Definition

Theta (Θ) measures the rate of change of an option’s price with respect to the passage of one day, with all other factors held constant.

A call option with a theta of −0.05 loses approximately $0.05 in value ($5.00 per standard 100-share contract) for each day that passes, assuming the underlying price and implied volatility remain unchanged. A put with theta of −0.08 loses approximately $0.08 per day.

Theta is almost always negative for long options — both calls and puts. Holding an option means paying for time. The seller of the same option has positive theta: they collect that daily erosion.

What Theta Is Actually Measuring

Options carry two components of value: intrinsic value (how far the option is in-the-money) and extrinsic value (also called time value — the premium above intrinsic). Theta measures the daily erosion of extrinsic value.

Intrinsic value does not decay. A call option 100 points ITM always has at least $100 of intrinsic value regardless of how much time has passed. What decays is the probability premium — the market’s estimate of the chance that an OTM option will move into the money, or that an ITM option will stay there.

Theta is the price of time. When you buy an option, you are buying that probability — and it erodes every day whether or not the underlying moves.

The Decay Curve: Non-Linear Acceleration

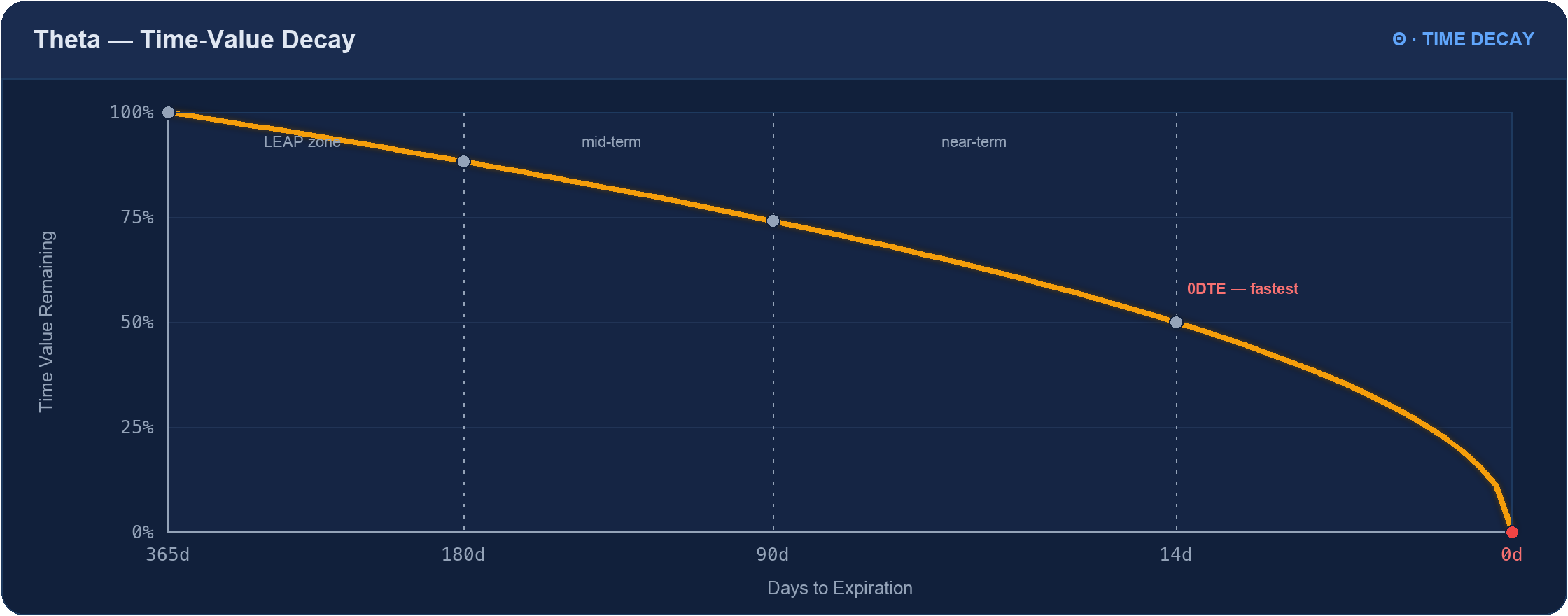

Theta decay is not linear. The rate of decay accelerates as expiry approaches — slowly at first, then rapidly in the final weeks, and maximally in the final days.

The curve illustrates the key property: an ATM option loses time value slowly at first, then progressively faster as expiry approaches. In the final two weeks, the rate of decay per day accelerates sharply.

Theta Across Expiration Timeframes

0DTE — Total Decay in One Session

At 0DTE, theta is at its conceptual maximum: all remaining extrinsic value must decay to zero by end of day (or the following morning for AM-settled options). An ATM 0DTE option may carry $10–30 of time value at market open, depending on implied volatility. Every cent of that value disappears by settlement regardless of what happens with the underlying — unless the underlying moves enough to convert that time value into intrinsic value.

For a 0DTE option buyer, theta works continuously throughout the session. Each hour that passes without a significant underlying move erodes a portion of the remaining premium. By late afternoon, OTM options near the strike may have lost 80–90% of their morning value even without a dramatic underlying move.

For a 0DTE option seller, positive theta is the primary edge: the entire premium is collected by end of day if the underlying stays away from the strike.

Near-Term (1–14 DTE) — Rapid, Accelerating Decay

The final two weeks of any option’s life are characterised by rapidly accelerating theta. An option with 14 DTE loses time value faster each day than it did at 21 DTE. An option at 7 DTE loses time value faster than at 14 DTE. The curve is steep and getting steeper.

Weekend theta is relevant here: options technically lose 3 days of theta over Friday-to-Monday (Saturday and Sunday count as calendar days even though markets are closed). Most brokers display this as 3× the daily theta rate, though the actual decay typically shows on Friday afternoon and again Monday morning.

Mid-Term (30–90 DTE) — Moderate, Steady Decay

At 30–90 DTE, theta is moderate. An option loses a meaningful but not dramatic amount of time value each day. The absolute dollar amount of daily theta may be similar to near-term options, but the remaining time value is much larger, so each day represents a smaller percentage loss.

Mid-term option sellers benefit from steady theta income over multiple weeks. Mid-term buyers have time to wait for the underlying to move — a position entered at 60 DTE has four weeks before entering the accelerated near-term decay zone.

LEAPs (1–3 Years) — Negligible Daily Decay

At LEAP expirations, theta is very small in absolute daily terms. A 2-year ATM option may carry substantial time value — potentially hundreds of dollars per contract — but the daily theta might represent only $1–5 of erosion per day. From a day-to-day perspective, the position barely moves on theta alone.

However, this creates a trap for long-LEAP holders who hold too long. Over a full year, even small daily theta accumulates significantly. A LEAP held for 12 months loses time value proportional to the difference between 24 months of time value and 12 months — which, due to the non-linear curve, can be a meaningful fraction of the original premium.

Theta and At-the-Money Options

Theta is highest for at-the-money options and decreases for both ITM and OTM options.

- ATM options have the most time value to decay and therefore the highest absolute theta. All of their premium is extrinsic.

- Deep ITM options have high intrinsic value but low time value. Their theta is small because there is little extrinsic value left to erode.

- Deep OTM options have low absolute theta because the premium is already small. As a percentage of remaining value, OTM options may decay quickly — but the absolute dollar amount is small.

Relationships with Other Greeks

Theta and Gamma: These are always in opposition for any options position. Long options have negative theta (you pay daily) and positive gamma (you benefit from large moves). Short options have positive theta (you collect daily) and negative gamma (large moves hurt).

Theta and Vega: As DTE increases, vega increases and daily theta decreases. As DTE decreases, daily theta accelerates and vega shrinks. A 0DTE option has maximum theta and near-zero vega. A LEAP has maximum vega and minimum theta.

Theta and IV: When implied volatility rises, option premiums increase — which means there is more time value to decay, increasing theta in absolute terms. High-IV environments produce higher theta for both buyers and sellers.

← Gamma (Γ) | Back to Greeks Overview | Next: Vega (ν) →

Related Articles

- Option Selling and Its Advantages — why positive theta is the core structural edge for premium sellers and how the decay curve benefits sellers of short-dated options

- 0DTE Options Trading: The Complete Guide — theta at its maximum on expiration day; how a 0DTE condor converts the daily decay cycle into a same-session income event

- The Commission Tax on the 0DTE Iron Condor — the tension between closing early to cap gamma risk vs holding to expiry to capture the final theta and skip the exit commission

- Gamma (Γ) — gamma and theta always trade off; you cannot collect one without accepting the other in any long or short options position

This content is for educational purposes only.