30-Second Summary

A long strangle buys an out-of-the-money call above the current price and an out-of-the-money put below it — different strikes, same expiration, both long. You pay a net debit. If the underlying moves far enough in either direction to surpass either breakeven at expiration, you profit. If it stays between the two OTM strikes, both options expire worthless and you lose the full debit.

The strangle is a cheaper, wider alternative to the Long Straddle . Placing each leg out-of-the-money reduces the debit — but widens the breakevens, requiring a larger move to profit. Lower cost, lower probability, same event-driven logic.

What Is a Long Strangle?

A long strangle says: I don’t know which direction the market moves, but I’m confident it will move significantly — enough to push past one of my two OTM options into profitable territory.

Like the long straddle, the strangle is a pure volatility bet. Direction is irrelevant. You own a call that profits if SPX rallies far enough above the call strike, and a put that profits if SPX falls far enough below the put strike. If SPX stays between the two strikes at expiration — anywhere in the dead zone — both options expire worthless and the full debit is lost.

The essential trade-off versus the straddle:

- Long Straddle: Both legs ATM. Higher debit. Breakevens closer to the current price. Profitable with a moderate move.

- Long Strangle: One leg OTM above, one OTM below. Lower debit. Breakevens further out. Requires a larger move to profit.

Think of the strangle as buying two out-of-the-money policies instead of one at-the-money policy. The premiums are lower — but the triggering event must be more extreme for either policy to pay out.

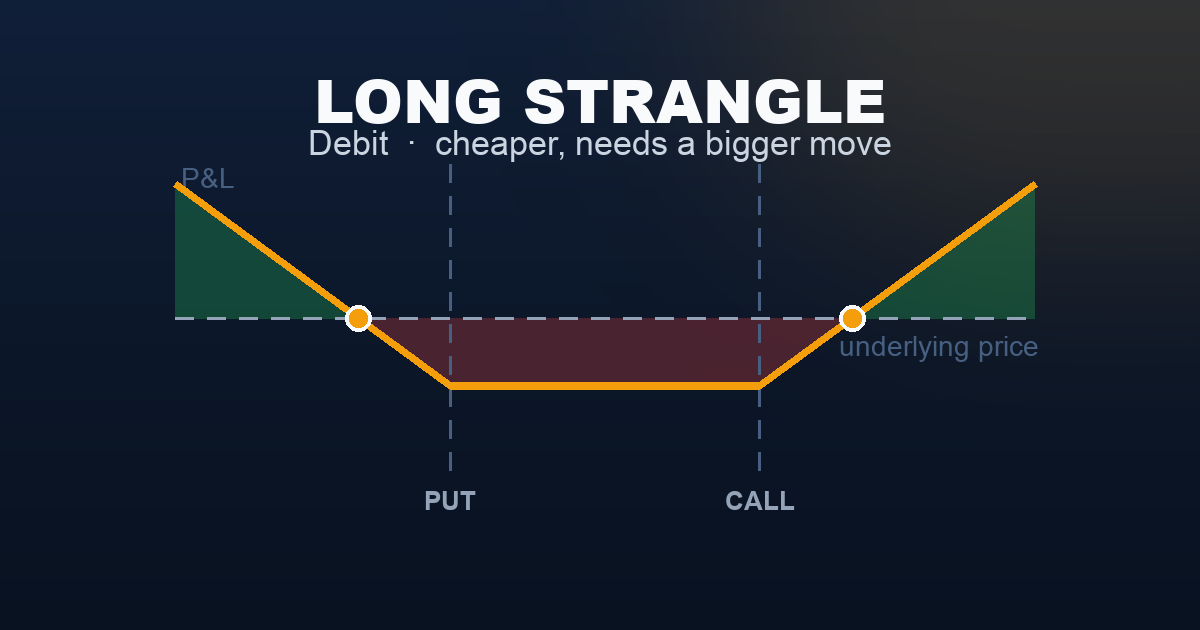

The strangle’s flat loss floor — the zone between the two strikes — is its visual signature. Unlike the straddle’s single point of maximum loss (the ATM pin), the strangle has a loss plateau spanning the entire range from the put strike to the call strike. SPX anywhere inside that zone at expiration produces the same full debit loss. This zone is the price paid for the reduced entry cost.

Setup & Execution

Legs:

- Leg 1 (Buy): 1 OTM call above the current underlying price

- Leg 2 (Buy): 1 OTM put below the current underlying price

Both legs: same underlying, same expiration, different strikes.

Strike selection: The defining choice is how far OTM to go on each leg. Closer strikes (25 points OTM each side for SPX) approach straddle cost and probability. Wider strikes (75–100 points OTM each side) dramatically reduce cost but require extreme moves to profit.

Common approaches:

- 25–30 delta strikes: The most balanced setup. Each leg roughly 25–30 delta — not deeply OTM, not ATM. Costs roughly 30–40% less than the ATM straddle on the same expiration. The standard starting point for event-driven strangles.

- 10–15 delta strikes: A cheap, high-leverage tail bet. Very inexpensive, but requires a large surprise move. Best used for defined-risk speculation around high-uncertainty events where a moderate move is insufficient.

For a symmetric, non-directional strangle, match the call and put strikes equidistant from the current price. A slight directional bias can be introduced by widening the side you’re less confident about.

Expiration selection: Identical to the straddle — event-driven:

- 30–45 DTE: Standard catalyst window with manageable daily theta in the early weeks

- 7–21 DTE: Pre-event targeting, maximum efficiency when a catalyst falls within the window

- Avoid 0 DTE: OTM premium is too thin; only extraordinary intraday moves produce profit

SPX Example — Entry:

Trade:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Long call | 7,550 | Buy | −$2,150 |

| Long put | 7,450 | Buy | −$2,150 |

| Total | −$4,300 (debit) |

- Net debit: $43.00 per contract = $4,300 total paid

- Max profit: Unlimited on the upside; very large on the downside (bounded only by SPX reaching zero)

- Max loss: $4,300 (any SPX close between 7,450 and 7,550 at expiration)

- Upper breakeven: 7,550 + 43 = 7,593

- Lower breakeven: 7,450 − 43 = 7,407

SPX must close above 7,593 or below 7,407 at expiration for the trade to be profitable.

Compare to the ATM straddle: A long straddle at the 7,500 strike would cost approximately $7,200 with breakevens at 7,428 and 7,572. This strangle costs $2,900 less but requires an additional 43 points of movement in either direction.

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,350 | +$10,000 |

| 7,407 (lower breakeven) | $0 |

| 7,450 (put strike) | −$4,300 |

| 7,500 (ATM — inside loss zone) | −$4,300 |

| 7,550 (call strike) | −$4,300 |

| 7,593 (upper breakeven) | $0 |

| 7,650 | +$10,000 |

The U-shape with a flat bottom is the long strangle’s signature. The flat loss floor spans the full range between the put strike (7,450) and the call strike (7,550) — any close within this zone at expiration is a full debit loss. The two rising arms begin at each OTM strike and reach breakeven further out before turning profitable.

This flat floor distinguishes the strangle from the straddle. In a straddle, maximum loss occurs at only one point — the ATM pin. In a strangle, maximum loss occurs across the entire range between the two OTM strikes. That range is the dead zone: a move into it from the current price produces no profit.

The Buyer vs Seller Reality

The natural counterpart to the long strangle is the Short Strangle — the seller who collects the same debit as a credit, profiting when SPX stays inside the range between the two OTM strikes.

| Long Strangle (Buyer) | Short Strangle (Seller) | |

|---|---|---|

| Probability of Profit | ~25–35% | ~65–75% |

| Max Profit | Unlimited / very large | Capped: premium collected |

| Max Loss | Capped: debit paid | Unlimited on both sides |

| Flat loss/profit zone | Between the two OTM strikes | Between the two OTM strikes |

| Theta impact | Enemy — daily erosion | Ally — daily income |

| Vega impact | Ally — rising IV helps | Enemy — rising IV hurts |

The strangle buyer has a lower probability of profit than the straddle buyer (25–35% vs 30–40%) because the breakevens are further away. But the debit risked is smaller. The expected value of a well-timed strangle — entered before a genuine volatility catalyst when IV is cheap — can be comparable to or better than a straddle on a risk-adjusted basis.

Understanding the Greeks

Net Delta (near zero at entry): An OTM call at approximately 25 delta and an OTM put at approximately −25 delta produce a net delta near zero at entry. The position is non-directional. As SPX moves toward one strike, the winning leg’s delta grows while the losing leg’s further shrinks toward zero — the position gradually develops a directional lean in the direction of the move.

Net Gamma (positive — but less than a straddle): Long gamma means the strangle’s delta accelerates as SPX moves. Because the strikes are OTM, gamma is lower at entry than for an ATM straddle. Gamma increases as SPX moves toward one of the OTM strikes, and accelerates sharply once it moves through a strike into the money. The strangle has two gamma acceleration points — one at the put strike (downside) and one at the call strike (upside). The straddle starts at peak gamma; the strangle must travel to reach it.

Net Vega (strongly positive — the IV bet): Both legs are long options, so both benefit from rising implied volatility. A VIX spike inflates both legs simultaneously, often producing significant mark-to-market gains before SPX has moved enough to cross a breakeven. Entering when IV is low (VIX 13–17) before a known catalyst that could spike it is the structural edge of any long volatility position — and the strangle’s lower debit makes this edge more capital-efficient than the straddle.

IV crush is the primary risk: if the catalyst resolves without surprising the market, VIX collapses and both OTM legs deflate rapidly, often producing a near-total loss. Exiting the same day the catalyst resolves preserves whatever residual value remains.

Net Theta (negative — smaller in absolute terms than a straddle): Two long OTM options decay, but at a slower rate than two long ATM options. OTM options carry less time value, so daily theta is lower. For a $4,300 strangle at 30 DTE, net theta is roughly −$55 to −$80 per day versus −$100 to −$145 for a $7,200 ATM straddle. The strangle decays more slowly — which is why it can be more practical for longer pre-catalyst positioning when the event is still weeks away.

Net Rho (≈ 0): The call’s positive rho and the put’s negative rho approximately offset at similar delta magnitudes. Negligible for standard 30–45 DTE strangles.

Trade Management

Rule 1 — Profit target: 50–100% gain on the debit

Because the strangle starts further OTM, a percentage gain requires a more meaningful SPX move than for a straddle. Many traders target 100% or more — a double — because the move required to reach breakeven already represents a significant market event. Set profit targets in advance and close immediately when reached.

Rule 2 — Exit the same day the catalyst resolves

Identical to the straddle rule: close the position the day the binary event occurs. If a large move materialised, take the profit before the winning leg’s IV collapses. If the market barely moved, close before IV crush eliminates the remaining value. The thesis ends when the catalyst resolves.

Rule 3 — Stop loss: 25–30% of debit

If the strangle declines 25–30% in value with no catalyst approaching, close it. A $1,075–$1,290 loss on a $4,300 strangle with no trigger for a move is better than holding for a full $4,300 loss. Residual premium can occasionally recover if IV expands, but buying time with theta drain is a negative-expectancy activity without a clear catalyst.

Rule 4 — Time-based close: 14 DTE

Close no later than 14 days before expiration. In the final two weeks, theta decay on OTM options accelerates while the probability of the required large move diminishes. The strangle is even more sensitive to time decay near expiration than the straddle because OTM options have no intrinsic value to anchor their price.

Real-World Example

The setup: Non-Farm Payrolls (NFP) report is due in 5 days. Employment data has been mixed — three consecutive months of surprise results. The market is pricing in a modest variance, but historical NFP surprises have occasionally exceeded 100,000 jobs versus consensus. VIX at 16.5 is below recent averages. SPX has been rangebound for 8 trading days in a 45-point band.

Trade:

- Buy SPX 7,550 Call (14 DTE): $11.50 = $1,150

- Buy SPX 7,450 Put (14 DTE): $11.50 = $1,150

- Total debit: $23.00 = $2,300

- Upper breakeven: 7,573 | Lower breakeven: 7,427

NFP day (5 days later): NFP comes in at +312,000 jobs — a massive upside surprise versus the 162,000 consensus. SPX gaps up 78 points, opening at 7,576 and closing at 7,592.

| Leg | Entry | NFP close |

|---|---|---|

| Call 7,550 | $11.50 | $48.50 |

| Put 7,450 | $11.50 | $0.80 |

| Strangle total | $23.00 | $49.30 |

- Strangle value: $4,930

- Profit: +$2,630 (114% gain on $2,300 debit)

Close the entire strangle the morning after NFP, before volatility starts to mean-revert. The call moved significantly into the money; the put retained a small residual from remaining time value.

The insufficient-move scenario:

NFP comes in at +148,000 — a slight miss versus the 162,000 consensus. SPX declines 14 points to 7,484. No breakeven crossed.

| Leg | Entry | NFP day |

|---|---|---|

| Call 7,550 | $11.50 | $2.50 |

| Put 7,450 | $11.50 | $3.50 |

| Strangle total | $23.00 | $6.00 |

VIX falls from 16.5 to 12.8 as event risk resolves.

- Strangle value: $600

- Loss: −$1,700 (74% of debit)

Close immediately — the remaining $600 will continue to decay to zero with no further catalyst. The 14-point SPX move stayed inside the dead zone, and IV crush took the rest.

When to Use This Strategy

Best conditions:

- A known binary catalyst is approaching where outcome uncertainty is high and the expected move could be large (NFP, FOMC, major earnings, elections)

- VIX is below recent averages — implied volatility is relatively cheap

- You want lower capital at risk than a straddle provides, and accept lower probability of profit in exchange

- You can exit immediately when the catalyst resolves

Prefer the strangle over the straddle when:

- Premium is expensive relative to recent IV levels — the cheaper strangle entry reduces IV crush impact

- A slight directional bias exists — you can widen one side more than the other while keeping the same total debit

- Account size constraints make the straddle debit too large as a percentage of equity

Prefer the straddle over the strangle when:

- You want the highest probability of capturing any significant move, including moderate ones

- The catalyst is expected to produce a moderate but not extreme move — the straddle’s closer breakevens still profit

- ATM liquidity is significantly better than OTM strikes

Avoid when:

- IV is already elevated — the strangle is more sensitive to IV crush than the straddle because both legs are entirely extrinsic value

- No clear catalyst is approaching — naked theta decay on two OTM options with no trigger is a reliable path to a full loss

- The expected move is known to be moderate — if consensus expects a 25-point SPX move and your strangle breakevens are 30+ points away, the base case produces a full loss

Ideal VIX level: Below 16. The strangle’s edge is maximised when IV is cheapest. Above 20, the entry is expensive and the probability of an IV-crush loss outweighing the directional gain increases substantially.

Strategy Ladder — Next Steps

Built from: Long Call + Long Put — placed at different OTM strikes rather than a single ATM strike. Understanding each component separately clarifies why the flat loss floor exists and how each leg contributes.

The ATM, higher-conviction version: → Long Straddle — buy both options at the same ATM strike. Higher debit, breakevens closer to the current price, higher probability of profit on a moderate move. The straddle is the strangle with the dead zone eliminated: both strikes at the same point means there is only one max-loss price, not a range.

The seller’s mirror: → Short Strangle — sell the same OTM call and OTM put, collect the credit, and profit when SPX stays inside the range. The seller wins approximately 65–75% of the time. Unlimited loss risk on both sides without defined-risk wings.

The defined-risk seller version: → Iron Condor — a short strangle with protective long wings added. Caps the unlimited losses of the short strangle at the cost of reduced credit. The most commonly traded professional income structure.

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.