30-Second Summary

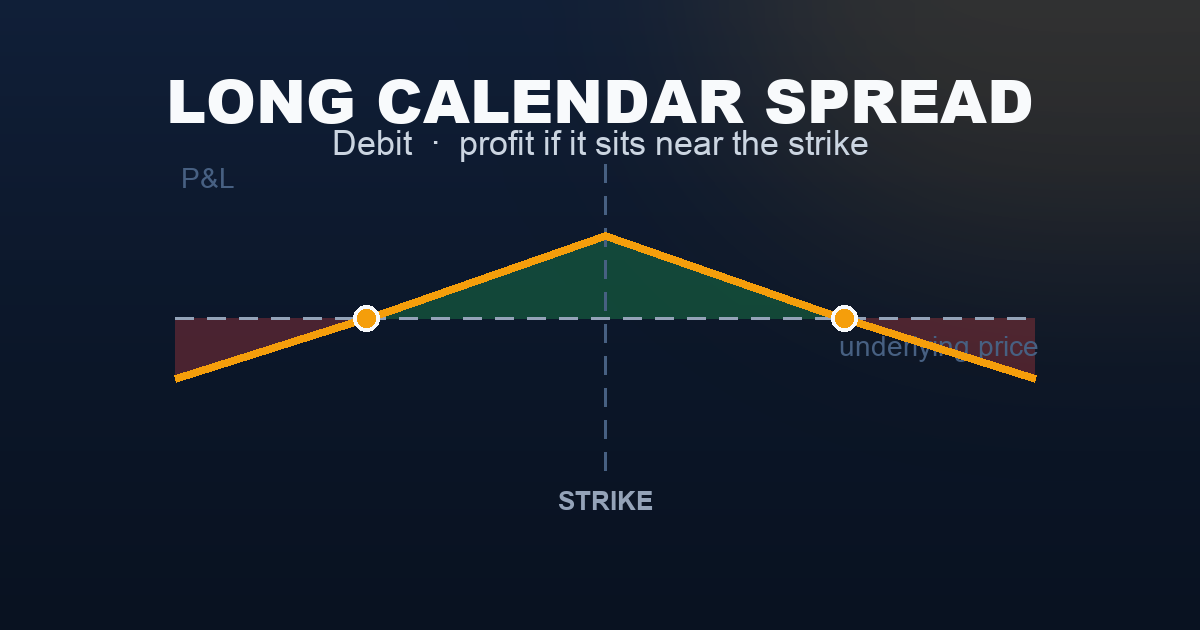

A long calendar spread buys a far-month option and sells a near-month option at the same strike, paying a net debit. The near-month option decays faster than the far-month option — this theta differential is the edge. If the underlying stays near the strike through the near-month expiration, the near-month expires worthless while the far-month retains much of its value, producing a profit. If the underlying moves sharply away from the strike, the theta differential collapses and the debit is largely lost.

This is a time-spread strategy, not a directional bet. The profit driver is the difference in time decay rates between two expirations, not the direction of the underlying. It also benefits from rising implied volatility (long vega), making it useful when IV is low and expected to rise.

What Is a Long Calendar Spread?

A calendar spread (also called a time spread or horizontal spread) uses the same strike across two different expirations:

- Buy: 1 far-month option (60 DTE) at the target strike — the anchor position that retains value

- Sell: 1 near-month option (30 DTE) at the same strike — the decaying position you are harvesting

The key mechanic: ATM options decay at a rate proportional to 1/√(DTE). A 30-day option decays approximately 1.4× faster than a 60-day option per dollar of time value. By selling the faster-decaying near-month and holding the slower-decaying far-month, you collect the theta differential as profit — provided the underlying stays cooperative.

The two ways this trade makes money:

- Theta differential: The near-month decays to zero faster than the far-month loses value. This is the core profit mechanism.

- Vega expansion: If IV rises after entry, the far-month (with more time and more vega) gains more value than the near-month. The long calendar is net long vega — it benefits from IV expansion.

Important caveat: The payoff diagram shown below is an approximation at near-month expiration assuming unchanged implied volatility. In practice, P&L depends significantly on IV at expiration, the term structure of volatility (whether near-month and far-month IVs move differently), and the exact level of the underlying at near-month expiry. Calendar spreads are among the most IV-sensitive structures in options trading.

Setup & Execution

Legs:

- Leg 1 (Buy): 1 ATM or near-ATM option at the far-month expiration (60 DTE)

- Leg 2 (Sell): 1 same-strike option at the near-month expiration (30 DTE)

Both legs: same underlying, same strike.

Option type:

- Call calendar: Use calls at an ATM or slightly OTM strike. Profits if the underlying stays at or slightly above the strike.

- Put calendar: Use puts at an ATM or slightly OTM strike. Profits if the underlying stays at or slightly below the strike.

- Double calendar: Run both a call and put calendar at different strikes simultaneously, widening the profit zone.

Strike selection:

- Place both strikes at-the-money or nearest the current underlying price. ATM options have the highest theta and vega, maximising the time-decay differential. A slightly OTM strike adds a small directional lean.

Expiration selection:

- Near-month: 21–45 DTE. This is the option you are selling — enough time value to justify the structure, close enough to decay meaningfully before expiry.

- Far-month: 45–90 DTE, typically 2× the near-month DTE. The far-month must have enough time value to retain meaningful value when the near-month expires.

SPX Example — Entry:

Trade:

| Leg | Strike | Expiry | Action | Premium |

|---|---|---|---|---|

| Long call | 7,500 | 60 DTE (far month) | Buy | −$8,600 |

| Short call | 7,500 | 30 DTE (near month) | Sell | +$5,750 |

| Total | −$2,850 |

- Net debit: $28.50 per contract = $2,850 total paid

- Max profit (approximate): ~+$2,850 when SPX pins at 7,500 at near-month expiry

- Approximate breakevens: 7,450 (lower) and 7,550 (upper)

- Max loss (approximate): ~$2,850 (the net debit, when SPX moves far from 7,500)

Actual P&L at near-month expiration depends heavily on implied volatility at that time. The values shown assume unchanged IV.

The Payoff Diagram

Approximate P&L at near-month expiration, assuming unchanged implied volatility.

| SPX at Near-Month Expiry | P&L (approximate) |

|---|---|

| 7,350 | −$2,150 |

| 7,400 | −$1,700 |

| 7,450 (lower BE) | $0 |

| 7,500 (ATM — max profit) | ≈ +$2,850 |

| 7,550 (upper BE) | $0 |

| 7,600 | −$1,700 |

| 7,650 | −$2,150 |

The hill shape is the calendar spread’s signature — a profit dome centred at the strike, sloping to losses on both wings. Unlike the iron condor’s flat profit plateau, the calendar’s peak is a single point. Also unlike most other strategies, there is no hard maximum loss — the far-month option always retains some residual value, even when deeply OTM.

Long vs Short: Two Ways to Trade a Calendar

| Long Calendar (This Article) | Short Calendar | |

|---|---|---|

| Structure | Buy far, sell near | Sell far, buy near |

| Net premium | −$2,850 debit paid | +$2,850 credit received |

| Profit requires | SPX stays near the strike | SPX moves far from the strike |

| Theta | Positive (net) — earns time decay differential | Negative (net) — pays time decay differential |

| Vega | Positive — benefits from IV expansion | Negative — benefits from IV collapse |

| Ideal condition | Calm, range-bound, low IV expected to rise | Volatile, large move expected, high IV expected to fall |

| Payoff shape | Hill (profit at ATM, loss on wings) | Valley (loss at ATM, profit on wings) |

Understanding the Greeks

Net Delta (near zero at ATM entry): A calendar spread with both legs at the same ATM strike has near-zero net delta at entry — the long and short calls partially cancel. As SPX drifts from the strike, the position develops a delta bias in the direction of the move (driven by the different deltas of each option as they go ITM/OTM). This delta drift is typically small and manageable.

Net Theta (positive — the edge): The near-month option decays faster per day than the far-month. Net theta is positive — every day that passes with SPX near the strike earns the theta differential. For a $2,850 debit calendar at 30/60 DTE, net theta might earn $30–$55 per day. Importantly, theta accelerates as the near-month approaches expiration — the final week of the near-month is the most productive theta harvest window.

Net Vega (positive — the IV exposure): The far-month option has significantly more vega than the near-month. Net vega is positive: if VIX rises after entry, the far-month gains more value than the near-month, increasing the spread’s mark-to-market value. This is the calendar’s second profit mechanism beyond theta. Entering a calendar when IV is low and expected to rise (before an anticipated volatility event) captures both theta differential AND vega expansion.

Net Gamma (negative): The near-month short option has more gamma than the far-month long option at the same strike. Net gamma is slightly negative — if SPX moves rapidly away from the strike, the spread loses value faster than a pure theta calculation would suggest. Large gap moves are the calendar spread’s primary risk.

Net Rho (near zero): The call legs’ rho effects approximately offset each other. Negligible.

Trade Management

Close or roll before near-month expiration: Never hold the near-month leg to expiration while still long the far-month. At near-month expiry, if SPX is ATM, the short call may be exercised (or auto-settled for index options) creating a naked long position in the far-month. Close both legs 1–3 days before near-month expiration, or roll the near-month to a new cycle.

Profit target: 25–50% of max estimated gain: If the position reaches 25–50% of its estimated maximum P&L (based on current theta differential), close and re-evaluate. The most efficient theta harvest window is the final 1–2 weeks of the near-month — if that window has passed and profit is adequate, there is no reason to roll.

Rolling the near-month (the primary management tool): If SPX stays near the strike and the near-month expires, sell a new near-month call at the same strike and same level of DTE. This creates a rolling calendar — continuously harvesting the theta differential across successive near-month expirations while holding the far-month as the anchor. Rolling extends the profit window as long as SPX cooperates.

Stop loss: close if SPX moves more than one breakeven distance: If SPX moves beyond either approximate breakeven (7,450 or 7,550 in this example), the theta differential has collapsed. Close the position. Rolling the far-month strike to follow SPX (diagonal calendar adjustment) is possible but adds complexity.

IV considerations: If IV rises sharply after entry, the position may show a mark-to-market gain even if SPX has moved slightly. Consider closing early if IV is at an elevated spike — subsequent IV collapse will erode gains. Conversely, if IV collapses after entry (a vega headwind), the long far-month loses value more than the short near-month gains, producing a loss even if SPX stays put.

Real-World Example

Scenario A — The ideal outcome: calm post-Fed market

Fed has held rates for three consecutive meetings. SPX is calm with daily ranges averaging 15 points. VIX at 14 is at a 6-month low. The trader enters a long calendar: buy 60 DTE 7,500 call at $8,600, sell 30 DTE 7,500 call at $5,750, net debit $2,850.

Day 28 (near near-month expiry): SPX at 7,507. VIX has risen slightly to 16 (a small vega tailwind). Near-month call worth $690 to close.

- Far-month call (now 32 DTE, approximately ATM): worth approximately $7,490 (some remaining time value, vega boost from VIX moving from 14 to 16)

- Position value: $7,490 − $690 = $6,800

- Initial cost: $2,850

- Net P&L: +$3,950 (139% of debit, 28 days)

Close both legs. The near-month decayed from $5,750 to $690 (88% decay), while the far-month decayed from $8,600 to $7,490 (only 13% decay). The theta differential and the small vega tailwind produced a substantial return.

Scenario B — The gap failure:

A surprise jobs report shows unexpected wage acceleration. SPX drops 95 points to 7,405 in a single session.

At SPX 7,405 (95 points below the strike, 18 DTE to near-month expiry):

- Near-month call (7,500, 18 DTE): deeply OTM, worth approximately $290 to close

- Far-month call (7,500, 48 DTE): also deeply OTM, worth approximately $1,730

- Position value: $1,730 − $290 = $1,440

- Initial cost: $2,850

- Net loss: −$1,410 (50% of debit)

The spread collapsed because both options lost most of their value as SPX moved far OTM — but the far-month still retained $1,730, softening the loss. Close and exit. The theta differential no longer functions when both options are deep OTM.

When to Use This Strategy

Best conditions:

- VIX is at or near multi-month lows — low IV means cheap debit AND creates the expectation that IV will rise (long vega works in your favor)

- SPX is consolidating in a tight range with no major catalyst expected in the near-month window

- A larger volatility event is expected in the far-month window (e.g., FOMC in 45 days) that will benefit the far-month vega

- You can monitor and roll the near-month systematically

Avoid when:

- VIX is already elevated — you’re paying expensive premiums for both legs, and any IV collapse (your vega enemy) produces losses even if SPX stays still

- A gap-risk event (earnings, FOMC, CPI) falls within the near-month window — the sharp move will collapse the spread value immediately

- The underlying is in a strong trend — a trending market will push SPX away from the strike faster than the theta differential can accumulate

Strategy Ladder — Next Steps

The mirror image: → Short Calendar Spread — sell far, buy near, receive a credit, profit when SPX moves far from the strike. Same strikes, opposite P&L profile.

Similar neutral outlook, defined risk: → Iron Condor — a spread-based neutral strategy with a defined profit zone. No time-structure dependency; all legs expire in the same month.

Similar long-vega exposure: → Long Straddle — buy both ATM call and put in the same expiration. Pure long volatility with no near-month to harvest, but no theta drag either.

The double calendar: Run a call calendar at one strike and a put calendar at another strike simultaneously — this widens the profit zone and reduces directional risk at the cost of higher debit.

This content is for educational purposes only. Calendar spread P&L is an approximation; actual results depend heavily on implied volatility levels at near-month expiration. Options trading involves significant risk of loss. Past performance is not indicative of future results.