On paper, a 0DTE iron condor looks clean. You sell four legs, collect a credit, and let theta do the work. The decay curve is steep, the math is tidy, and the expected value pencils out.

Then the fills come back, and the credit is smaller than the screen promised.

That gap is slippage. It is the difference between the price you should get and the price you actually get, and on same-day options it is larger and more frequent than most new sellers expect. The theta edge is real. So is the execution cost that sits on top of it. Understanding slippage is the difference between the return you model and the return you keep.

What Slippage Actually Is

Two costs get bundled together in casual conversation, and it helps to separate them.

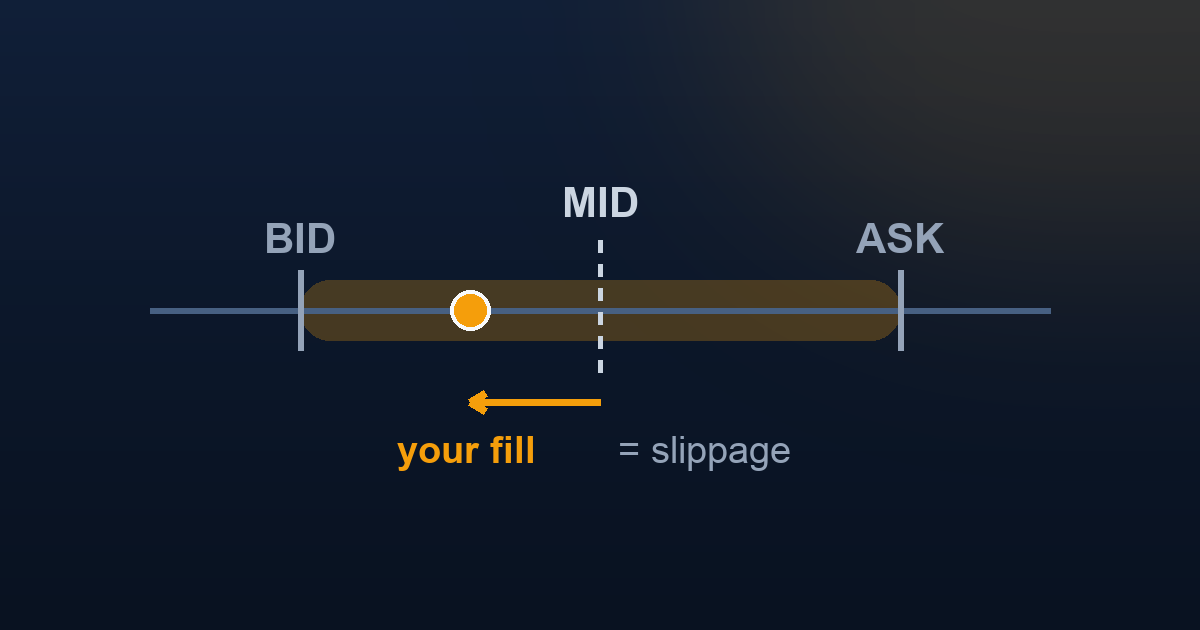

The bid/ask spread is the published gap between what buyers are bidding and what sellers are asking. If a spread shows $2.95 bid / $3.05 ask, the mid-price is $3.00. Sell at the bid and you have already given up a nickel versus mid.

Slippage proper is when the market moves between the moment you decide and the moment you fill — or when your order is large enough to walk through the available size at the top of the book. A marketable order sent into a fast tape can fill several cents worse than the quote you were looking at a second earlier.

In practice the two blur together, because every fill pays some share of the spread and some share of movement. For a seller, both work the same direction: they shrink the credit on the way in and inflate the debit on the way out.

Why 0DTE Is Especially Exposed

Longer-dated options have time premium to cushion small pricing errors. 0DTE does not. Three things make same-day expiry the worst-case environment for execution costs.

Gamma is at its peak. On expiration day, an option’s delta swings violently as price moves through the strike. A 0DTE option that is near-the-money can reprice meaningfully on a one or two point move in SPX. The quote you saw is stale almost immediately, so any hesitation gets paid for in the fill.

Liquidity thins out at the wrong times. The open is fast and wide. The final hour, when theta is richest and the temptation to hold is strongest, is also when spreads on at-risk strikes blow out as market makers price the pin risk. The moments you most want to transact are the moments the book is least friendly.

Multi-leg orders compound it. An iron condor is not one trade. It is four. Each leg has its own bid/ask spread, and a complex order has to find a price that satisfies all four at once.

The Four-Leg Multiplier

This is the piece that surprises people. A single short option pays the spread once. An iron condor pays a slice of it four times.

Assume a modest one-to-two cent edge given up per leg versus mid-price. Spread across the structure:

| Leg | Mid | Realistic fill | Slippage |

|---|---|---|---|

| Short call | $1.80 | $1.78 | -$0.02 |

| Long call | $0.65 | $0.66 | -$0.01 |

| Short put | $1.80 | $1.78 | -$0.02 |

| Long put | $0.65 | $0.66 | -$0.01 |

| Net credit | $2.30 | $2.24 | -$0.06 |

Six cents on a $2.30 credit does not sound like much. It is 2.6% of the credit gone before the trade has done anything — and that is the entry only. Close the position the same way and you pay it again on the exit. A trade you modeled at $2.30 in and $1.15 out (a 50% profit target) can realistically come back as $2.24 in and $1.21 out. The theoretical $1.15 of captured premium becomes $1.03. You kept about 90% of the edge you thought you had.

Now run that drag across hundreds of trades a year. Slippage is not a one-time fee. It is a recurring tax on a high-frequency, low-margin approach, and it lands every single cycle.

A Worked Example

Put rough dollars on it. One SPX iron condor, one contract, profit-target exit:

- Theoretical: sell for $3.00, buy back at $1.50. Captured = $1.50 × 100 = $150.

- With slippage: sell for $2.93, buy back at $1.57. Captured = $1.36 × 100 = $136.

That is $14 of edge surrendered to execution on a single contract — roughly 9% of the modeled profit. Trade five contracts and it is $70. Trade that structure 200 times in a year at five contracts and you are looking at thousands of dollars that never showed up in the backtest, because most backtests fill at the mid and ignore the book entirely.

This is also why a strategy can look profitable in simulation and bleed in practice. The signal was fine. The fills were not.

Why SPX Helps

Not every underlying is equally hostile. SPX is the preferred venue for 0DTE selling partly because its execution costs are among the lowest available.

| Factor | Effect on slippage |

|---|---|

| Deep, liquid market | Large size rests at each price level, so orders rarely walk the book |

| Tight quoted spreads | The penny-to-nickel markets on liquid strikes keep per-leg cost small |

| Daily expirations | Volume concentrates, and concentrated volume means tighter pricing |

| Large notional per point | Fewer contracts needed for a given exposure, so fewer spreads paid |

The same iron condor on a thin, wide-quoted underlying could give up several times the slippage shown above. The instrument choice is itself a cost-control decision. This is one of the quieter reasons the 0DTE iron condor lives on SPX rather than on smaller, choppier names.

How to Keep Execution Costs Down

Slippage can’t be eliminated. It can be managed, and the difference between sloppy and disciplined execution shows up directly in the bottom line.

- Work the mid, don’t cross the spread. Send the complex order as a limit at or near mid-price and give it room to fill. A few seconds of patience often saves the nickel that a marketable order would have paid instantly.

- Avoid the first and last fifteen minutes. The open is wide and the close is gamma-charged. The 9:45–10:30 window most systematic sellers favor isn’t only about premium levels; it’s also where spreads are tightest.

- Size to the book, not just to the account. If your order is larger than the resting size at the top of the book, it will walk into worse prices. Splitting a large order or scaling in keeps each fill closer to the quote.

- Respect event days. Around scheduled data and on high-volatility sessions, spreads widen and quotes go stale faster. Reducing size or sitting out is partly a slippage decision.

- Measure it. Log the mid at decision time against the actual fill. If you don’t track slippage, you can’t tell a pricing problem from a strategy problem — and the two have very different fixes.

The Bottom Line

The theta math is the headline. Slippage is the fine print, and the fine print compounds. A clean-looking 0DTE edge can lose a tenth or more of its value to execution before the first dollar of decay is counted, and it pays that toll on every entry and every exit, every day the system trades.

None of this argues against 0DTE selling. It argues for treating execution as part of the strategy rather than an afterthought. The traders who keep the most of their edge are not the ones with the cleverest entries. They are the ones who give up the least at the fill.

Slippage is only half the friction story. The other half is the flat fee you pay to open and close all four legs — see the commission tax on the 0DTE iron condor for how that fixed cost compounds across a year of trading.

→ Read next: Commission Costs on the Iron Condor | 0DTE Options Trading: The Complete Guide | Option Selling and Its Advantages | Options Greeks — Complete Guide

This content is for educational purposes only. Options trading involves significant risk of loss. 0DTE options carry elevated intraday risk due to gamma. Past performance is not indicative of future results. Consult a qualified financial professional before trading.