOMC, CPI, NFP, major earnings gap SPX through short strikes regularly

- SPX is in a confirmed trend — one strike will be continuously threatened; rolling is a losing tactic in a trend

- You cannot monitor positions during market hours

When to prefer the strangle over the straddle:

- You want a wider profit zone and higher probability of profit

- Implied volatility is moderate (VIX 17–22) — the straddle’s higher premium collection is less compelling when IV is not extreme

- You prefer more built-in resilience over maximum premium per trade

Ideal VIX level: 18–28. Premium is substantial, IV mean-reversion is a realistic tailwind, and daily SPX ranges typically don’t reach OTM strikes. Below 15, premium is thin relative to the undefined risk. Above 30, gap moves become frequent enough to threaten OTM strikes regularly.

Strategy Ladder — Next Steps

The buyer’s mirror: → Long Strangle — buy the same OTM call and put, pay the debit, profit from a large move in either direction. Every dollar of credit you collect as the seller is a dollar the buyer paid. The same flat zone that is your profit is the buyer’s loss — until the market moves far enough past a breakeven.

The tighter, higher-credit version: → Short Straddle — sell both options at the ATM strike. Collects significantly more premium but narrows the profit zone to a single ATM pin rather than a 100-point range. Same unlimited-risk structure, higher credit, lower probability of maximum profit.

The defined-risk evolution: → Iron Condor — a short strangle with protective long wings added. Buying an OTM call further above the short call and an OTM put further below the short put caps the unlimited losses at the cost of reduced net credit. The iron condor is the professional standard for income trading precisely because it eliminates the tail risk of the naked short strangle while preserving most of the premium income.

The higher-credit defined-risk version: → Iron Butterfly (coming soon) — move both short strikes to the ATM level and add wings. Collects the maximum premium for a defined-risk structure, but the profit zone narrows significantly.

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.