30-Second Summary

A short calendar spread sells a far-month option and buys a near-month option at the same strike, collecting a net credit. Because the far-month option commands more premium than the near-month option, selling it creates an upfront credit. The trade profits when the underlying makes a large move in either direction by near-month expiration — both options then approach the same value, collapsing the spread in the seller’s favor. It also benefits if implied volatility contracts sharply after entry, since the far-month option (which has more vega) deflates faster than the near-month.

This is the exact mirror of the Long Calendar Spread , which profits when the underlying stays pinned near the strike. Where the long calendar has positive theta and positive vega, the short calendar has negative theta and negative vega. Where the long calendar draws a profit dome over the strike, the short calendar draws a loss trough — and profits on both wings.

Important caveat: The payoff diagram shown below is an approximation at near-month expiration assuming stable implied volatility. In practice, P&L depends heavily on IV at near-month expiry, the term structure of volatility, and the level of the underlying. Short calendar spreads are among the most IV-sensitive structures in options trading — even more so than their long counterparts.

What Is a Short Calendar Spread?

A short calendar spread (also called a reverse calendar or short time spread) uses the same strike across two different expirations — one shorter-dated, one longer-dated — but in the opposite direction from the long calendar:

- Sell: 1 far-month option (60 DTE) at the target strike — the expensive leg you are shorting

- Buy: 1 near-month option (30 DTE) at the same strike — the cheaper leg you own to cap the near-term risk

The far-month option costs more because it carries more time value and more vega. Selling it and buying the cheaper near-month generates a net credit. The profit logic runs in reverse from the long calendar: instead of harvesting the theta differential as the near-month decays faster, the short calendar pays that differential as a cost while waiting for a large move to collapse the spread.

The two ways this trade makes money:

- Large move: If the underlying moves far from the strike by near-month expiration, both options approach the same value (or near zero). The spread collapses, and the seller keeps the credit differential.

- IV contraction: If implied volatility drops sharply after entry, the far-month option — which has more vega — loses value faster than the near-month. The spread narrows in the seller’s favor even without a large price move.

The one way this trade loses: The underlying stays near the strike while IV stays elevated. The near-month decays (hurting the buyer of the near-month leg) while the far-month retains its value. The spread widens, costing more to close than the credit received.

Setup & Execution

Legs:

- Leg 1 (Sell): 1 ATM or near-ATM option at the far-month expiration (60 DTE)

- Leg 2 (Buy): 1 same-strike option at the near-month expiration (30 DTE)

Both legs: same underlying, same strike, same option type.

Option type:

- Call calendar short: Sell the far-month call, buy the near-month call at the same ATM strike. Symmetrical P&L — profits equally from large up or down moves.

- Put calendar short: Sell the far-month put, buy the near-month put. Economically equivalent at ATM but may differ in pricing due to put-call skew.

- Straddle calendar short: Short a call calendar and a short put calendar simultaneously at the same strike. Doubles the credit and doubles the exposure — used by sophisticated traders who want maximum sensitivity to both the move and IV change.

Strike selection:

- Place both strikes at-the-money. ATM options carry the most time value, giving the short calendar the largest credit and the most vega exposure. OTM strikes reduce the credit and shift the breakeven structure.

Expiration selection:

- Near-month: 21–35 DTE. Close enough that a large move will collapse its value quickly; far enough to have meaningful premium.

- Far-month: 45–90 DTE, typically 2× the near-month DTE. Must carry significantly more time value than the near-month to justify the credit structure.

SPX Example — Entry:

VIX at 22 is elevated — the far-month premium is rich, making the short calendar credit larger and more attractive. Traders typically enter short calendars in the upper third of IV’s 52-week range.

Trade:

| Leg | Strike | Expiry | Action | Premium |

|---|---|---|---|---|

| Short call | 7,500 | 60 DTE (far month) | Sell | +$8,600 |

| Long call | 7,500 | 30 DTE (near month) | Buy | −$5,750 |

| Total | +$2,850 |

- Net credit: $28.50 per contract = $2,850 total received

- Max profit (approximate): ~+$2,850 when both options approach worthless (large move)

- Approximate breakevens: 7,450 (lower) and 7,550 (upper)

- Max loss (approximate): ~−$2,850 when SPX pins at 7,500 at near-month expiry with stable IV

Actual P&L at near-month expiration depends heavily on implied volatility at that time. All figures shown assume relatively unchanged IV.

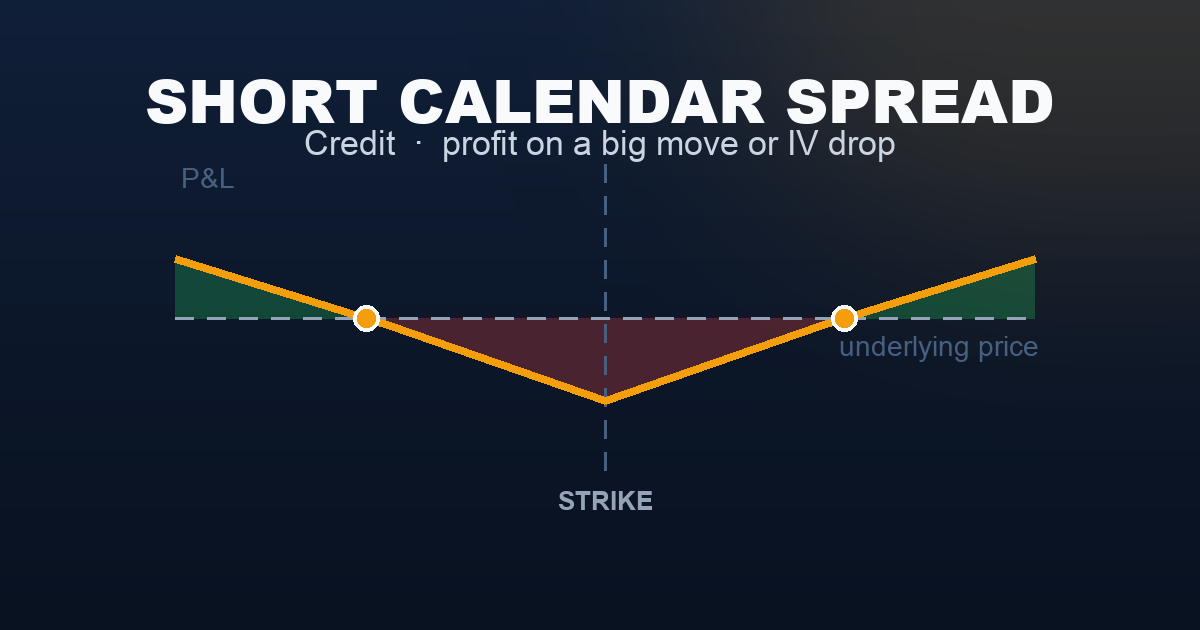

The Payoff Diagram

Approximate P&L at near-month expiration, assuming unchanged implied volatility.

The valley shape is the short calendar’s signature — the inverse of the long calendar’s hill. Max loss sits at the strike; profit rises as the underlying moves away in either direction. Unlike a long strangle or straddle (which have unlimited upside), the short calendar’s profit is capped near the initial credit once the far-month option becomes nearly worthless.

| SPX at Near-Month Expiry | P&L (approximate) |

|---|---|

| 7,350 | ~+$2,150 |

| 7,400 | ~+$1,300 |

| 7,450 (lower approx. BE) | ~$0 |

| 7,500 (ATM — max loss) | ~−$2,850 |

| 7,550 (upper approx. BE) | ~$0 |

| 7,600 | ~+$1,300 |

| 7,650 | ~+$2,150 |

If IV contracts sharply during the trade, the max-loss level improves — the far-month deflates, narrowing the spread. If IV spikes, the max-loss worsens.

Short vs Long: Two Ways to Trade a Calendar

| Short Calendar (This Article) | Long Calendar | |

|---|---|---|

| Structure | Sell far, buy near | Buy far, sell near |

| Net premium | +$2,850 credit received | −$2,850 debit paid |

| Profit requires | SPX moves far from the strike | SPX stays near the strike |

| Theta | Negative — time decay works against you | Positive — earns time decay differential |

| Vega | Negative — benefits from IV contraction | Positive — benefits from IV expansion |

| Gamma | Positive — large moves help | Negative — large moves hurt |

| Ideal condition | High IV, large move expected quickly | Low IV, calm, range-bound expected |

| Payoff shape | Valley (loss at ATM, profit on wings) | Hill (profit at ATM, loss on wings) |

The short calendar is the rarer, more aggressive trade. It collects credit but must fight negative theta every day the underlying stays near the strike. Its edge comes from being selective: entering only in high-IV environments with a strong conviction that a large move is imminent.

Understanding the Greeks

Net Delta (near zero at ATM entry): Both legs are ATM at entry, so directional exposure is nearly zero. As SPX moves away from the strike, both options lose value — but the spread’s value collapses in the seller’s favor, so delta works with the position on large moves. Delta itself is not the primary risk driver.

Net Gamma (positive — large moves help): The near-month option you bought has more gamma than the far-month option you sold, because gamma is proportional to 1/√(DTE). Buying higher gamma and selling lower gamma produces net positive gamma — the position benefits mechanically from large, rapid moves. This is the structural edge that makes profit possible on the wings.

Net Theta (negative — the daily cost): Near-month options decay faster per day than far-month options. Since you bought the faster-decaying leg (near-month) and sold the slower-decaying leg (far-month), net theta is negative. Every day that SPX stays near 7,500, you lose the theta differential — approximately $43–$72 per day in this example. This is the opposite of most credit strategies and is the primary reason short calendars require a catalyst to justify the trade.

Net Vega (negative — IV contraction is your friend): The far-month option carries substantially more vega than the near-month. Selling the high-vega far-month and buying the low-vega near-month produces net negative vega. If VIX drops after entry, the far-month loses value faster than the near-month — the spread narrows, benefiting the short calendar seller. An IV spike after entry is painful: the far-month balloons in value, widening the spread and increasing the cost to close.

Net Rho (near zero): Interest rate effects largely offset between the two legs. Not a meaningful risk driver for short-dated calendars.

Trade Management

Close before near-month expiration — no later than 5–7 DTE: Never allow the near-month to expire while still short the far-month. At near-month expiry, closing leaves you with a naked short far-month option — unlimited risk with no hedge. Close both legs together no later than one week before the near-month expires, regardless of P&L.

Profit target: 50–75% of initial credit ($1,425–$2,140): If a large move occurs early in the trade’s life, close promptly. The position earns most of its profit in the first few days of a decisive move. Holding for the last dollar is rarely worth the continued theta drag. A common approach is to close once 50% of the credit is realised.

Stop loss: 1.5–2× the initial credit ($4,275–$5,700): If the underlying is grinding sideways and the spread is widening, a hard stop prevents a catastrophic loss. Some traders also use a proximity stop: if SPX stays within 20 points of the strike for more than 10 days, exit — the theta drag is working against you and the thesis is failing.

Monitor IV closely — it overrides the price story: A sharp IV spike (VIX moving from 22 to 30) after entry can push the far-month premium significantly higher, overwhelming any gamma benefit from a moderate price move. If VIX rises materially and the underlying hasn’t moved enough to compensate, exit rather than wait for the price move to materialise.

Do not roll into a new short calendar without reassessing: If the near-month is expiring and the trade hasn’t worked, do not reflexively roll to a new cycle. The conditions that made the original entry reasonable (high IV, imminent catalyst) may no longer exist. Reassess IV levels and the next catalyst window before re-entering.

Real-World Example

Scenario A — The CPI shock (trade works)

You enter the short calendar on Monday with SPX at 7,500 and VIX at 22 — elevated, with a hot CPI print expected Thursday. You sell the 60 DTE 7,500 call for $8,600 and buy the 30 DTE 7,500 call for $5,750, collecting $2,850 net credit.

Thursday morning: CPI prints hotter than expected. SPX opens 110 points lower at 7,390. By near-month expiration the following week, SPX remains near 7,390.

- Near-month 7,500 call (bought): Expires worthless. You paid $5,750 — complete loss on this leg.

- Far-month 7,500 call (sold): SPX at 7,390, 110 points OTM, 30 DTE remaining. Worth approximately $1,010. You buy it back at $1,010.

Near-month leg: −$5,750 paid + $0 recovered = −$5,750

Far-month leg: +$8,600 collected − $1,010 to close = +$7,590

Net P&L: +$1,840 (65% of the theoretical maximum credit)

The rapid 110-point move collapsed the far-month’s value while the near-month expired naturally. The thesis worked exactly as designed.

Scenario B — The quiet Fed meeting (trade loses)

Same entry. Fed meeting arrives with no surprises — the statement is mild, rates on hold, markets shrug. SPX barely moves. Over the next four weeks, VIX gradually compresses from 22 to 18 as the volatility event passes without incident.

At near-month expiration, SPX is at 7,505.

- Near-month 7,500 call (bought): Expires with just $5 of intrinsic ($500 value). Paid $5,750, recovered $500 — loss of $5,250.

- Far-month 7,500 call (sold): Nearly ATM with 30 DTE and VIX now 18. Revalued from $8,600 to approximately $6,920 (IV compression helped, but not enough). Buy back at $6,920.

Near-month leg: −$5,750 + $500 = −$5,250

Far-month leg: +$8,600 − $6,920 = +$1,680

Net P&L: −$3,570

The IV compression from 22 to 18 softened the loss — without it, the far-month might have been worth $7,900, producing a −$4,470 loss. But the underlying staying near the strike still delivered a painful result. The loss is close to the diagram’s max-loss level, confirming that a pinned underlying is the short calendar’s worst scenario.

When to Use This Strategy

Best conditions:

- Implied volatility is elevated (upper third of its 52-week range) — the far-month premium is rich, maximising the credit received and the short-vega benefit if IV subsequently contracts

- A major catalyst is approaching that is expected to produce a large, decisive move in either direction: FOMC decision, CPI print, earnings for a highly volatile underlying, geopolitical event

- The underlying has been consolidating tightly for weeks and technicals suggest a breakout is overdue

- You want exposure to a large move without paying the full debit of a long straddle or strangle

Avoid when:

- IV is low — the far-month premium is thin, reducing the credit and the short-vega benefit. This is exactly when the long calendar is attractive.

- The outlook is neutral with no expected catalyst — negative theta will steadily erode the position with no mechanism to recover

- The underlying is in a slow, steady trend without explosive moves — moderate drift without volatility provides no gamma benefit and the theta drag kills the trade

- You cannot actively monitor the position — short calendars need daily attention given the negative theta and IV sensitivity

The short calendar is a niche strategy. Most retail traders find the Long Straddle simpler for large-move bets (no time structure to manage, uncapped profit) and the Iron Condor more reliable for credit income (positive theta, defined risk). The short calendar sits in a narrow window: high IV + imminent catalyst + conviction in a decisive move.

Strategy Ladder — Next Steps

The mirror image: → Long Calendar Spread — buy far, sell near, pay a debit. Profit from time decay when SPX stays near the strike. Positive theta, positive vega, negative gamma. Enter when IV is low and a quiet period is expected.

Uncapped large-move bet (simpler): → Long Straddle — buy both ATM call and put in the same expiration. No time structure to manage. Pays a debit but profits are uncapped on the upside, and the downside is only limited by the underlying reaching zero. Better for traders who want to avoid the complexity of rolling calendar legs.

Long move bet with lower cost: → Long Strangle — buy OTM call and OTM put. Lower debit than a straddle, needs a larger move, no calendar management required.

Credit with defined risk: → Iron Condor — sell both an OTM call spread and OTM put spread. Positive theta, range-bound outlook, no gamma edge. Go-to for income when the view is neutral and IV is moderately elevated.

This content is for educational purposes only. Calendar spread P&L is an approximation; actual results depend heavily on implied volatility levels at near-month expiration. Options trading involves significant risk of loss. Past performance is not indicative of future results. Always consult a licensed financial professional before trading.