30-Second Summary

A short straddle sells an at-the-money call and an at-the-money put simultaneously — same strike, same expiration, both short. You collect the combined premium on both options upfront as a net credit. If the underlying stays near the strike at expiration, both options decay and you keep the credit. If the underlying moves significantly in either direction, one of the short options creates losses that grow without a ceiling.

This is the exact mirror image of the Long Straddle — same two strikes, same expiration, opposite side. Where the straddle buyer needs a large move, the short straddle seller needs the market to stay put. Theta works for you on both legs every day. You are short gamma, short vega, and long theta. The short straddle collects the most premium of any two-leg strategy — and carries the most risk.

What Is a Short Straddle?

Selling a straddle means taking on the obligations of two contracts simultaneously:

- Short call: You are obligated to pay if SPX rallies above the strike. If SPX moves from 7,500 to 7,650, the 7,500 call you sold is worth $150 intrinsic — you owe $15,000, offset only by the premium you collected.

- Short put: You are obligated to pay if SPX falls below the strike. If SPX moves from 7,500 to 7,350, the 7,500 put you sold is worth $150 intrinsic — you owe $15,000, offset only by the premium you collected.

You are selling both of these obligations simultaneously. In exchange, you collect the combined premium of both options. If the market stays near the strike and neither obligation becomes costly, you keep the premium. If the market makes a significant move in either direction, one of those obligations starts costing you money — and unlike spreads, there are no protective long options to cap the loss.

The key insight: you are the counterparty to the straddle buyer. The buyer pays a premium hoping for a large move. You collect that premium hoping for calm. One of you will be right, but the payoffs are asymmetric: the seller wins frequently in small amounts; the buyer wins rarely but in large amounts.

The short straddle sits at the top of the risk spectrum for two-leg strategies. It requires active management, strict position sizing, and a clear understanding that every dollar of premium collected represents an obligation that can grow many times larger.

Setup & Execution

Legs:

- Leg 1 (Sell): 1 ATM call at the current price strike

- Leg 2 (Sell): 1 ATM put at the same strike

Both legs: same underlying, same strike, same expiration.

Strike selection: Always place the short straddle at-the-money — the strike nearest to the current underlying price. ATM options carry the highest extrinsic value and therefore collect the most premium. Selling OTM options on both sides is a different, lower-risk structure: the Short Strangle .

As SPX drifts away from the strike after entry, the position develops a directional lean. Managing a short straddle often involves rolling to a new ATM strike to re-centre the delta.

Expiration selection:

- 30–45 DTE: The standard window for swing-style short straddles. Theta per day is substantial, and there is enough time to manage if SPX tests a breakeven before expiry.

- 7–21 DTE: Higher theta-per-dollar but less buffer for large moves. Requires tighter management.

- 0 DTE: Extreme case — the straddle either pins near the ATM or it doesn’t. Used by systematic intraday sellers, not appropriate for learning this structure.

SPX Example — Entry:

Trade:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Short call | 7,500 | Sell | +$3,750 |

| Short put | 7,500 | Sell | +$3,450 |

| Total | +$7,200 |

- Net credit: $72.00 per contract = $7,200 total received

- Max profit: $7,200 (SPX pins exactly at 7,500 at expiry — both options expire worthless)

- Upper breakeven: 7,500 + 72 = 7,572

- Lower breakeven: 7,500 − 72 = 7,428

- Max loss: Unlimited on the upside; very large on the downside (theoretical maximum if SPX → 0)

For any profit at expiration, SPX must close between 7,428 and 7,572 — a 144-point profit zone centred over the short strike.

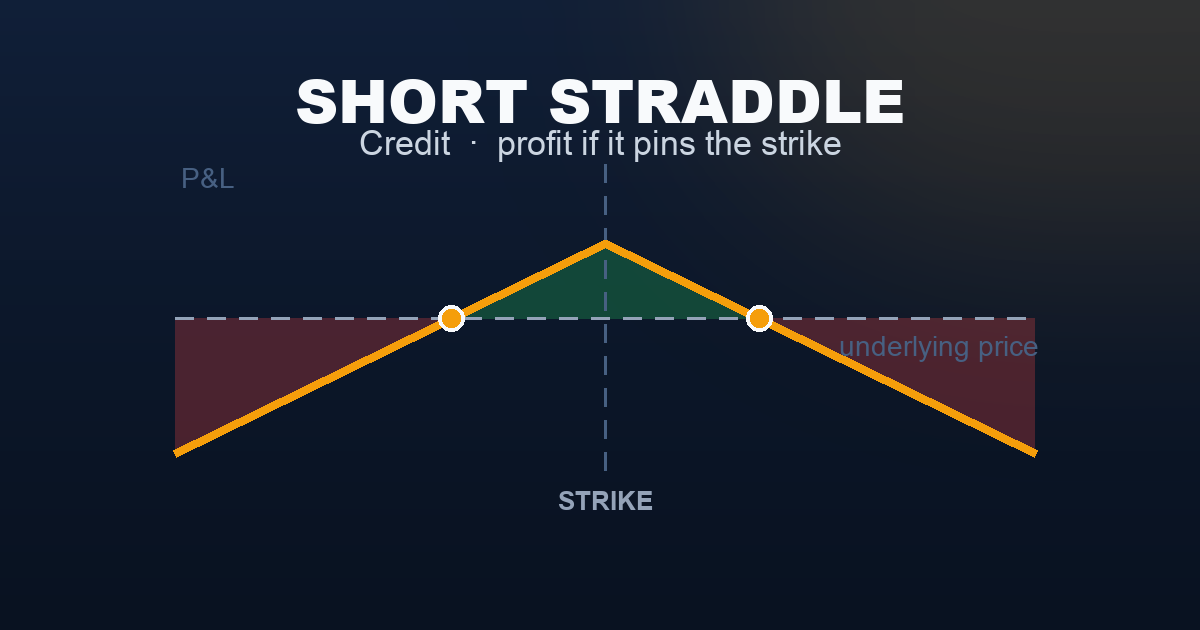

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,350 | −$14,400 |

| 7,400 | −$7,200 |

| 7,450 (lower breakeven) | $0 |

| 7,500 (strike — max profit) | +$7,200 |

| 7,550 (upper breakeven) | $0 |

| 7,600 | −$7,200 |

| 7,650 | −$14,400 |

The inverted V (Λ shape) is the short straddle’s signature — the exact mirror of the long straddle’s V. The peak sits at the ATM strike where both options expire worthless and the full credit is kept. Moving in either direction from the peak reduces profit, and beyond the breakevens the loss grows without limit.

The Seller vs Buyer Reality

| Short Straddle (Seller — this article) | Long Straddle (Buyer) | |

|---|---|---|

| Probability of Profit | ~60–70% | ~30–40% |

| Max Profit | Capped: premium collected ($7,200) | Unlimited / very large |

| Max Loss | Unlimited on both sides | Capped: debit paid ($7,200) |

| Theta | Ally — earns every day | Enemy — costs every day |

| Vega | Enemy — rising IV hurts | Ally — rising IV helps |

| Who wins more often? | Seller — usually | — |

| Who wins bigger when wrong? | — | Buyer — dramatically |

The seller wins roughly 60–70% of the time — but the losses when they occur can be many times the premium collected. One significant gap move can erase months of theta income. This is the fundamental bargain of short premium selling: consistent small wins in exchange for occasional large losses.

The math only works if losses are managed ruthlessly. A seller who lets a losing short straddle run hoping for a recovery is the options market’s most reliable source of catastrophic account drawdowns. The management rules below are structural requirements, not suggestions.

Understanding the Greeks

Net Delta (near zero at entry): The ATM call has a delta of approximately +0.50 and the ATM put approximately −0.50. Together, net delta at entry is close to zero — the position is non-directional initially. As SPX moves away from the strike, the short position develops a delta bias: a rally makes the position delta-negative (short call dominates), and a decline makes it delta-positive (short put dominates). This delta drift is the core management challenge for a short straddle held over time.

Net Gamma (strongly negative — the primary risk driver): Short gamma means the position’s losses accelerate as SPX moves further from the strike. Small moves near the strike create small P&L changes; large moves create disproportionately large losses. Negative gamma is most dangerous near expiration: in the final 7–10 days, a 20-point SPX move on an ATM short straddle can produce a $2,000–$4,000 loss in a single session.

Negative gamma is the mirror of the long straddle buyer’s positive gamma. The short straddle seller profits when the market realises less volatility than implied — when realised vol is below implied vol. The buyer profits when the opposite is true. The straddle is fundamentally a bet on realised volatility versus implied volatility.

Net Theta (strongly positive — the daily income engine): For a $7,200 short straddle at 30 DTE, net theta earns approximately $115–$170 per calendar day. Every day SPX stays near the strike is income. This is the entire appeal of the short straddle: two ATM options decay at the fastest rate of any two-leg combination. The theta accelerates in the final 30 days — which is also when gamma risk becomes most acute. The seller who captured 50% of the premium and exits at 21 DTE has extracted most of the theta without entering the gamma danger zone.

Net Vega (strongly negative — the IV expansion threat): Two short ATM options means two positions that lose value when IV rises. If VIX spikes from 18 to 28 after entry — even if SPX doesn’t move — the straddle’s mark-to-market value surges, producing large unrealised losses. IV expansion is the silent risk: the market can hold completely still and a short straddle can lose 50% or more of the credit collected if VIX doubles.

This is the primary reason to sell straddles when IV is elevated rather than low. Entering at VIX 22 and watching it mean-revert to 16 produces an accelerated theta-plus-vega tailwind. Entering at VIX 14 and watching it spike to 28 produces a simultaneous headwind from both theta and vega.

Net Rho (ρ ≈ 0): The call’s positive rho and the put’s negative rho approximately offset at the same ATM strike. Rho is negligible for 30–45 DTE structures.

Trade Management & Adjustments

The short straddle is the most management-intensive two-leg structure. Unlike an iron condor, there are no protective wings — every management decision matters.

Rule 1 — Profit target: 25–50% of credit collected

At 25% of the $7,200 credit collected (straddle worth $5,400 to close), the position has captured meaningful premium. At 50% ($3,600 remaining value), the risk-reward of holding further has shifted decisively against the seller. Closing at 50% and redeploying is the systematic standard.

Rule 2 — Stop loss: 200% of credit received

If the straddle’s current value reaches 200% of the original credit ($14,400 for a $7,200 credit), close immediately. This limits the net loss to approximately 100% of the credit collected. Many experienced sellers use a tighter 150% stop. The exact level matters less than the discipline to actually execute it.

Rule 3 — Time-based exit: 21 DTE

Close regardless of P&L at 21 days remaining. The gamma environment from 21 DTE inward produces disproportionate risk relative to the remaining theta income. The premium still available at 21 DTE is almost never worth the tail risk of holding through the gamma-concentrated final three weeks.

Rule 4 — Rolling to re-centre

When SPX drifts 25–35 points from the strike, the position develops a significant delta bias. Rather than closing entirely, traders often roll: buy back the straddle and re-sell a new one at the current ATM strike. Rolling collects additional premium and resets delta. The risk: rolling into a larger credit when the market is trending can compound losses if the move continues. Roll once or twice at most — never chase a trending market with successive rolls.

Rule 5 — Close before scheduled binary events

If a major catalyst (FOMC, CPI, non-farm payrolls, major earnings) falls within the remaining days, close or roll the straddle before the event. Short straddles are designed to win in calm markets — they are structurally exposed to the gap moves that catalysts produce. Holding through an event on a short straddle is one of the most reliable ways to incur maximum loss.

Position sizing: Risk no more than 2–3% of account equity per short straddle. This is stricter than the iron condor rule (2–5%) because undefined-loss structures require tighter per-trade limits.

Real-World Example

The setup: VIX has been running at 21–22 for two weeks following a geopolitical shock that proved less severe than feared. SPX has stabilised, average daily ranges have narrowed from 55 to 28 points, and no major catalyst is scheduled for the next 22 days. Implied volatility is above realised — the market is pricing in more movement than it’s producing.

Trade:

- Sell SPX 7,500 Call (30 DTE): $45.00 = $4,500

- Sell SPX 7,500 Put (30 DTE): $39.00 = $3,900

- Total credit: $84.00 = $8,400

- Upper breakeven: 7,584 | Lower breakeven: 7,416

Day 16: SPX at 7,514. VIX has fallen from 21.8 to 14.6 — significant IV mean-reversion. The straddle is worth $38.00 to close.

- Cost to close: $3,800

- Original credit: $8,400

- Net profit: +$4,600 (55% of max)

Close at the 50%+ target. The trade captured theta plus an IV collapse tailwind — both working simultaneously, which is exactly what elevated-IV entry is designed to produce.

The gap scenario:

On Day 11, a surprise CPI print shows inflation re-accelerating. SPX drops 95 points in 90 minutes to 7,400 — breaching the lower breakeven of 7,416 and sitting 100 points below the short strike.

- The short put (7,500 strike) is worth approximately $115 (intrinsic + residual time value)

- The short call is nearly worthless at $1.50

- Straddle to close: $11,650

- Original credit: $8,400

- Net loss: −$3,250

At $16,800, the straddle would pass the 200% stop threshold. The trade should be closed when it reaches that level — not held hoping for a recovery. Without mechanical stop execution, a short straddle account can see months of gains erased in a single session.

When to Use This Strategy

Best conditions:

- VIX is elevated relative to recent realised volatility — implied volatility is overstating actual market movement, and mean-reversion is likely

- SPX is in a consolidation phase with tightening daily ranges and absent momentum

- No major binary catalyst is scheduled within the expiration window

- You have active monitoring capacity and can manage intraday if the position is tested

Avoid when:

- VIX is below 15 — premium collected barely justifies the unlimited risk; breakevens are narrow and any meaningful move is damaging

- A known catalyst is approaching — FOMC, CPI, major earnings, elections are structurally threatening to this position

- SPX is in a confirmed trend — a trending market will push through breakevens and keep moving; the straddle has no wing to limit the loss

- You cannot monitor daily — this is not a set-and-forget structure

Ideal VIX level: 18–28. In this range, premium is substantial and IV mean-reversion is a realistic tailwind. Below 15, the credit barely justifies the risk. Above 30, moves become chaotic and breakevens can be breached multiple times in a single session.

The short straddle wins more often than not — but each win is modest relative to each potential loss. Position sizing and mechanical stop execution are the only two variables that determine whether this strategy builds an account or destroys one.

Strategy Ladder — Next Steps

The buyer’s mirror: → Long Straddle — buy the same ATM call and put, pay the debit, profit from a large move in either direction. Every dollar of premium you collect as the seller is a dollar the buyer is paying. One of you will be right; the payoffs are asymmetric in opposite directions.

The defined-risk version: → Iron Butterfly — add protective long wings to this structure. Selling the 7,500 straddle plus buying a 7,600 call and 7,400 put creates an iron butterfly. The wings cap the unlimited losses at the cost of reduced premium. Most professional sellers prefer the defined-risk iron butterfly over the naked short straddle precisely because it survives the events that can terminate a naked account.

The wider, lower-risk version: → Short Strangle — sell the call 25–50 points above the market and the put 25–50 points below, instead of both at the same ATM strike. Collects less premium but the breakevens are wider. Far more commonly traded by professionals than the naked short straddle.

What this builds toward: → Iron Condor — the iron condor is a short strangle with protective wings added. It is the natural, defined-risk evolution of this selling framework: the core strategy of this site.

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.