30-Second Summary

A Section 1256 contract is a category of instrument in the U.S. tax code — regulated futures and broad-based index options, including SPX, XSP, and VIX options — that gets special treatment: every gain or loss is split 60% long-term and 40% short-term, regardless of holding period. A trade held 30 minutes is taxed mostly at the long-term capital gains rate. For an active index option seller in a high bracket, that one rule can cut the effective tax rate on trading gains by around 10 percentage points versus the same trades on SPY.

What Is a Section 1256 Contract?

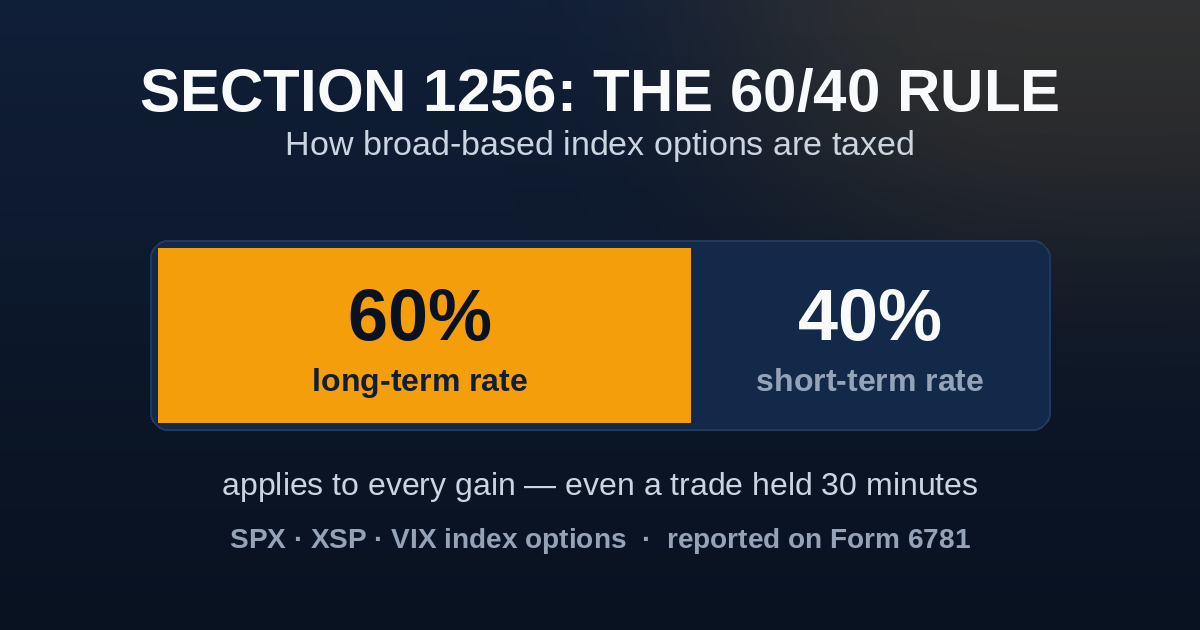

A Section 1256 contract is any instrument the tax code marks to market and taxes under the 60/40 rule: regulated futures contracts, options on futures, and nonequity options — which is where cash-settled, broad-based index options like SPX live. Gains are treated as 60% long-term and 40% short-term no matter how long the position was held.

The category comes from Section 1256 of the Internal Revenue Code, and the practical test for an options trader is simple: is the option written on a broad-based index (SPX, XSP, NDX, RUT, VIX) or on a security (a stock, or an ETF like SPY)? The first group qualifies. The second doesn’t. Same market, same direction, same fill — completely different tax bill.

That distinction is one of the four structural gaps covered in SPX vs SPY Options , and for a frequent trader it’s arguably the biggest one.

How the 60/40 Rule Works

Under normal tax rules, a gain on a position held one year or less is short-term and taxed at your ordinary income rate — up to 37%. Since nobody holds a 0DTE option for a year, every dollar an active SPY option trader makes is short-term by definition.

Section 1256 ignores the holding period entirely. Every gain is split: 60% taxed at your long-term capital gains rate, 40% at your ordinary rate.

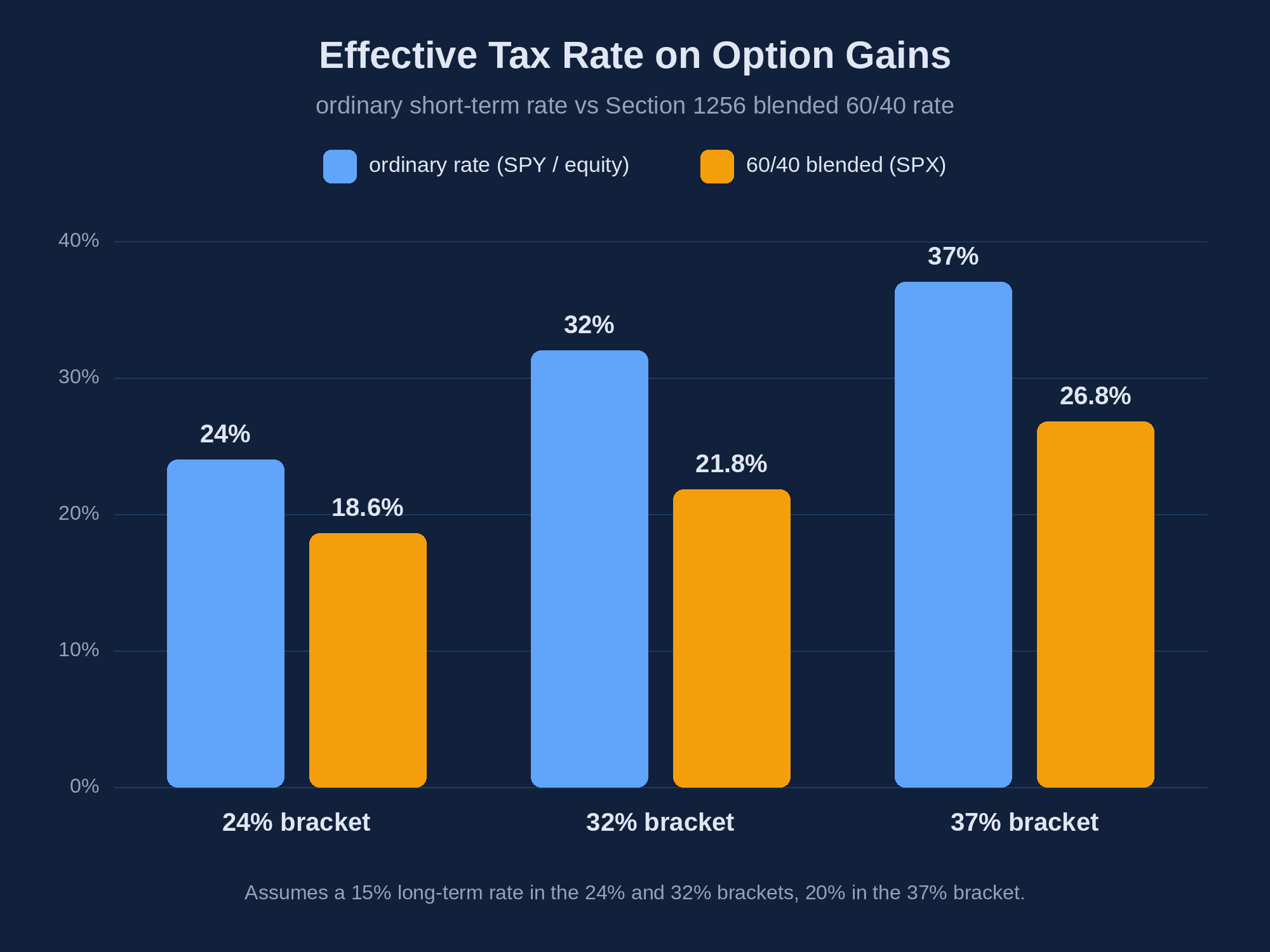

Run the numbers for a trader in the 32% bracket (15% long-term rate) with $50,000 of net option gains for the year, all from trades held under an hour:

| SPY options (standard) | SPX options (Section 1256) | |

|---|---|---|

| Long-term portion | $0 | $30,000 × 15% = $4,500 |

| Short-term portion | $50,000 × 32% = $16,000 | $20,000 × 32% = $6,400 |

| Total federal tax | $16,000 | $10,900 |

| Effective rate | 32% | 21.8% |

Same trades, same gains, $5,100 less tax. Compounded across years, the gap does real work.

The higher your bracket, the more the blend saves. At the top 37% bracket (20% long-term rate), the blended rate is 26.8% — a 10.2-point discount on every trading dollar.

Mark-to-Market: The Year-End Rule

Section 1256 contracts are marked to market on the last business day of the year. Any position still open on December 31 is treated as if it were sold at fair market value, and the unrealized gain or loss goes on that year’s return. The position’s cost basis then resets for the new year.

For a 0DTE seller this rule is close to invisible — positions open in the morning and close (or expire) the same afternoon, so there’s rarely anything left open at year end. But it matters for anyone holding longer-dated index options or futures across December 31: you can owe tax on a gain you haven’t realized in cash yet.

Everything flows through IRS Form 6781 (Gains and Losses From Section 1256 Contracts and Straddles), which handles the 60/40 split and feeds the results to Schedule D. Most brokers report the aggregate number for you on the year-end 1099-B.

No Wash-Sale Rule, and a Loss Carryback

Two quieter perks come with the territory.

The wash-sale rule doesn’t apply. Because Section 1256 contracts are marked to market, the rule that disallows a loss when you re-enter a substantially identical position within 30 days simply has no grip. A systematic seller who trades the same SPX structure every single day — including the day after a loss — never has to think about wash sales. The same daily cadence on SPY options can turn into a genuine bookkeeping problem.

Losses can be carried back. Individuals can elect to carry a net Section 1256 loss back up to three years, but only against prior Section 1256 gains. It’s a narrow provision, and worth knowing it exists in a bad year. The details live in IRS Publication 550 .

Which Options Qualify — and Which Don’t

| Instrument | Section 1256? | Why |

|---|---|---|

| SPX options | ✅ Yes | Cash-settled broad-based index option |

| XSP (Mini-SPX) options | ✅ Yes | Same index, 1/10th size |

| VIX, NDX, RUT options | ✅ Yes | Broad-based index options |

| Futures & options on futures | ✅ Yes | Regulated futures contracts |

| SPY options | ❌ No | Option on an ETF — a security, not an index |

| Single-stock options | ❌ No | Equity options |

| QQQ / IWM options | ❌ No | ETF options, same as SPY |

The pattern to remember: if exercise would deliver shares, it’s not a 1256 contract. If it settles in cash against a broad index, it almost certainly is. (Settlement mechanics are their own topic — see cash-settled vs physically settled options .)

What This Means for a 0DTE Premium Seller

A systematic index seller takes hundreds of small gains a year, every one of them held for minutes or hours. Under standard rules that’s the worst possible tax profile — 100% short-term, 100% ordinary rates. Section 1256 converts the majority of it to long-term treatment automatically, with no holding-period gymnastics and no planning required. It stacks with the structural reasons sellers pick SPX in the first place: European exercise , cash settlement, and daily PM-settled expirations .

The edge in premium selling is thin. A 10-point tax discount is one of the few line items that widens it without adding a single unit of market risk.

Frequently Asked Questions

Are SPX options Section 1256 contracts?

Yes. SPX options are cash-settled options on a broad-based index, which makes them nonequity options under Section 1256. All gains and losses receive 60/40 treatment — 60% long-term, 40% short-term — regardless of holding period. XSP, NDX, RUT, and VIX options qualify the same way.

Do SPY options get 60/40 tax treatment?

No. SPY is an ETF, so its options are equity options on a security — outside Section 1256. Gains on SPY options held a year or less are taxed entirely as short-term capital gains at your ordinary income rate, which for active traders means every gain.

Does the 60/40 split apply to losses too?

Yes. Losses are split the same way — 60% long-term, 40% short-term — and net Section 1256 losses can be carried back up to three years against prior Section 1256 gains, an election that doesn’t exist for ordinary capital losses.

Where do Section 1256 gains get reported?

On Form 6781, which applies the 60/40 split and carries the totals to Schedule D. Brokers aggregate Section 1256 activity on the 1099-B, including the year-end mark-to-market adjustment for any open positions.

Related Articles

- SPX vs SPY Options: 4 Key Structural Differences — the full comparison this tax rule sits inside: settlement, exercise style, contract size, and taxes.

- SPX AM vs PM Settlement — the other piece of SPX mechanics worth knowing cold: which contracts settle at the close and which settle on the Friday opening print.

- 0DTE Options Trading: The Complete Guide — where the trading side of the SPX story lives: theta math, strike selection, and the daily cycle.

This content is for educational purposes only and is not tax advice. Tax rates and rules change, and your situation is your own — consult a qualified tax professional before acting on anything here. Options trading involves significant risk of loss.