30-Second Summary

A naked short call sells one call option without owning the underlying or any offsetting hedge. You collect the full premium as a net credit. If the underlying stays below the short strike at expiration, the call expires worthless and you keep the entire premium. If the underlying rallies above the breakeven, losses grow without limit — in theory, the loss can be infinite since equities have no price ceiling.

This is the most capital-intensive, highest-risk single-leg options position. It requires significant margin, advanced options approval, and active monitoring. It is placed here at the advanced level specifically because of its unlimited risk profile — not because the mechanics are complex, but because the consequences of mismanagement are severe.

What Is a Short Naked Call?

Selling a naked call means taking on an obligation with no hedge:

- The obligation: If SPX closes above the short strike at expiration, you must pay the difference between SPX and the strike × 100. There is no long call to cap that loss.

- The income: You collect the full option premium upfront. If the option expires worthless, you keep every dollar of it.

- The risk: SPX has no theoretical upper limit. A short call can, in extreme cases, turn a modest premium into a catastrophic loss in a single session.

The strategy wins when: (a) SPX stays below the short strike, or (b) implied volatility collapses, reducing the call’s value even if SPX hasn’t moved.

The strategy loses when: (a) SPX rallies through the strike and the breakeven, or (b) implied volatility spikes, increasing the mark-to-market loss even before SPX moves.

Compare this to the defined-risk alternative: a Bear Call Spread — sell a call and buy a higher-strike call. The bought call caps the loss at the cost of a lower credit. Most professional traders prefer defined-risk structures precisely because an unexpected gap move cannot produce an account-ending event.

Setup & Execution

Position:

- Sell 1 OTM call — the further OTM the strike, the higher the probability of profit but the lower the premium collected.

Strike selection:

- Target a delta in the 10–20 range. A 15-delta call has approximately an 85% probability of expiring worthless.

- Higher delta (closer to ATM) = more premium, lower probability of profit, faster loss acceleration.

- Strike placement should align with a technical resistance level or a price SPX is unlikely to reach in the expiration window.

Expiration selection:

- 14–30 DTE: The standard window. Enough premium to justify the trade, enough time to manage if tested.

- 7–14 DTE: Faster theta decay, less premium, shorter exposure window.

- 0 DTE: Extreme case. The call either expires worthless (most common) or the position faces a severe same-session loss.

Margin requirement: Naked short calls require significant margin. Most brokers calculate margin as: 20% of the notional underlying value minus the out-of-the-money amount, plus the premium received. For a 7,600 call on SPX (spot 7,500), this typically exceeds $115,000–$145,000 per contract. Portfolio margin accounts allow more efficient use of capital. This strategy requires Level 4 (or equivalent) options approval at most brokers.

SPX Example — Entry:

Trade:

| Position | Strike | Action | Premium |

|---|---|---|---|

| Short call | 7,600 | Sell | +$2,150 |

- Net credit: $21.50 per contract = $2,150 total received

- Max profit: $2,150 (SPX closes at or below 7,600 at expiry)

- Breakeven: 7,600 + 21.50 = 7,621.50

- Max loss: Unlimited (every point above 7,621.50 costs an additional $100)

At SPX 7,650 (50 above the strike), the loss would be ($50 intrinsic − $21.50 credit) × 100 = −$2,850. At SPX 7,700 the loss would be $7,850. There is no ceiling.

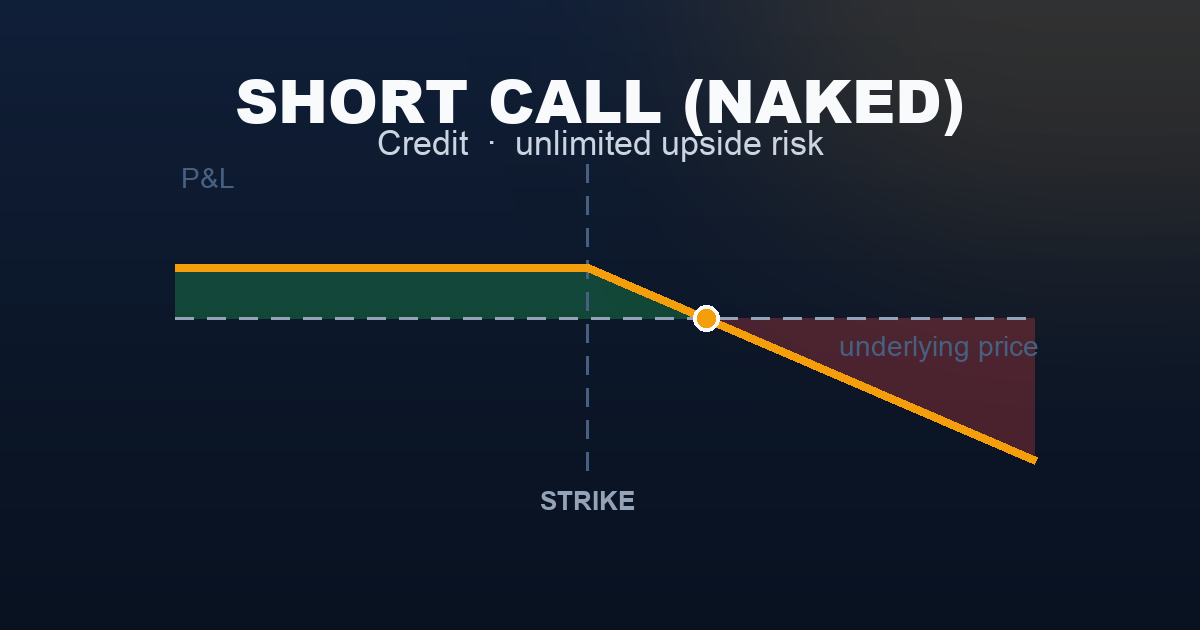

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,350 | +$2,150 (max profit) |

| 7,400 | +$2,150 (max profit) |

| 7,500 | +$2,150 (max profit) |

| 7,600 (short strike) | +$2,150 (max profit) |

| 7,621 (breakeven) | $0 |

| 7,650 | −$2,850 |

| 7,700 | −$7,850 |

| 7,800 | −$17,850 |

The flat green line extending to the left is the signature of this strategy: full credit collected anywhere below the short strike. To the right of the breakeven, every additional SPX point costs $100 more. There is no floor.

The Seller vs Buyer Reality

| Short Call (Seller — this article) | Long Call (Buyer) | |

|---|---|---|

| Net premium | +$2,150 collected | −$2,150 paid |

| Max profit | $2,150 (capped at premium) | Unlimited |

| Max loss | Unlimited | $2,150 (debit paid) |

| Profit requires | SPX stays below 7,621 | SPX rallies above 7,621 |

| Theta | Ally — earns every day | Enemy — costs every day |

| Vega | Enemy — rising IV hurts | Ally — rising IV helps |

| Probability of profit | ~85% (15-delta strike) | ~15% |

| Who wins more often | Seller | — |

| Who wins bigger | — | Buyer (unlimited upside) |

The probability math is compelling: an 85% win rate sounds exceptional. But a single maximum-loss event at SPX 7,700 (−$7,850) requires more than three full wins (+$2,150 each) to recover. The strategy has positive expectancy only with strict position sizing and mechanical stop-loss execution.

Understanding the Greeks

Delta (negative — bearish lean): A 15-delta short call has delta ≈ −0.15. The position loses $15 per point SPX rallies and gains $15 per point SPX declines. As SPX approaches and passes the short strike, delta becomes increasingly negative — the position accumulates losses faster and faster. A 50-delta short call (ATM) loses $50 per SPX point — a far more aggressive position.

Gamma (negative — accelerates losses on rallies): Negative gamma means losses accelerate as SPX rises above the strike. Near expiration, gamma is highest for near-ATM options — a small SPX move in the final days can produce a loss many times larger than the same-size move at entry. This is the primary reason systematic sellers set stop losses far from expiration.

Theta (positive — the income engine): Every day SPX stays below the short strike is earned income. A $2,150 premium collected over 30 days produces roughly $70 of theta per day. Theta accelerates in the final two weeks — the same period when gamma risk becomes most acute.

Vega (negative — the silent risk): A short call loses money when IV rises, even if SPX hasn’t moved. If VIX spikes from 18 to 28 after entry, the 7,600 call becomes much more expensive to close — producing a large unrealised loss before SPX has tested the strike. Entering when VIX is elevated and mean-reverting offers a vega tailwind.

Rho (negative): Rising interest rates increase call values (calls benefit from higher rates). A short call therefore has negative rho — rising rates produce a headwind. Negligible for short-duration positions but worth noting in rate-volatile environments.

Trade Management

Rule 1 — Profit target: 50% of premium

If you collected $2,150 and the call is now worth $1,075 to close, buy it back. The final $1,075 requires holding through the most gamma-concentrated period near expiration. Closing at 50% and redeploying is the systematic standard.

Rule 2 — Hard stop: 200% of premium collected

If the call is worth $6,450 to close ($4,300 above the original credit = 200% of original credit in total loss), close immediately without exception. This limits the maximum realised loss to approximately $4,300. Never negotiate with this rule — the short call’s unlimited risk profile means every point of delay can compound significantly.

Rule 3 — Strike proximity stop: close at or before SPX reaches the short strike

Many traders use a secondary stop: if SPX trades within 5–10 points of the short strike (7,590–7,595 in this example), close or roll regardless of the P&L level. Once SPX is at-the-money, delta, gamma, and vega all accelerate simultaneously.

Rule 4 — Time-based close: 21 DTE

Close the position with 21 days remaining. Gamma risk from 21 DTE inward is disproportionate to the remaining theta income. This is especially critical for a naked position where there is no long strike to slow the loss.

Rule 5 — Rolling: extend duration, not strike

If the call is tested (SPX approaching the strike) but hasn’t hit the stop, roll the call up and out: buy back the current strike and sell a new call at a higher strike in a later expiration. This extends the duration and moves the strike further OTM. Roll only once — rolling a losing naked call into a successively larger position is a systematic account risk.

Position sizing: Due to the unlimited risk profile, size naked calls at no more than 1–2% of account equity. The margin requirement often enforces this naturally, but margin ≠ risk — the actual maximum loss has no ceiling.

Real-World Example

Scenario A — The thesis plays out:

SPX has failed three times to break above 7,580 in the past month. VIX is elevated at 22 — higher than realised volatility — suggesting IV is overpriced. The trader sells the 7,600 call for $2,150, placing the short strike above the recent resistance zone.

Day 22: SPX at 7,488. VIX has declined from 22 to 14 on improving macro sentiment. The 7,600 call is worth $360 to close.

- Cost to close: $360

- Original credit: $2,150

- Net profit: +$1,790 (83% of max in 22 days)

Close. The position benefited from both theta decay (22 days) and IV collapse (8 VIX points) simultaneously. This double tailwind is the ideal outcome for a naked short call entered at elevated IV.

Scenario B — The gap rally:

A surprise CPI print shows disinflation — markets interpret it as a signal for rate cuts. SPX gaps up 80 points at the open from 7,500 to 7,580.

At SPX 7,580 (20 below the short strike):

- The 7,600 call (now 12 DTE) is worth approximately $4,600 (20 points OTM but with elevated IV and 12 days of time value)

- Position showing unrealised loss: $4,600 − $2,150 = −$2,450

SPX continues to 7,625 two sessions later:

- Short call now worth $9,800 (intrinsic $25 + elevated time value)

- Net loss: −$7,650

The 200% stop ($6,450 to close = $4,300 net loss) would have triggered at SPX approximately 7,610. Holding through to 7,625 added another $3,350 in losses in two days. Without the mechanical stop, this trade becomes a margin call event.

When to Use This Strategy

Best conditions:

- SPX is in a confirmed downtrend or strong consolidation, with clearly defined resistance above the intended short strike

- VIX is elevated (20–30) relative to recent realised volatility — IV overpricing works in the seller’s favour

- No major bullish catalyst (positive FOMC surprise, major earnings beats from large index constituents) is scheduled within the window

- A portfolio margin account is available, reducing the capital requirement significantly

Avoid when:

- SPX is in an uptrend or breaking out to new highs — the probability of the short strike being tested rises dramatically

- VIX is below 14 — low premium doesn’t justify the unlimited risk; the risk-reward is structurally poor

- A known bullish catalyst falls in the window (Fed pivot signals, major positive economic data)

- The position is not actively monitored daily — naked short calls cannot be left unattended

Preferred alternative for most traders: The Bear Call Spread provides nearly identical directional exposure with a capped maximum loss. The reduction in premium collected (typically 30–50% less) is a reasonable price to pay for the certainty that a single gap move cannot produce an account-ending event.

Strategy Ladder — Next Steps

The defined-risk version: → Bear Call Spread — buy a higher-strike call to cap the loss. Lower credit, but unlimited risk becomes defined risk. The difference is structural safety, not strategy.

The bullish mirror: → Short Put (Naked) — sell a put without a long put hedge. Same unlimited-risk mechanics, same margin requirements, but directionally bullish (profits if SPX stays above the short strike).

The neutral income structure: → Short Strangle — sell an OTM call and an OTM put simultaneously. Collects premium on both sides, still undefined risk. Higher credit, wider breakevens, but still requires margin and active management.

The defined-risk neutral structure: → Iron Condor — add wings to the short strangle. This is the fully defined-risk evolution of the naked selling framework and the core strategy of this site.

This content is for educational purposes only. Options trading involves significant risk of loss. Naked short options carry theoretically unlimited loss potential and are only appropriate for experienced traders with sufficient capital and active monitoring. Past performance is not indicative of future results.