30-Second Summary

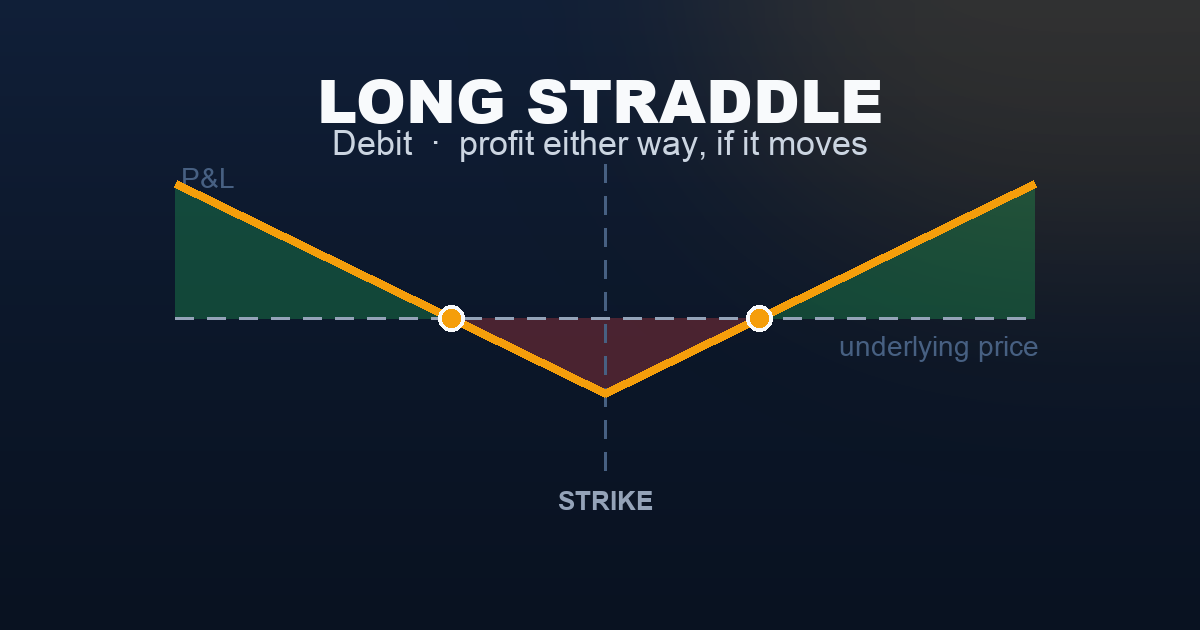

A long straddle buys an at-the-money call and an at-the-money put at the same strike and expiration, paying a net debit for both. You profit if the underlying moves far enough in either direction — up past the upper breakeven or down past the lower breakeven — by expiration. If the underlying stays near the strike, both options lose value and you lose the entire debit. Direction doesn’t matter; magnitude does.

This is the buyer’s pure volatility bet. You’re not predicting which way the market moves — you’re betting it moves significantly. The enemy is time decay and IV collapse, not direction.

What Is a Long Straddle?

A long straddle has one job: to profit from a large move.

Think of it as buying insurance against both outcomes simultaneously — upside and downside. You pay a fixed premium (the total debit) to participate in whichever direction the market ultimately chooses. If the market goes nowhere, you lose that premium. If the market makes a large move, you win on one leg while the other approaches zero.

The analogy: imagine you’re watching a trial verdict that will either send stock prices sharply higher or much lower, but you have no idea which way it goes. A straddle lets you buy tickets for both outcomes. One ticket will be worthless, but the other will more than cover the cost of both — if the verdict produces a large enough market reaction.

The straddle differs from simply buying a call or put in one critical way: direction is irrelevant. A long call profits only from a rally. A long put profits only from a decline. The long straddle profits from the size of movement regardless of direction. This makes it ideal for event-driven trading — earnings, Fed decisions, CPI releases, elections — where outcome uncertainty is high but the amount of price movement is expected to be substantial.

The risk is equally clear: if nothing happens — if the underlying pins near the strike through expiration — the full premium paid is lost. Time decay erodes both legs simultaneously, making patience expensive. The trade must move, and it must move enough.

Setup & Execution

Legs:

- Leg 1 (Buy): 1 ATM call at the strike nearest to the current underlying price

- Leg 2 (Buy): 1 ATM put at the same strike as the call

Both legs: same underlying, same expiration, same at-the-money strike.

Strike selection: The straddle must be placed at-the-money for the position to be non-directional at entry. The ATM call carries a delta of approximately +0.50 and the ATM put approximately −0.50 — together, net delta is close to zero. The position reacts symmetrically to moves in either direction.

- Use the strike nearest to the current underlying price. For SPX at 7,497, use the 7,500 strike rather than 7,450 or 7,550.

- Avoid splitting the strikes. Using different call and put strikes creates a Long Strangle — a related structure that’s cheaper but requires a larger move to profit.

Expiration selection:

- 30–45 DTE: Standard swing straddle. Enough time for the catalyst to develop; manageable theta decay in the early weeks.

- 7–21 DTE: Targeted catalyst trades (earnings, FOMC). Higher gamma, cheaper premium, but little time buffer if the catalyst is muted.

- Avoid 0 DTE: Premium is almost entirely intrinsic. A same-day straddle requires an extreme intraday move and offers no buffer for timing.

Position sizing note: The maximum loss is the full debit paid — there is no defined-risk offset like a spread provides. Size so that the total debit at risk represents no more than 2–3% of account equity.

SPX Example — Entry:

Trade:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Long call | 7,500 | Buy | −$2,500 |

| Long put | 7,500 | Buy | −$2,500 |

| Total | −$5,000 (debit) |

- Net debit: $50.00 per contract = $5,000 total paid

- Max profit: Theoretically unlimited (upside); very large (downside, bounded only by SPX reaching zero)

- Max loss: $5,000 (if SPX pins exactly at 7,500 at expiration)

- Upper breakeven: 7,500 + 50 = 7,550

- Lower breakeven: 7,500 − 50 = 7,450

SPX must close above 7,550 or below 7,450 at expiration for the trade to be profitable.

The Payoff Diagram

| SPX at Expiry | P&L |

|---|---|

| 7,350 | +$10,000 |

| 7,400 | +$5,000 |

| 7,450 (lower breakeven) | $0 |

| 7,500 (strike — max loss) | −$5,000 |

| 7,550 (upper breakeven) | $0 |

| 7,600 | +$5,000 |

| 7,650 | +$10,000 |

The V-shape is the long straddle’s signature. The bottom of the V sits at the ATM strike — where both options expire worthless and the full debit is lost. The two breakevens are equidistant above and below the strike. Beyond each breakeven, profit grows linearly without a cap.

The Buyer vs Seller Reality

The long straddle is a buyer’s position — you pay premium and need a move. The natural counterpart is the Short Straddle — the seller who collects the same premium hoping the market stays quiet.

| Long Straddle (Buyer) | Short Straddle (Seller) | |

|---|---|---|

| Probability of Profit | ~30–40% | ~60–70% |

| Max Profit | Unlimited / very large | Capped: premium collected |

| Max Loss | Capped: debit paid | Unlimited on both sides |

| Who wins most often? | Rarely | Usually |

| Who wins bigger when right? | Buyer — dramatically | — |

| Theta impact | Enemy — daily erosion | Ally — daily income |

| Vega impact | Ally — rising IV helps | Enemy — rising IV hurts |

The straddle buyer loses money the majority of the time. This is not a failure of strategy — it’s the structure of optionality. Most days, markets don’t move enough to cover the debit. The straddle buyer is waiting for the outlier: the earnings miss, the surprise Fed decision, the macro shock. When that outlier arrives, one side of the straddle delivers a return that covers multiple losing trades.

Think of the straddle buyer as the policyholder — paying premiums regularly, expecting most of them to expire worthless, waiting for the event that makes them all worthwhile. The seller is the insurance company: collecting those premiums consistently, profiting most months, and occasionally facing a catastrophic claim.

The question isn’t whether the straddle wins more often than it loses — it won’t. The question is whether the wins are large enough, and the losses disciplined enough, that the overall expectancy is positive. That demands entering when IV is cheap, selecting the right catalysts, and exiting quickly after them.

Understanding the Greeks

Net Delta (near zero — the non-directional core): At entry, the ATM call carries a delta of approximately +0.50 and the ATM put approximately −0.50. Together, net delta is close to zero — the straddle has no initial directional preference. As SPX moves, the winning leg’s delta grows while the losing leg’s delta shrinks toward zero. The position develops a directional lean in the direction of the move. This is gamma at work.

Net Gamma (strongly positive — the buyer’s engine): Long gamma is the defining characteristic of the straddle and the reason buyers accept a sub-50% win rate. Positive gamma means delta increases faster as the underlying moves. A 10-point SPX rally increases the call’s delta more than it reduces the put’s delta — net delta turns positive, and further rallies produce accelerating profits. The same mechanism applies on the downside. Large moves generate disproportionately large profits because gamma compounds the directional exposure automatically.

Gamma increases as expiration approaches. In the final week, a straddle near the money sees violent delta swings on small intraday moves — this is why holding straddles into the last 10–14 days is rarely advisable without a clear catalyst still pending.

Net Vega (strongly positive — the IV bet): Both legs are long options. Both benefit from rising implied volatility. A VIX spike after entry inflates the value of both legs, often before SPX has moved significantly. This is why straddles entered before catalysts at low IV can profit from the anticipation of movement, not just from the movement itself. Conversely, when a catalyst passes and IV collapses — IV crush — both legs deflate simultaneously. IV crush is the most common cause of straddle losses on earnings trades: the position paid for a move, the move happened, but IV collapse outweighed the directional gain.

Net vega makes the long straddle as much about implied volatility as about magnitude of movement. Entering when IV is cheap (VIX below 16) is structurally superior to entering when IV is already elevated (VIX above 24).

Net Theta (strongly negative — the daily enemy): Two long ATM options decay at among the fastest rates of any options position. For a $5,000 straddle at 30 DTE, net theta is roughly −$70 to −$100 per calendar day. Every day without a meaningful move is money lost. Over two weeks at −$85 daily: the straddle loses approximately $1,190 from theta alone — nearly a quarter of the debit — before any price movement factor is applied.

This is why timing the catalyst correctly matters more than the catalyst itself. Entering a 30-day straddle 25 days before earnings and watching the stock drift sideways — then finally moving on earnings day — often results in a loss despite a large post-earnings move. Theta consumed the premium the move tried to recover.

Net Rho (ρ = ∂C/∂r − ∂P/∂r ≈ 0): The call’s positive rho and the put’s negative rho approximately offset each other at the same ATM strike. Rho is negligible for 30–45 DTE straddles. For long-dated LEAPS straddles (90+ DTE), rising rates give a slight advantage to the call leg; falling rates favour the put — but this is a second-order effect that rarely drives meaningful P&L at standard durations.

Trade Management & Adjustments

Rule 1 — Profit target: close at 25–50% gain on the debit

A $5,000 straddle that grows to $6,250 (25% gain = +$1,250) or $7,500 (50% gain = +$2,500) should be closed. The biggest straddle management mistake is holding after a catalyst has already resolved — IV crush begins immediately post-event and removes premium faster than any further directional move adds it back. Take the win and redeploy.

Rule 2 — Exit the same day the catalyst resolves

The moment an earnings report, FOMC decision, or other binary event passes, the trade’s thesis has resolved. Close the position regardless of P&L. If a large move materialised, take the profit. If the underlying barely moved, take the loss before IV crush removes the remaining value. Holding a straddle after its catalyst is the most reliable way to turn a manageable loss into a full debit loss.

Rule 3 — Stop loss: 25–30% of debit

If the straddle loses 25–30% of its value and there’s no catalyst approaching, close it. A $5,000 straddle at a $1,250–$1,500 loss with no trigger in sight is decaying toward zero with no recovery mechanism. Accepting a partial loss early is nearly always better than holding for a move that doesn’t come.

Rule 4 — Time-based close: 14 DTE

Close no later than 14 days before expiration regardless of P&L. The final two weeks bring accelerating theta decay and increasingly violent gamma swings. The time value remaining rarely justifies the management complexity. If the expected move hasn’t happened by 14 DTE, close and accept the loss.

Rule 5 — Leg management (advanced)

If one leg is deeply profitable and the other near worthless, closing the losing leg and holding the winner converts the straddle into a directional position. This can make sense when the directional move is strongly established and continuing. But it introduces naked directional risk — ensure the remaining leg is sized and monitored accordingly.

What to avoid:

- Entering when IV is already elevated (VIX 24+) — premium is expensive and IV mean-reversion hurts even when SPX moves

- Holding through expiration — the full debit loss requires a perfect pin at exactly the strike; the path there involves severe theta drain

- Doubling down on a losing straddle — adding size to a theta-burning position without a catalyst is among the most common account-shrinking habits

Real-World Example

The setup: FOMC meeting in 6 days. The Fed is expected to hold rates, but the tone around future policy is genuinely uncertain. VIX at 16.2 is below its 30-day average of 18.5 — options are relatively cheap. SPX has been in a 55-point range for two weeks, compressing daily ranges and declining volume. This is textbook straddle territory: known binary catalyst, cheap IV, coiled price action.

Trade:

- Buy SPX 7,500 Call expiring in 14 days: $23.00 = $2,300

- Buy SPX 7,500 Put expiring in 14 days: $22.00 = $2,200

- Total debit: $45.00 = $4,500

- Upper breakeven: 7,545 | Lower breakeven: 7,455

FOMC day (6 days later): The Fed holds rates but signals an aggressive tightening path — a hawkish surprise. SPX drops 68 points in 90 minutes, closing at 7,432.

| Leg | Entry | FOMC close |

|---|---|---|

| Call 7,500 | $23 | $0.50 |

| Put 7,500 | $22 | $71.50 |

| Straddle total | $45 | $72.00 |

- Straddle value at close: $7,200

- Profit: +$2,700 (60% gain)

The trader exits the entire straddle within 30 minutes of the FOMC statement — before VIX starts to mean-revert. Holding overnight risks IV collapse as the initial panic fades.

The no-move scenario:

FOMC is perfectly in line with expectations. SPX moves 8 points on the statement, closes at 7,508. No surprise — no catalyst.

Next morning: VIX falls from 16.2 to 12.4 (IV crush). Call worth $4.00, Put worth $4.50. Straddle total: $850.

- Loss: −$3,650 (81% of debit)

The loss is not from SPX moving against the trade — it’s from IV collapse. The position that paid $4,500 for volatility saw that volatility evaporate the moment the catalyst resolved without surprise. The correct action was closing the straddle immediately after the FOMC statement regardless of direction, capturing whatever premium remained before IV crush eliminated it.

When to Use This Strategy

Best conditions:

- A known binary event is approaching: earnings, FOMC, CPI, non-farm payrolls, elections, regulatory decisions

- Implied volatility is below its 30-day or 60-day average — entering when options are cheap relative to recent norms

- Recent price action shows compression: tightening daily ranges, declining volume, converging moving averages — a coiled spring before a release

- You can exit the same day the catalyst resolves — the thesis ends with the event

Avoid when:

- VIX or the stock’s IV is already elevated (VIX 22+) — premium reflects large expected moves that may not materialise, and any subsequent IV mean-reversion erodes the position before SPX can move enough

- No catalyst exists within the expiration window — pure theta drag with no identifiable trigger for the required move

- The catalyst is already known and priced in — markets are forward-looking; if everyone knows the move is coming, the straddle is expensive to enter

- You cannot monitor the position during the event — straddles require an active exit decision at the moment of catalyst resolution

Ideal VIX level: Below 16. In the 12–16 range, options are pricing in relatively modest moves. A straddle entered at VIX 14 benefits from any subsequent VIX expansion — the position is long volatility by nature. Above VIX 22, the straddle is structurally expensive and IV mean-reversion creates a headwind even when the trade works directionally.

The long straddle is not a passive position. It’s an event-driven, tactical trade with a hard-wired thesis expiration. Enter before the catalyst. Exit when the catalyst resolves. Don’t hold waiting for a second wave that rarely comes.

Strategy Ladder — Next Steps

Built from: Long Call + Long Put — the straddle is simply both bought simultaneously at the same strike. Understanding each leg’s individual behaviour is the prerequisite for understanding why the straddle works and when it fails.

The wider, cheaper version: → Long Strangle — instead of both options at the same ATM strike, buy an OTM call above the market and an OTM put below it. Cheaper to enter because both legs start out-of-the-money, but requires a larger move to profit. Lower cost, lower probability, same event-driven logic.

The seller’s mirror: → Short Straddle — sell the same ATM call and put you’d buy in this strategy. Collects the premium and profits if SPX stays near the strike. Exposed to unlimited losses if SPX moves far in either direction. High-probability, high-risk — the exact inverse of this article.

The defined-risk seller version: → Iron Butterfly — add protective long wings to a short straddle. The iron butterfly caps the unlimited losses of the short straddle at the cost of reduced premium collected. Mechanically, it’s a short straddle with insurance.

The range-bound alternative: → Iron Condor — if this article represents a bet that the market will move big, the iron condor is the bet that it won’t. Wider short strikes, lower credit, higher probability of keeping the full profit. The conceptual opposite of the long straddle.

This content is for educational purposes only. Options trading involves significant risk of loss. Past performance is not indicative of future results.