Definition

Rho (ρ) measures the change in an option’s price for every 1 percentage-point (100 basis point) change in the risk-free interest rate.

A call option with a rho of +0.08 increases in value by approximately $0.08 for every 1% rise in interest rates. A put option with a rho of −0.06 decreases in value by $0.06 for every 1% rise in rates.

Calls have positive rho — they benefit from rising rates. Puts have negative rho — they are hurt by rising rates.

Rho is the least dramatic of the five primary Greeks for most options positions. Interest rates change far less frequently than underlying prices, IV, or time — and for short-dated options, a rate change between entry and expiry is essentially impossible. But for long-dated positions held across rate cycles, rho becomes a meaningful and sometimes underestimated source of risk.

Why Interest Rates Affect Option Prices

The intuition comes from the cost-of-carry concept. Owning a call option provides synthetic exposure to the underlying without requiring the capital to buy it outright. That capital, in the meantime, earns the risk-free rate. When rates rise, the implied value of this capital efficiency increases — making calls more valuable. Puts, which provide short exposure, become relatively less valuable because the cost-of-carry advantage of not holding the underlying decreases.

More precisely: options pricing models use the risk-free rate to discount the expected future payoff back to present value. Rising rates reduce the present value of future payoffs — this increases call prices (because the forward price of the underlying rises with rates) and decreases put prices.

The direction of the effect:

- Rising rates → calls more valuable, puts less valuable

- Falling rates → calls less valuable, puts more valuable

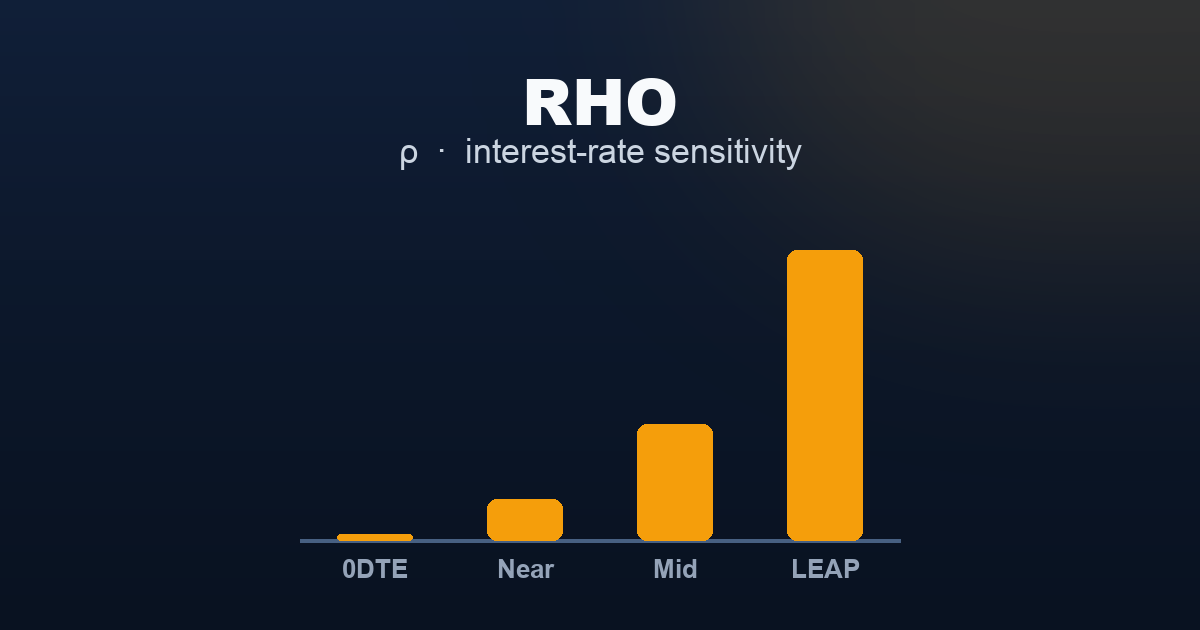

Rho Across Expiration Timeframes

| Expiration | Rho Magnitude | Practical Relevance |

|---|---|---|

| 0DTE | Effectively zero | None — rates cannot change within a single trading session |

| Near-Term (1–14 DTE) | Negligible | Central banks do not change rates between consecutive days |

| Mid-Term (30–90 DTE) | Small but present | A Fed rate change during a 2–3 month hold can shift option prices modestly |

| LEAPs (1–3 years) | Significant | Multi-year positions span entire rate cycles; rho accumulates over time |

0DTE — Zero Relevance

At 0DTE, rho is effectively zero and can be ignored entirely. Interest rates are set by central bank committees that meet on a predetermined schedule and change rates by deliberate policy action — not intraday. No rate change will occur between market open and close. For a same-day position, rho does not exist as a practical risk.

Near-Term (1–14 DTE) — Negligible

For near-term options spanning a few days to two weeks, rho remains negligible. Rate decisions are infrequent events (the Federal Reserve meets 8 times per year). The probability of a rate change in any given two-week window is low, and even if it occurred, the magnitude of the rho effect on a short-dated option would be minimal.

Near-term options are rarely positioned around interest rate risk. The Greeks that matter here are gamma, theta, and vega.

Mid-Term (30–90 DTE) — Small but Measurable

At 30–90 DTE, a position may span one or two Federal Reserve meeting dates. If a rate change occurs during the hold, rho becomes a modest contributor to position P&L. A 25-basis-point rate cut for a mid-term call with rho of +0.15 would change the call’s value by approximately +$0.04 — noticeable but not dominant.

During periods of active monetary policy (a rate hiking cycle or cutting cycle), mid-term options holders should be aware that rho is present, even if it is rarely the primary driver of profit or loss.

LEAPs (1–3 Years) — Meaningful Exposure

At LEAP expirations, rho accumulates into a meaningful risk factor. A 2-year call might carry a rho of +0.50 to +1.00 or more (for higher underlying prices). A 100-basis-point rate increase over the hold period would increase the call’s value by $0.50–1.00 purely from rho, while a 100-basis-point rate cut would reduce it by the same amount.

For LEAP positions entered during a high-rate environment, a subsequent rate cutting cycle introduces a rho headwind on long calls (rates falling reduces call value via rho) and a rho tailwind on long puts (rates falling increases put value via rho).

LEAP buyers of calls are implicitly long rho — they benefit if rates rise. LEAP put buyers are implicitly short rho — they benefit if rates fall. This alignment is structural, not a choice.

Rho for Deep ITM vs OTM Options

Rho is largest for deep in-the-money options and near zero for far out-of-the-money options.

- Deep ITM calls carry the highest positive rho. They behave most like the underlying, so the cost-of-carry effect is largest.

- ATM options carry moderate rho.

- Far OTM options carry near-zero rho. Their value is dominated by the probability of a large move, which is largely independent of the current interest rate level.

This pattern mirrors the delta curve: options with high delta carry high rho (for calls), and options with low delta carry low rho.

Rho vs Other Greeks: Relative Importance

To contextualise rho’s practical importance:

- A 1-point VIX move changes option value via vega — this can happen in minutes.

- A $1 underlying move changes option value via delta — this happens continuously.

- A 1-day passage of time changes option value via theta — this happens every day.

- A 100-basis-point rate change changes option value via rho — this may happen once or twice a year, by committee decision, with advance market pricing.

For most options positions most of the time, rho is the last Greek to examine. The priority order for risk management is almost always: delta → gamma → theta → vega → rho.

The exception is a LEAP position held across a significant rate cycle — where cumulative rho exposure over 12–24 months can rival the contribution of other Greeks.

Dividend Sensitivity (Pseudo-Rho)

For equity options on dividend-paying stocks (not index options like SPX), a related sensitivity exists for dividend payments. When a company pays a dividend, the stock price typically drops by the dividend amount on the ex-dividend date. This affects option pricing in a way structurally similar to rho: dividends increase put values and decrease call values.

SPX options are cash-settled index options and are not directly affected by individual stock dividends, though the index level itself reflects the aggregate dividend behaviour of its components.

Relationships with Other Greeks

Rho and Delta: Deep ITM options have both high delta and high rho (for calls). Far OTM options have both low delta and low rho. The two Greeks are positively correlated across the moneyness spectrum.

Rho and DTE: Rho scales with time to expiry, in the same direction as vega. Longer-dated options carry more rho. Unlike vega, however, rho’s importance scales with the frequency and magnitude of actual rate changes, which are infrequent and scheduled rather than continuous.

Rho and Vega: Both increase with DTE, making them the dominant Greeks for LEAP positions. In practice, IV cycles tend to be more frequent and larger in impact than rate cycles for most LEAP holding periods.

← Vega (ν) | Back to Greeks Overview →

Related Articles

- Introduction to Options Trading — the foundational primer where all five Greeks are introduced alongside calls, puts, and option pricing

- Vega (ν) — the other long-dated Greek; for LEAP positions, vega and rho often compete as the dominant risk factors depending on whether IV or rates are more active

- Options Greeks — Overview — how rho fits alongside the four Greeks that are more consistently active across the full expiration spectrum

This content is for educational purposes only.