Definition

Vega (ν) measures the change in an option’s price for every 1-point change in implied volatility (IV).

If an option has a vega of 0.15, its price increases by approximately $0.15 for every 1-point rise in IV, and decreases by $0.15 for every 1-point decline. A vega of 0.40 means the option is $0.40 more valuable for every 1-point IV increase.

Vega is always positive for long options (both calls and puts). Rising IV always increases the value of a long option position regardless of whether it is a call or a put. Short options have negative vega — rising IV hurts the seller, who has collected a premium that is now worth more to buy back.

What Implied Volatility Is

Implied volatility is the market’s forward-looking estimate of how much the underlying will move over the option’s remaining life, expressed as an annualised percentage. It is derived from the option’s market price — “implied” because it is backed out of the price rather than observed directly.

When markets are calm, IV tends to be low — options are priced for modest moves. When uncertainty is high (before major events, during market stress), IV rises — options become more expensive to reflect the greater expected range of outcomes. The VIX index measures the 30-day implied volatility of SPX options and is the most widely followed barometer of overall options pricing.

IV can change independently of the underlying price. A stock can stay flat while its options become more expensive (IV rising) or cheaper (IV falling). Vega captures exactly this sensitivity.

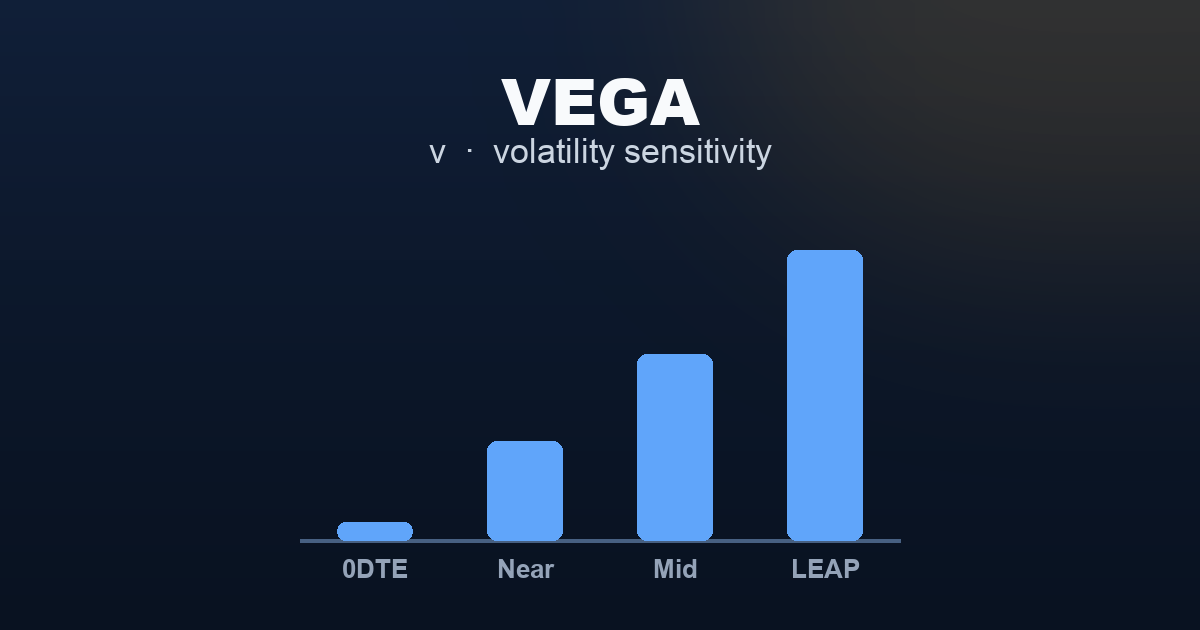

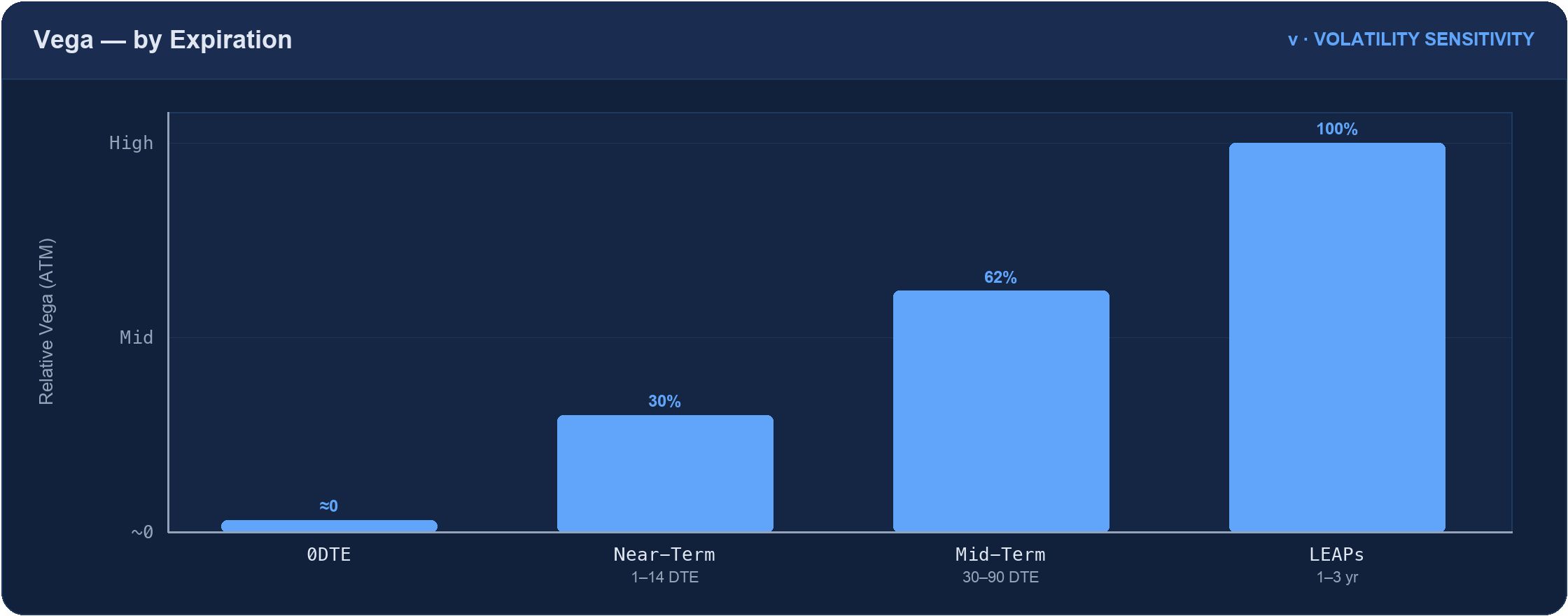

Vega Across the Expiration Spectrum

Vega scales directly with time to expiry. Longer-dated options carry dramatically more vega than shorter-dated options at the same strike.

Vega Across Expiration Timeframes

0DTE — Vega Near Zero

At 0DTE, vega is negligible. The option’s price is almost entirely composed of intrinsic value (for ITM options) or is nearly worthless (for OTM options). There is minimal time value remaining, which means IV changes have almost no effect on the option’s price.

If IV spikes 5 points on a 0DTE option, the price change is minimal — the option is priced for what will happen in the next few hours, not for a range of outcomes over weeks. This is why 0DTE sellers are largely immune to IV crush — the mechanism that deflates option prices after a catalyst resolves — but also why 0DTE buyers cannot benefit from an IV expansion that arrives too late in the session to matter.

Near-Term (1–14 DTE) — Low to Moderate Vega

With days to expiry remaining, vega begins to matter. A 7-DTE option will respond modestly to IV changes — a 5-point IV move might shift the option’s value by $0.20–0.50 for an ATM option.

For near-term options entering a known catalyst window, vega becomes more significant. The option’s price rises as IV expands in anticipation of the event, then can drop sharply after the event resolves — IV crush. A near-term option that expires in 3 days after the catalyst still has enough time value for IV crush to meaningfully reduce its price.

Mid-Term (30–90 DTE) — Significant Vega Exposure

At 30–90 DTE, vega is a primary driver of position value. IV changes of 3–5 points can shift an ATM mid-term option’s price by $1–3 or more, which may represent 10–20% of the option’s total value. A position entered at VIX 16 that experiences a spike to VIX 22 will see its option values increase substantially — beneficial for buyers, harmful for sellers — purely from IV expansion, even without a large underlying move.

LEAPs (1–3 Years) — Vega Is the Dominant Greek

At LEAP expirations, vega is the dominant risk factor. The position is primarily an implied volatility exposure with some directional component.

A 2-year ATM call on SPX might carry a vega of 10–15 or more. A 5-point VIX move would change the position’s value by $500–750 per contract from vega alone. The directional move of the underlying might produce a similar change in value via delta, but the vega exposure from IV changes is comparable in magnitude and can work in either direction independently of price.

LEAP buyers benefit from rising IV. Entering when IV is low (VIX well below historical averages) provides a vega tailwind: if IV normalises upward during the hold period, the position benefits from both the passage of time and any underlying move. Entering when IV is already elevated introduces a vega headwind even if the underlying moves favourably.

IV Rank and IV Percentile

Raw IV levels are difficult to interpret without context. Two tools help frame the current IV level:

IV Rank (IVR): Compares current IV to the range of IV over the past 52 weeks. An IVR of 75 means current IV is at the 75th percentile of its 52-week range.

IV Percentile: Measures what percentage of days over the past year had lower IV than today. An IV percentile of 80% means 80% of days in the past year had lower IV than the current reading.

Both measures contextualise whether options are currently expensive or cheap relative to recent history.

IV Crush

IV crush refers to the rapid decline in implied volatility after a known binary event resolves. Before an earnings report, FOMC decision, or CPI release, IV rises in anticipation of a large move. Once the event passes and its outcome is known, that uncertainty resolves — IV falls, sometimes dramatically, within minutes of the announcement.

Options with meaningful vega exposure lose value during IV crush even if the underlying makes a significant move. The IV-driven price decline can partially or fully offset the gain from intrinsic value increase.

At 0DTE, IV crush has minimal effect — vega is near zero. At near-term expirations, IV crush matters meaningfully. At mid-term and LEAP expirations, a large IV crush can dominate the position’s P&L even when the underlying moves in the expected direction.

Relationships with Other Greeks

Vega and Theta: As DTE increases, vega increases and daily theta decreases. Choosing an expiration is partly a choice about the vega-theta balance.

Vega and Gamma: Shorter-dated options have low vega and high gamma. Longer-dated options have high vega and low gamma. The dominant risk shifts from gamma (short-dated) to vega (long-dated).

Vega and Delta: Deep OTM options have low delta but can carry meaningful vega relative to their premium. The OTM option’s value depends more on implied volatility than on intrinsic price movement, which is why IV changes affect low-delta options proportionately more.

← Theta (Θ) | Back to Greeks Overview | Next: Rho (ρ) →

Related Articles

- Option Selling and Its Advantages — how short vega turns IV crush into a secondary profit source on top of theta decay, and why selling into elevated IV is a structural advantage

- 0DTE Options Trading: The Complete Guide — why IV events (FOMC, CPI, NFP) matter far more for multi-day positions than for same-day expiry, where vega approaches zero

- Slippage in 0DTE Options Trading — IV spikes widen bid/ask spreads on 0DTE options, compounding execution costs when the tape moves fast

- Rho (ρ) — the other DTE-sensitive Greek; like vega, rho is negligible at 0DTE and becomes meaningful only for multi-year positions

This content is for educational purposes only.