Definition

Gamma (Γ) measures the rate of change of delta per $1 move in the underlying asset.

If a call option has a delta of 0.50 and a gamma of 0.03, and the underlying rises $1, the new delta will be approximately 0.53. If the underlying rises another $1, the delta will be approximately 0.56. Gamma compounds: as the underlying moves, delta changes, and the rate of that change is gamma.

Gamma is always positive for long options (both calls and puts) and always negative for short options. It does not depend on whether the option is a call or a put — only on whether you are long or short.

What Gamma Means in Practice

Delta describes where a position is. Gamma describes how fast it gets somewhere else.

A position with high positive gamma benefits from large moves in either direction — as the underlying moves away from the strike, delta accelerates in the favourable direction. A position with high negative gamma suffers from large moves — as the underlying moves against the short strikes, the position’s directional exposure worsens faster than a static delta would suggest.

This is why gamma is described as the “accelerator.” It is not the rate of loss or gain itself — it is the rate at which the rate of loss or gain changes.

Gamma Across the Strike Spectrum

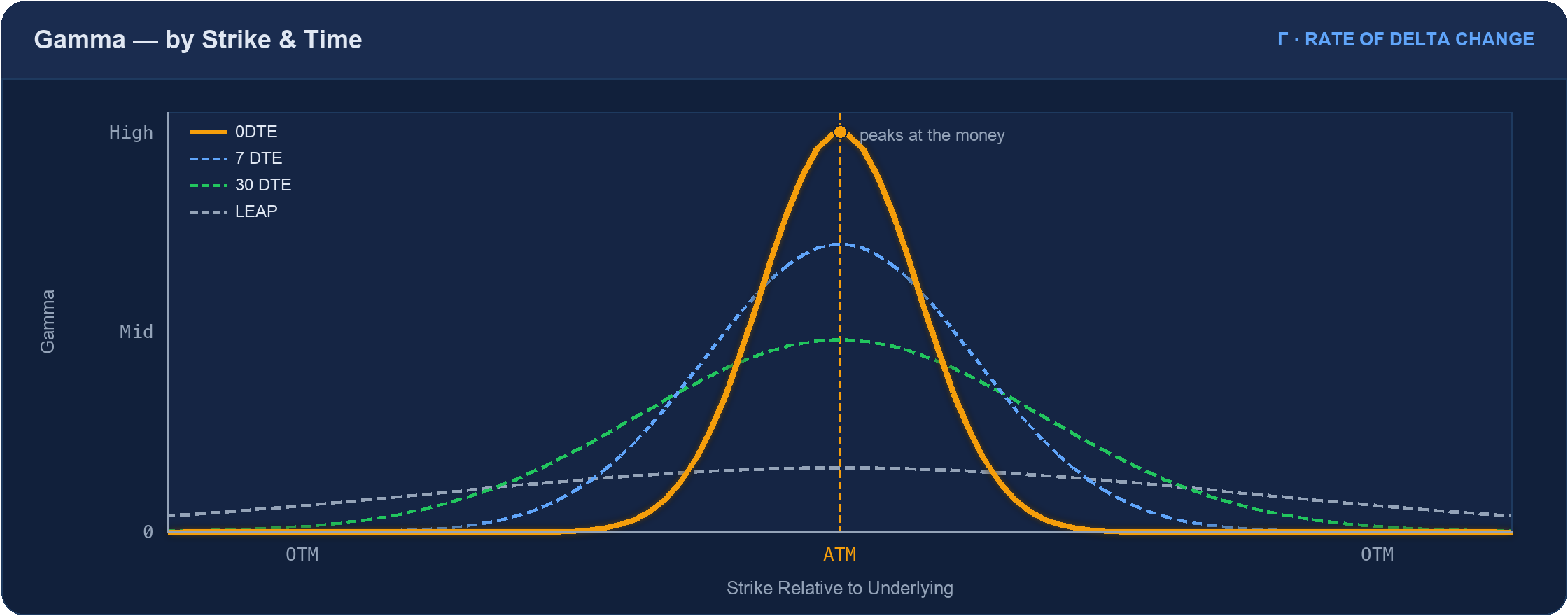

Gamma is not uniform across all strikes. It peaks at the at-the-money strike and declines toward zero for deeply in- or out-of-the-money options.

The ATM strike always has the highest gamma. The key difference across expirations is the sharpness of the peak: at 0DTE, gamma at ATM is extreme and drops off steeply. At 30 DTE, the curve is lower and wider. At LEAP expirations, the curve is nearly flat.

Gamma Across Expiration Timeframes

0DTE — The Gamma Spike

Gamma is at its theoretical maximum at 0DTE for options near the ATM strike. The reason is probability mechanics: with no time remaining, the option must converge to either zero or intrinsic value by end of day. Near the ATM strike, every $1 move in the underlying significantly shifts that probability, causing delta to change rapidly.

The practical consequence: a position that appears delta-neutral or safely out-of-the-money at 10 AM can develop significant directional exposure by 2 PM on a trending day, with little time for the underlying to reverse. The same $10 SPX move that barely affects a 30-DTE iron condor can substantially change the delta profile of a 0DTE position.

Gamma risk at 0DTE is not linear. Near the ATM strike, gamma is extreme. Thirty points away from the strike, gamma drops sharply. This concentration near ATM is why 0DTE short options near the money carry disproportionate risk in the final hours.

Near-Term (1–14 DTE) — Elevated and Accelerating

Gamma remains elevated at near-term expiries, particularly in the final 2–3 days. As each day passes, gamma at ATM increases — a 7-DTE option has higher ATM gamma than a 14-DTE option; a 2-DTE option has higher gamma still.

Near-term positions require active monitoring because delta can change meaningfully on intraday moves. The binary character of 0DTE has not yet fully emerged, but the gamma acceleration is well underway.

Mid-Term (30–90 DTE) — Moderate and Manageable

At 30–90 DTE, gamma is moderate. The underlying must move substantially to produce a meaningful delta change. A $20 SPX move might shift a mid-term option’s delta by 0.05–0.08 — enough to notice but not enough to dramatically alter a position’s risk profile in a single session.

This predictability is one reason mid-term options are often described as more forgiving. The position has time to recover, and the delta change from any given move is gradual.

LEAPs (1–3 Years) — Gamma Near Zero

At LEAP expirations, gamma approaches zero. A deep ITM call with a delta of 0.85 and 2 years to expiry will still have a delta near 0.85 after a $50 underlying move. The delta changes, but only slowly.

This low-gamma characteristic makes LEAPs behave more like the underlying in directional terms. For LEAP buyers, large moves are profitable — but the profitability comes primarily from intrinsic value growth, not gamma amplification. For LEAP positions, the primary risk shifts to vega (IV expansion) rather than gamma (rapid delta change).

Long Gamma vs Short Gamma

Long gamma (buying options): you benefit from large moves in either direction. As the underlying moves away from your strike, your delta accelerates in the favourable direction. The cost is theta — you pay daily time decay while waiting for the move.

Short gamma (selling options): you benefit from the underlying staying near the strike, collecting theta each day. But if the underlying makes a large move, your delta accelerates in the unfavourable direction. The loss on a large move can substantially exceed the premium collected if the move is large enough.

Gamma and theta are inseparable. Long gamma always comes with negative theta. Short gamma always comes with positive theta.

Relationships with Other Greeks

Gamma and Theta: The tighter the relationship, the more important at short expirations. High gamma at 0DTE is paired with high theta at 0DTE. You cannot have one without the other in a long option position.

Gamma and Vega: At the same strike, longer-dated options have lower gamma but higher vega. Shorter-dated options have higher gamma but lower vega. Choosing an expiration is partly a choice about which Greek dominates the position.

Gamma and Delta: Gamma is simply the derivative of delta. Understanding the S-curve shape of delta explains why gamma peaks at ATM — that is where the slope of the delta curve is steepest.

← Delta (Δ) | Back to Greeks Overview | Next: Theta (Θ) →

Related Articles

- 0DTE Options Trading: The Complete Guide — gamma is the central risk on expiration day; why holding through the final hour requires strict discipline

- 0DTE Iron Condor: The Strategy and the Rules — the 50% stop and early exit rules exist specifically because of how gamma behaves in the final session hours

- Slippage in 0DTE Options Trading — gamma-driven quote instability late in the day is one reason 0DTE fills are harder than they look on paper

- Theta (Θ) — gamma and theta are inseparable; understanding one requires understanding the other

This content is for educational purposes only.