30-Second Summary

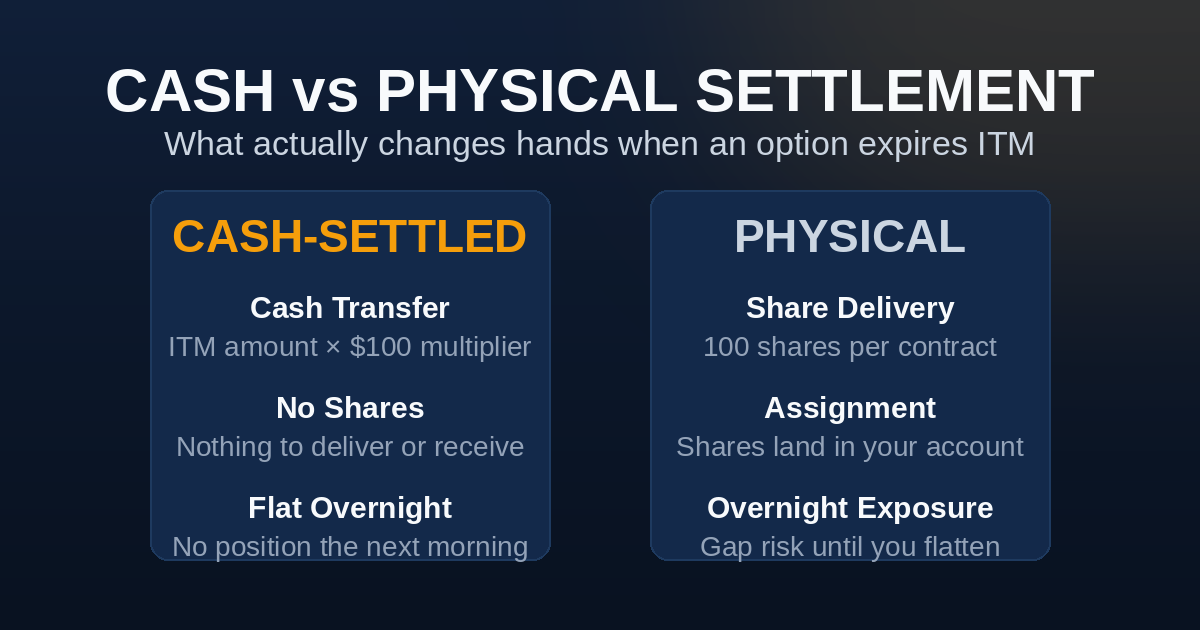

Settlement type answers what happens when an option expires in the money. A cash-settled option pays the ITM amount in cash — intrinsic value times the $100 multiplier moves between accounts, and no shares exist anywhere in the process. A physically settled option delivers the underlying: 100 shares per contract change hands at the strike price. Index options (SPX, XSP, VIX) settle in cash; equity and ETF options (SPY, single stocks) settle in shares. The dollars at stake are identical either way — what differs is whether expiration ends the trade or hands you a stock position to manage.

How Cash Settlement Works

When a cash-settled option expires in the money, the ITM amount is converted directly to cash: (settlement value − strike) × $100 for a call, the reverse for a put. The money is debited or credited, the contract ceases to exist, and the account holds no position the next morning.

Work a real example. You’re short a 5500/5525 call spread on SPX — short the 5500 call, long the 5525 — collected for $4.00 ($400). SPX settles at 5510.

- The short 5500 call is 10 points ITM → you’re debited 10 × $100 = $1,000

- The long 5525 call is out of the money → expires worthless, $0

- Net result: −$1,000 settlement + $400 credit collected = −$600 on the trade

That’s the entire event. No deliveries, no positions, no morning-after decisions. If SPX had settled below 5500, both legs vanish worthless and the full $400 stays. The arithmetic is cold, but it’s only arithmetic — which is exactly the appeal for a 0DTE seller who wants each day’s trade fully dead by dinnertime.

How Physical Settlement Works

A physically settled option that expires in the money settles in the underlying itself. Each ITM contract converts into 100 shares at the strike: an exercised call delivers shares to the holder (and calls them away from the seller); an exercised put delivers shares to the seller at the strike price.

Say you’re short one SPY 550 put and SPY closes expiration Friday at 546. The put is 4 points ITM, it’s exercised, and you’re assigned: 100 shares of SPY arrive in your account at $550 each — a $55,000 purchase, settled through the OCC after the close. Whether that’s a problem depends entirely on the account. A trader running the wheel wants those shares; that’s the strategy working as designed. A spread trader who only ever intended to trade the options now owns $55,000 of stock, carries its gap risk overnight, and may face a margin call Monday if the account can’t support the position.

Physical settlement isn’t worse. It’s just a different contract — one that assumes you have a plan for the shares.

What Is Pin Risk?

Pin risk is the uncertainty a seller faces when the underlying closes at or very near the short strike on expiration day. With SPY at 549.98 against your short 550 put, you genuinely don’t know whether you’ll be assigned: some holders exercise, some don’t, and exercise decisions can be submitted for a while after the closing bell. You find out hours later whether you own $55,000 of stock through the weekend.

Cash settlement reduces that coin-flip to arithmetic. SPX settles at 5500.20 against your 5500 short call? You owe exactly $20 per contract. At 5499.80? Exactly zero. The outcome may be pleasant or painful, but it’s never unknown — and unknown is the part that keeps sellers up at night. (For SPX there’s a second wrinkle worth knowing — AM vs PM settlement decides which print does the settling.)

Cash Settlement Doesn’t Shrink the Loss

One misconception deserves its own section: cash settlement is not a discount. If your short spread finishes fully in the money, the max loss is the max loss — cash settlement pays it out in dollars just as surely as physical settlement does through shares. A 25-point-wide SPX spread that settles fully ITM costs you $2,500 minus credit, full stop.

What cash settlement removes is everything around the loss: the share position, the overnight gap on assigned stock, the margin call, the Monday-morning forced liquidation. The dollar risk is identical by design. The operational risk is not — and operational risk is the kind that turns a bounded losing trade into an unbounded bad week.

Which Products Cash-Settle

| Product | Settlement | What ITM expiration produces |

|---|---|---|

| SPX / SPXW options | Cash | ITM amount × $100 in cash |

| XSP (Mini-SPX) | Cash | ITM amount × $100 in cash |

| VIX options | Cash | ITM amount vs the settlement print |

| NDX, RUT options | Cash | ITM amount × $100 in cash |

| SPY, QQQ, IWM options | Physical | 100 ETF shares per contract |

| Single-stock options | Physical | 100 shares per contract |

The rule of thumb: options on an index settle in cash; options on a security settle in that security. There’s nothing to deliver on an index — you can’t hand someone a basket of 500 weighted stocks — so the cash mechanism isn’t a convenience feature, it’s the only way the contract can work. The same split shows up in exercise style (index options are European, equity options American) and in tax treatment (cash-settled index options qualify for Section 1256’s 60/40 rule).

Frequently Asked Questions

What happens if my SPX option expires in the money?

The ITM amount is settled in cash: intrinsic value at settlement times $100 per contract, debited or credited to your account. No shares are delivered, nothing carries overnight, and the position simply ceases to exist after the settlement value is determined.

What happens if I let a SPY spread expire in the money?

Each ITM leg settles in shares — 100 per contract, assigned or delivered at the strike. If only the short leg finishes ITM, you end up with a naked stock position (long from a put, short from a call) carrying full overnight gap risk, which is why most spread traders close ETF spreads before expiration rather than let settlement decide.

Can cash settlement cause a margin call?

The settlement itself is a simple cash debit, so there are no shares to margin. But the debit is real money — a max-loss settlement can still leave an under-capitalized account negative. Cash settlement removes share logistics, not the obligation to be able to afford the loss.

Are cash-settled options safer than physically settled ones?

The dollar risk is identical for the same structure. Cash settlement is operationally cleaner: no assignment uncertainty, no overnight share exposure, no forced liquidations. Safer is the wrong word — simpler is the right one, and for systematic sellers simplicity compounds.

Related Articles

- European vs American Style Options — settlement’s sibling concept: when exercise can happen, and why early assignment only exists on one side of the table.

- SPX AM vs PM Settlement — the next level of detail for SPX specifically: which print settles the contract, and the overnight trap inside AM settlement.

- SPX vs SPY Options: 4 Key Structural Differences — the full index-vs-ETF comparison that settlement type sits inside.

This content is for educational purposes only. Options trading involves significant risk of loss. Always trade within your risk tolerance.