Definition

Delta (Δ) measures the rate of change of an option’s price relative to a $1 change in the underlying asset’s price.

If a call option has a delta of 0.60, its price increases by approximately $0.60 for every $1 the underlying rises, and falls by approximately $0.60 for every $1 the underlying drops. A put option with a delta of −0.40 gains approximately $0.40 in value for every $1 the underlying falls.

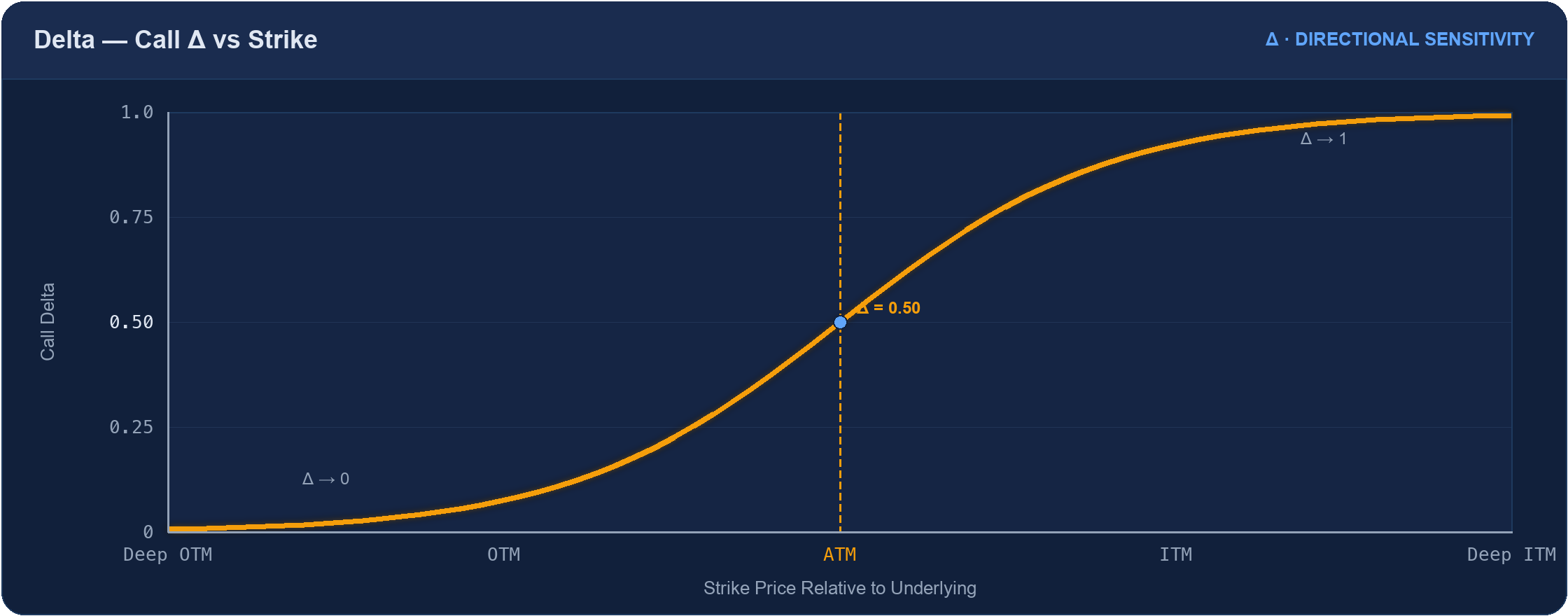

Calls carry positive delta: range 0 to +1. Puts carry negative delta: range −1 to 0.

Delta is the most intuitive Greek — it translates underlying price movement into option price movement in familiar dollar terms.

What the Delta Value Tells You

| Delta Range | Description | Position Relative to Strike |

|---|---|---|

| 0 to ±0.20 | Low sensitivity; option barely moves with underlying | Far out-of-the-money |

| ±0.20 to ±0.40 | Moderate sensitivity | Out-of-the-money |

| ±0.45 to ±0.55 | Near-equal sensitivity in both directions | At-the-money |

| ±0.60 to ±0.80 | High sensitivity; option tracks underlying closely | In-the-money |

| ±0.80 to ±1.0 | Near dollar-for-dollar tracking | Deep in-the-money |

ATM options carry delta close to ±0.50 because at the strike price, there is roughly equal probability of the option finishing in or out of the money. Each $1 move in the underlying shifts that probability approximately in half.

Delta as a Probability Proxy

Delta is frequently used as a rough approximation of the probability that an option expires in-the-money. A 0.30-delta call option is approximately 30% likely to finish ITM at expiration. A 0.15-delta put is approximately 15% likely to expire ITM.

This approximation comes directly from options pricing theory, where the delta of a call equals the probability that the underlying finishes above the strike under the risk-neutral measure. In practice, it serves as a useful heuristic for strike selection and risk assessment, though it is not a precise real-world probability.

The Delta Curve

The S-shape is characteristic. At the extremes, delta is stable and near its boundary values (0 or 1). Near the strike, delta changes rapidly — this is where Gamma is highest.

Delta Across Expiration Timeframes

0DTE — Binary Behaviour Near the Strike

At 0DTE, delta collapses toward a binary state. An option that starts the session at delta 0.50 (ATM) can swing to delta 0.90 on a 20-point underlying rally, then back to 0.15 on a reversal — all within the same trading day.

This happens because with zero time remaining, the probability that an option finishes in-the-money is converging toward either 0% or 100%. An option 40 points out-of-the-money at 3:45 PM has almost no chance of recovering. An option 40 points in-the-money will almost certainly settle at its intrinsic value. Delta reflects this collapsing uncertainty.

The practical consequence: 0DTE options near the ATM strike are extremely sensitive to underlying direction. Small intraday trends can dramatically alter the delta profile of a position within minutes, with little time for the underlying to reverse.

Near-Term (1–14 DTE) — Elevated but Not Binary

With a few days to expiry, delta is elevated but not yet fully binary. ATM options still carry delta near 0.50. Out-of-the-money options don’t collapse to zero as immediately — a 30-point OTM option at 7 DTE still has several days to move into the money, so its delta might be 0.20–0.30 rather than near zero.

Delta sensitivity to underlying moves is high at near-term expiries. Positions can shift quickly but with slightly more warning than at 0DTE. The binary character of 0DTE is not yet fully present.

Mid-Term (30–90 DTE) — Stable and Predictable

At 30–90 DTE, delta is most stable. ATM options carry delta near 0.50 and remain near 0.50 even after moderate underlying moves, because there is sufficient time remaining for the option to move in or out of the money. Delta only changes meaningfully after large underlying moves or the passage of significant time.

This stability makes mid-term options the most predictable for directional trading. A 0.35-delta call is still approximately 0.35 delta after a $10 underlying move, because the out-of-the-money strike still has 60+ days of time for the underlying to reach it.

LEAPs (1–3 Years) — Stock-Like or Near-Zero

At multi-year expirations, delta behaves differently at the extremes:

- Deep ITM LEAPs carry delta near 0.80–0.95 and track the underlying almost like a stock position. A 2-year call option that is already 500 points in-the-money behaves primarily as a leveraged directional exposure.

- ATM LEAPs carry delta near 0.50 — the same as any ATM option — but the delta barely moves with moderate underlying price changes, because gamma is very low.

- Far OTM LEAPs carry delta of 0.10–0.25, which reflects genuine multi-year probability. An option 300 points out-of-the-money with 2 years remaining has meaningful time to close that gap. This low delta does not mean the option is nearly worthless — it may carry significant vega.

Deep ITM LEAPs are sometimes used as stock substitutes: they provide high directional exposure (delta near 1.0) at a fraction of the capital required to own the underlying outright.

Delta in Multi-Leg Positions

The delta of a multi-leg options position is the sum of the individual leg deltas (each weighted by its contract quantity and multiplier).

A position where all legs net to a delta near zero is described as delta-neutral at the moment of entry. This doesn’t mean the position is risk-free — it means it has no initial directional preference. As the underlying moves, the net delta of most multi-leg structures will drift away from zero, which is why Gamma matters.

Relationships with Other Greeks

Delta and Gamma: Gamma is the rate of change of delta. High gamma means delta is changing rapidly — at 0DTE near ATM, gamma is extreme, which is why delta swings so dramatically on small moves. Low gamma (as in LEAPs) means delta is stable.

Delta and Theta: ATM options (delta ≈ 0.50) carry the highest absolute theta decay. As an option moves deep ITM (delta → 1.0) or deep OTM (delta → 0), theta decreases in absolute terms because there is less time value left to erode.

Delta and Vega: Deep OTM, low-delta options are relatively more vega-sensitive — their value depends heavily on implied volatility because they have little intrinsic value. High-delta ITM options are less affected by IV changes because intrinsic value dominates.

← Back to Greeks Overview | Next: Gamma (Γ) →

Related Articles

- Introduction to Options Trading — where delta first appears alongside calls, puts, and basic option mechanics

- 0DTE Iron Condor: The Strategy and the Rules — delta is the primary tool for strike selection; the 20-delta target and what it implies for probability and premium

- Iron Condor Strategy Guide — how to use delta to choose short and long strikes and understand the position’s directional exposure at entry

- Gamma (Γ) — delta’s rate of change; why 0DTE positions can shift so quickly on a small intraday move

This content is for educational purposes only.